Insights

J.S. Held Acquires Shechter & Everett to Expand Forensic Accounting Capabilities for Family Law Disputes in Florida

Read MoreIn 2023, there were significant geopolitical shifts, regulatory developments, economic trends, and technological advancements leading to widespread impacts that reverberated across the global business landscape. The resulting whiplash felt by organizations, governments, and communities cannot be overstated.

With change comes both risk and opportunity. In the inaugural J.S. Held Global Risk Report, we combine the technical, scientific, financial, and strategic expertise of our team members to provide insight on influential topics for 2024, including implications of global elections, China’s economic uncertainty, the risks and rewards of artificial intelligence, weather and natural disasters, ESG and sustainability, and political risk from government intervention.

Information shared in the report is a collection of research and observations from J.S. Held experts who advise insurance professionals, legal counsel, governments, investors, and corporations across every sector and geography. If you have any questions or would like to further discuss the risks and opportunities outlined in the report, email [email protected].

Click the links below to jump to a Featured Topic:

In 2024, an extraordinarily high number of national elections will be held across the globe, including in some of the biggest economies: the United States, United Kingdom, India, Mexico, South Africa, Indonesia, Russia – and even the European Parliament. More than four billion people in at least 60 countries will head to the polls to choose who will lead them and shape economic and social policy. In many cases, these elections are being conducted for the first time since the COVID-19 pandemic and major military conflicts – first, Russia’s full-scale invasion of Ukraine, and more recently, the war between Hamas and Israel.

Populism will likely be a common feature of all these contests, with implications for businesses engaging with foreign partners. Populism has been one of the factors behind the shift seen in recent years away from the tenets of open trade, global integration, and a rules-based international order.

Another major factor is perceived national security prerogatives, such as the need to safeguard supply chains, diversify away from dependence on strategic rivals, and even restrict competitors’ technological and economic advancement – a dynamic in US-China relations that transcends party divisions.

As such, regardless of the results of this year’s polls, tariffs, import/export controls, and other forms of protectionism are likely here to stay. However, the combined outcome of these elections may result in major policy shifts – including sanctions, alliances, and energy trade.

The election of populist contenders could result in more erratic policymaking with no clear or consistent economic agenda. Such changes in government leadership could lead to policy shifts that prove risky for business and investment. One example can be seen in South Africa. Falling support for the dominant African National Congress (ANC) will likely force the party into an unprecedented coalition with either hard-left populists or centre-right technocrats this year. This could result in political paralysis, delaying much-needed economic reforms.

The 2024 election cycle could lead to clashes that disrupt the business environment and global supply chains and threaten the safety of staff. In Mexico, where political violence has plagued the country's elections for decades, the army was recently drafted to protect the two leading presidential candidates. In the US, the Capitol Hill riot of January 2021 reflects the risk of post-election unrest when populist candidates refuse to accept the legitimacy of democratic processes.

Success of populist candidates will increase the risks of so-called “resource nationalism” – an admittedly loaded term covering everything from local governments’ legitimate demands for higher royalties from foreign investors through export curbs on key commodities to outright illegal expropriation. For example, Mexico’s ruling party candidate will likely maintain the policy of nationalizing the country’s lithium sector and potentially withdraw existing concession rights for mining companies. In South Africa, where unemployment is the key political issue, the next government is likely to force investors to shoulder more responsibility for social programs.

Expropriation and violations of international trade agreements would invariably result in disputes in construction and related projects, leading to arbitration and insurance cases.

This year’s elections will in many cases serve as referendums on green policies, with populists seeking to move away from broad consensus on net zero to turn it into a wedge issue. In the US, a Trump/GOP administration will likely water down or scrap regulations on clean energy, cut tax subsidies for electric vehicles and other green industries, and again withdraw from international commitments like the Paris Agreement. In Europe, victories for far-right parties in the EU parliament election could prompt the European Council to curb the continent’s ambitious Green Deal.

A Trump/GOP administration will likely seek to cut corporate and individual tax rates, the former from 21% to as low as 15%. Ultimately, any decision on this matter will need to balance the potential positive impact on business valuations across industries against the risk to US fiscal credibility from decreased tax revenues if the financial market upheaval that followed former UK Prime Minister Liz Truss’s similar experiment with tax cuts is anything to go by. Former President Trump has also promised to increase executive control over some federal agencies and reduce funding for others, such as the Federal Trade Commission, which could weaken antitrust and consumer protection restrictions. This could create opportunities for some industries, while also entailing reputational risks.

A probable victory for Keir Starmer’s Labour Party in the UK’s general election will represent a return to a broadly centrist technocratic government. This follows years of instability triggered by Britain’s Brexit vote to leave the EU in 2016, which caused substantial disruption and uncertainty for British businesses trading across the Channel. There is significant opportunity given that Keir Starmer is likely to mend ties with the EU and has pledged to spend GBP 28 billion on green jobs and industry. There may be select nationalization of underperforming services, such as railway companies, while some industries, like utilities, may face tighter regulation.

A growing isolationist stance – especially within the US GOP – could result in an administration that opposes sending further military and financial aid to Ukraine. Meanwhile in Europe, Slovakia’s newly appointed Prime Minister Robert Fico has already announced that he will not support further aid to Ukraine. In addition to Slovakia and Hungary (where Prime Minister Viktor Orban is increasingly aligned with the Kremlin), populists sympathetic to Moscow may also control or influence governments in Austria, Bulgaria, and Romania by the end of 2024. This would severely undermine the West’s ability to maintain a united front on arming Ukraine and sanctioning Russia.

Should Russia gain the decisive upper hand in the conflict as Western military and financial aid to Ukraine ebbs away, security fears on NATO’s eastern flank would damage investment prospects in the region.

Prime Minister Narendra Modi will likely win a third term in the spring. Modi will continue to drive India’s economic ascendance, bolstered by geopolitical developments that make New Delhi an indispensable, although increasingly uncomfortable, partner for the West. India will remain a primary destination for Western investment and businesses seeking to diversify away from China. Despite the business environment’s persistent challenges, there will be opportunities from New Delhi’s continued business-friendly reforms, which include infrastructure investment, incentives for manufacturing, easing of labor laws, and other efforts to boost private investment.

If you have any questions or would like to further discuss the risks and opportunities outlined in this Featured Topic, please email [email protected].

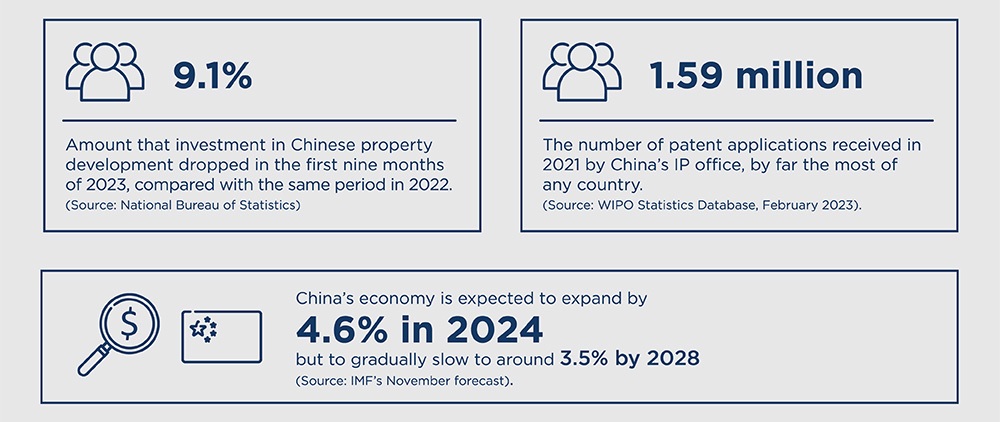

After 30 years of extraordinary growth, China’s economy, the world’s second largest, appears to be entering a new phase of slower expansion. The real estate sector, which accounts for around one-third of Chinese GDP and has been one of the main drivers of the country’s economy, is in crisis. Exports and foreign investment have stalled, youth unemployment is at record levels, and the post-pandemic recovery has been anemic. Meanwhile, there are long-term structural problems: the population is aging, with the cohort of working-age people falling, and the economy remains unbalanced, in part due to consumers opting to save, resulting in weaker demand for products and services. Future levels of foreign investment are also in question: in July-September 2023, China recorded its first deficit in foreign investment, possibly an indication that Western governments’ “de-risking” is starting to have an impact.

The expected prolonged period of slower growth ahead comes at a time when the country’s political, economic, and social fabric has already been tested by almost three years of intermittent COVID-19 lockdowns, which forced many citizens to close or severely curtail the activities of their businesses.

From the realities of the slowdown and geopolitical challenges, a new government agenda has emerged: one that appears to prioritize state control, economic stability, national security, and self-sufficiency. So far, there is little indication that Beijing will make the economic changes to rebalance the economy, including shifting toward a more consumption-driven model. Nonetheless, China retains enormous potential to grow and has significant bright spots in its economy, such as the world’s busiest patent office and its electric vehicle (EV) industry.

Western countries and China are attempting to reduce strategic vulnerabilities, as well as insulate and protect their economies through regulation and trade restrictions. The US and some of its allies have imposed tariffs, export bans, and other restrictions on partnerships with an investment in Chinese companies, especially those involved in developing sensitive strategic technologies, such as advanced microchips, quantum computing, and artificial intelligence. China has retaliated with trade restrictions of its own. That said, there have been some limited attempts to increase cooperation, including visits by three US cabinet secretaries in 2023 and the San Francisco summit between Chinese President Xi Jinping and US President Joe Biden. However, various restrictions on business and free trade, imposed by both sides, will remain in place or even expand as long as intractable political issues – such as the status of Taiwan – remain unresolved.

China’s slower economic expansion threatens projected growing demand for some raw materials, particularly those used in its booming construction sector. This is globally significant because China currently consumes enormous amounts, including nearly one-fifth of the world’s oil; half of its refined copper, nickel, and zinc; and more than three-fifths of its iron ore. That said, the shift is relative – China will continue to need more raw materials, albeit at a slower pace – and Xi’s future political decisions will significantly impact demand. He may, for example, support property developers to finish projects already underway, in the interest of maintaining social order, or prioritize accelerating the country’s green energy transition, both of which would increase demand for some raw materials.

The combination of rising geopolitical tensions and increasing pressures on Chinese companies amid an economic slowdown may lead to more legal cases involving international firms. These could include cases concerning breach of contract, insolvencies, pandemic-related difficulties, and regulatory and sanctions issues. International companies doing business in China through joint ventures or otherwise should take special precautions to protect themselves and their intellectual property.

China has been the leading global investor in Africa, with Chinese financing peaking in 2016 as a result of its Belt and Road Initiative, which aims to strengthen Beijing’s global influence through strategic infrastructure development around the globe. However, a Chinese economic slowdown could cause China to change its foreign investment strategy, with certain sectors and countries becoming less of a priority. Although critical minerals are unlikely to be deprioritized, this still could open up opportunities for countries such as the US, UK, and EU nations trying to increase their influence in Africa and secure the commodities needed for their decarbonization drives. For example, the US, together with the Democratic Republic of the Congo (DRC) and Zambia, recently agreed to jointly develop the supply chain for EV batteries. Separately, a recent deal will see Namibia export rare earth minerals and green hydrogen to the EU.

Businesses in India will benefit from the reallocation of some investment from China, as it continues to grow in both population and economic strength. The World Bank forecasts India’s GDP to grow at 6.3% in fiscal year 2023/2024.

Opportunities will open up in other economies, too. China has long been South America’s top trading partner and the second largest for the entire Latin America region. The Belt and Road Initiative poured money into some twenty Latin American countries, primarily in the energy and infrastructure sectors. A slower-growing Chinese economy, coupled with US incentives to ‘onshore’ supply chains in ‘friendly’ countries, will help Western companies be more competitive in these markets.

Strategically important sectors like EV batteries and renewable energy are likely to continue to receive state support. Moreover, in practice, China’s strong position across the EV supply chain may prove much more resilient to Western attempts at “decoupling” than some senior Western officials’ tough rhetoric suggests.

China retains significant potential for future economic growth because of its large population, including many new university graduates. Strong state control over the economy also gives Beijing the tools to mitigate and tackle many of the structural problems in China’s economy. Overcoming the current economic impasse, painful though it may be, could eventually result in a more resilient, balanced economy in which growth is driven more by domestic consumption and less by credit-fueled investment. Policy shifts in this direction could provide companies selling to China’s large domestic market with significant opportunities.

The Chinese government’s plan to increase spending on infrastructure projects should help its construction sector. This comes despite a continuing downturn in the property market, which will adversely affect growth in residential and non-residential buildings, according to the US International Trade Administration. At the same time, China dominates the global construction market. The country’s influence can be seen in companies such as the China State Construction Engineering Corp., the China Railway Construction Corp., and the China Communications Construction Group. According to the Engineering News-Record in 2023, these three firms are listed among the top international contractors in the building and transportation sectors.

If you have any questions or would like to further discuss the risks and opportunities outlined in this Featured Topic, please email [email protected].

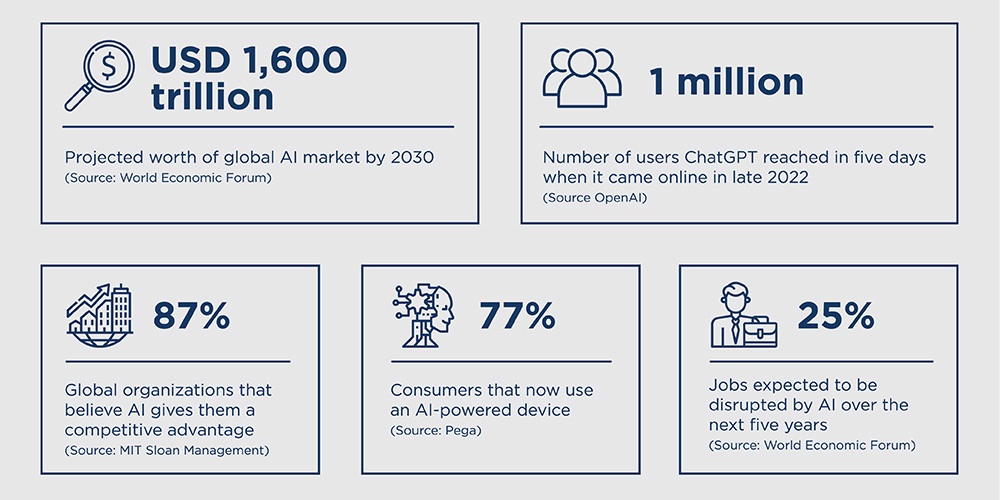

The race to develop AI and calls to regulate it are heating up around the world. In November 2023, 28 countries, including the US, UK, China, and the European Union, met and pledged to work together to address and contain the potentially harmful risks of AI. These countries are establishing guidelines to manage the risks while balancing the benefits of this new and evolving technology.

AI holds the promise of dramatic improvements across industries and greater cybersecurity by improving threat detection and identifying anomalies. Yet AI also brings potential threats to personal privacy, job loss, surveillance, bioweapons, cyberattacks, intellectual property issues, and the proliferation of misinformation, among other challenges.

Among the legislation being introduced in different jurisdictions, the EU is in the final stages of formulating its AI Act. The legislation would establish requirements for providers and users depending on the level of risk, whether it be “unacceptable risk,” meaning those systems considered a threat to people, which will be banned; or “high risk,” which would adversely affect fundamental rights or safety. The EU is aiming for a more comprehensive approach to AI regulation in an attempt to limit surveillance, while the US is seeing more of a patchwork and has yet to create a unified regulatory approach throughout its various states. Still, US President Joe Biden issued an executive order in late 2023 focusing on developing AI in tandem with safety and security. According to the White House, it establishes new standards for protecting the privacy and interests of both consumers and workers and advances equity and civil rights while promoting innovation and competition.

Generative AI (Gen-AI), like ChatGPT and other chatbots, can imitate human speech and writing to create phony personas and documents, as well as “deep fake” photos and videos that have shown prominent people in false and reputationally harmful settings. Bot networks can create new ways to exploit vulnerabilities, including the expansion of phishing to gain access to personal information, as well as the replication of voices to fraudulently request money from family and friends. These uses of AI tools by threat actors to facilitate wrongdoing pose a growing risk to both businesses and consumers.

When Gen-AI creates a particular work, there is a question as to whether copyright, patent, or trademark protections apply. There is also uncertainty pertaining to the ownership of AI-generated works. Additionally, tech companies have increasingly been sued for using copyrighted material to train their AI programs. Some recent examples include a class action filed by a San Francisco-based law firm challenging the training and output of AI-based systems for software programmers. More recently, the New York Times filed a lawsuit over the use of millions of its articles to train ChatGPT without the newspaper’s permission.

AI is not infallible, especially when it is not trained with a sufficiently robust dataset that is tested for bias. As a result, AI can produce hallucinations, namely answers that are not accurate or are completely false. AI hallucinations pose the risk of reputational damage or criminal charges. In one example, a US lawyer was sanctioned by a court for using ChatGPT for legal research that was full of false case citations. As a result, at least two federal district courts are mandating certification of the use of AI in cases, and a federal appeals court is considering doing the same. Under certification requirements that have been adopted or proposed, lawyers must attest that either no portion of the filing was drafted using Gen-AI, or if Gen-AI was relied upon, that the work was checked for accuracy by a human being.

Automation, especially with the increasing adoption of Gen-AI, will create dependency, and combined with the loss of skills, could result in a multiplying effect on the ability to deliver proactive and responsive measures. Once dependency has been “baked in” to a workflow, it may be very difficult to correct. For example, poorly programmed AI could result in biased outputs. Gen-AI could also be used as a crutch that hinders critical thinking and creativity of real people.

AI can help legal and regulatory consultants to detect fraud and conduct investigative data analytics. Compliance departments and legal teams can use Gen-AI systems to examine financial transactions in real time to uncover fraud and initiate internal investigations or examine practices of external vendors or sales agents. Regulators are encouraging many companies to expand internal compliance review capabilities with advanced analytics systems, inclusive of machine learning AI, which can predict patterns of wrongdoing.

Gen-AI can be used to provide enhanced data management practices and information governance by improving classification according to different types of media; increasing the quality of data by reducing errors; keeping data secure from threat actors while in compliance with laws and regulations; locating data; and integrating information from various lists and sources.

AI can be integrated into cybersecurity workflows to enable the quick triaging of alerts, automated incident response workflows, predictive review for phishing detection, identifying bots, and flagging suspicious access.

Language Processing AI, such as ChatGPT, is starting to be introduced to discovery processes of litigation. The eDiscovery industry often uses Technology Assisted Review and other analytic methods to find the most relevant documents early in a review, thereby reducing the cost of the process.

From underwriting to customer service and telematics, the insurance industry has been a leader in the innovative uses of AI. AI can input claims data faster over a long period of time by enabling the automation of time-consuming and repetitive tasks, such as data entry and document verification. It can take photos of car accident scenes and use telematics data to determine how the actions of the drivers or, even the road conditions, contributed to the incident. AI is accelerating fraud investigations by its ability to analyze vast amounts of data in real time and quickly identify suspicious patterns. AI is helping the insurance industry to forecast natural disasters and extreme weather events, in addition to quickly processing claims.

If you have any questions or would like to further discuss the risks and opportunities outlined in this Featured Topic, please email [email protected].

The growing frequency and ferocity of major weather events and natural disasters have pushed the climate change discussion to the forefront of governments and businesses. Droughts, floods, wildfires, earthquakes, and volcanic eruptions, among other weather-related and natural disasters, can damage buildings, bridges, roads, and dams. Tropical cyclones can disrupt fossil fuel drilling in the Gulf of Mexico, while the reliability of renewable energy sources, such as solar and wind, are both completely dependent on weather conditions to function but can also be adversely affected by extreme weather events. An unprecedented storm or disaster event can shut down airports, trains, and electrical power grids and put national security and economic stability at risk.

Governments are responding with tougher climate disclosure laws and mandating other mitigation steps. For their part, companies are taking action to protect their assets from climate-related damage and litigation. Insurance companies are amending their policies and pulling out of some regions that are hit hard with losses to protect their bottom line but are also using new technology to obtain more accurate data and streamline the claims process.

Owners and developers are becoming more attuned to the location, design factors, and building materials used to secure structures. They are also reviewing mitigation strategies. For example, the state of California recently approved the construction of new hospitals with a three-day water tank and their own energy generators to keep the sites fully running in the event of a major disaster. Construction firms are increasingly taking into account the root causes of climate change, as well as its impacts – for example, considering emissions controls, use of solar panels, and stormwater management. They are also reviewing their policies, procedures, and strategies in anticipation of changes to the regulatory environment.

In the US, the Inflation Reduction Act will provide nearly USD 400 billion over the coming decade to cut carbon emissions and lower the cost of clean energy technologies, but it also includes trade protectionism aspects that may spur a backlash from European nations. Additionally, the US Securities and Exchange Commission has proposed rules that increase climate-related reporting requirements of companies. On the state level, California has passed two groundbreaking climate-related bills. One requires companies with annual revenues greater than USD 1 billion that operate in the state to report annually on their emissions. The second requires US companies that do business in California and with annual revenues greater than USD 500 million to disclose climate-related financial risks and what they are doing to mitigate those.

Europe and the UK have already passed strong climate disclosure rules. British regulations require company disclosures to explain how climate change is addressed in corporate governance; its impacts on corporate strategy; how climate-related risks and opportunities are handled; and the performance measures and targets.

While some of the regulations and climate change accords may be beneficial for highly developed countries, they could hold back some emerging economies.

Following a catastrophic weather or natural disaster event, resolving the potential disputes over property damage, causation, and quantification of impact costs and other insurance claims will lead to lawsuits, liability, and costs in defending positions.

Some large companies are, in effect, self-insured. Their incentive is to keep operations going and quickly get their own facilities back online, rather than submit an insurance claim. These companies have become motivated to develop technologies that would address climate risks and have built highly-resilient supply chains.

Many structures now have to incorporate “green designs” that have a minimal impact on the surrounding environment. In India, for example, hospitals are required to have their own micro-grids to sustain power and operations in the event of a storm or natural disaster that cuts off the facility from the main power grids. That technology has started to be adopted in the US.

More companies are reviewing their structures to see if they should retrofit them to withstand extreme weather conditions and natural disasters or build entirely new facilities. This is especially important for companies that are disaster providers, i.e., that deliver goods in emergency situations and cannot afford to have any ‘down’ time. It is also necessary for smaller companies that need to build facilities in one region, in case there is a disaster in another area.

There is a trend of companies hiring forensic meteorologists to mitigate climate-related disasters and gain a competitive advantage, especially when collecting information for an insurance claim or litigation. Storm reports may not contain information that is accurate to the specific project location. Professional meteorologists who recognize the inherent problem with reporting procedures can aggregate and interpret storm data for applicability and accuracy.

Businesses are using pre-loss and post-loss technologies to limit the cost of the insurance claims process. One example of the former is monitoring via early warning systems. Post-loss technology can include ground penetrating radar, drones, satellite imagery, and even underwater remote-controlled vehicles to see the extent of damage following an extreme weather event or natural disaster.

Insurers are using automated claims processing to quickly review and assess claims and reduce the time it takes to settle them. Insurance firms are also using mobile reporting which allows customers to report claims and submit photos and videos of the damage for faster processing.

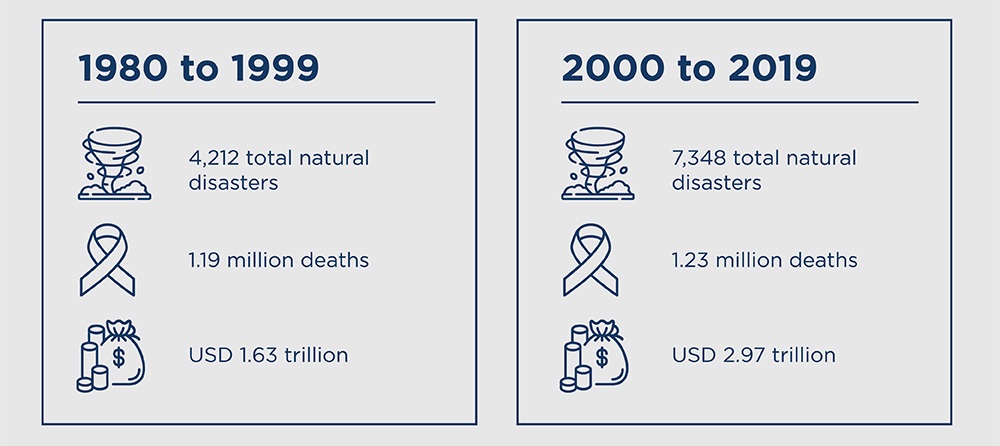

(Source: UNDRR report: The Human Cost of Disasters: an overview of the last 20 years (2000-2019) / The Centre for Research on the Epidemiology of Disasters (CRED)’s Emergency Events Database (EMDAT))

(Source: World Meteorological Organization’s Atlas of Mortality and Economic Losses from Weather, Climate and Water-Related Hazards)

(Source: UNDRR report: The Human Cost of Disasters: an overview of the last 20 years (2000-2019) / The Centre for Research on the Epidemiology of Disasters (CRED)’s Emergency Events Database (EMDAT))

If you have any questions or would like to further discuss the risks and opportunities outlined in this Featured Topic, please email [email protected].

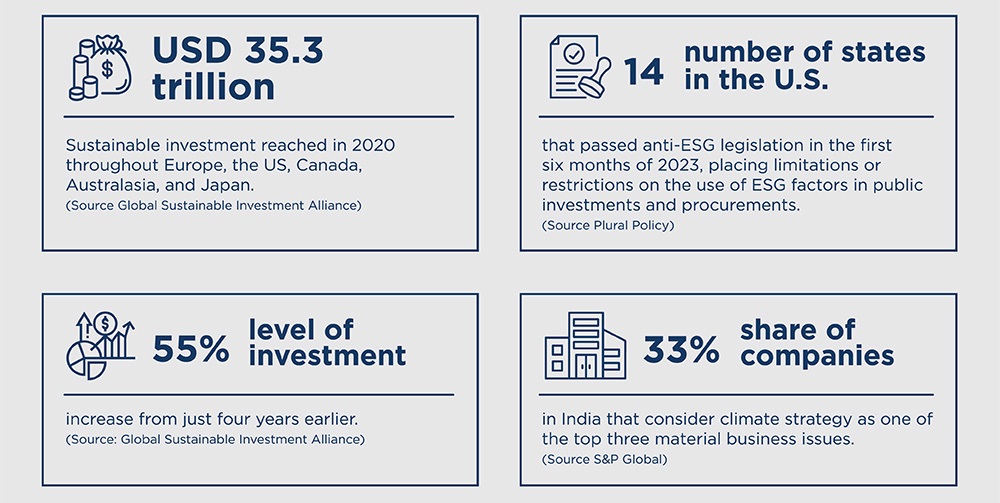

The extraterritorial expansion of ESG laws and policies will reach a significant turning point in 2024. Investors, government regulators, and consumers are demanding greater transparency and disclosure when it comes to a company’s internal ESG policies. Companies are now putting ESG factors into business metrics reflecting material risks to the organization that, when utilized appropriately, should serve as a business improvement tool, and provide others with tracking mechanisms.

As a result, corporate strategies for implementing ESG policies will become even more vital in 2024 to a company’s long-term success. For those with a global footprint, the varying approaches to ESG enforcement will be challenging. Increasing pressure is being placed on companies regarding the operation of their supply chains and whether they meet the evolving requirements of ESG regulatory mandates. At the same time, there is a growing wave of pushback against ESG company initiatives.

Climate risk disclosure is among the most significant issues facing multinational companies and investors across the globe. Starting in January 2024, large companies operating in Europe must account for the effect of their operations on climate under the Corporate Sustainability Reporting Directive (CSRD). The directive rolls out to smaller companies over the following two years.

In the US, the Securities and Exchange Commission proposed climate-reporting rules that are expected to be adopted in 2024 – although its final form is uncertain. The proposed rules mandate disclosure of more information about a company’s climate-related risks, financials, targets, and greenhouse gas emissions. Essentially, companies will have to disclose the effect of climate change on their operations as well as the potential impact on profits.

The state of California has adopted SB 253, the ‘Climate Corporate Data Accountability Act,’ and SB 261, the ‘Climate- Related Financial Risk Act.’ SB 253 requires public and privately held companies with annual revenues greater than USD 1 billion doing business in California to report on their emissions each year starting in 2026 for scope 1 and 2 greenhouse gas emissions and scope 3 starting in 2027. SB 261 requires companies with annual revenues of USD 500 million or more to start disclosing climate financial risks on January 1, 2026, and biennially thereafter.

With the various and sometimes conflicting ESG mandates coming into effect, companies with cross-border operations and supply chains will have to make sure they are meeting the sustainability standards in each jurisdiction.

Currently, countries within the EU and elsewhere have differing ESG laws and directives. France’s legislation, for instance, applies to companies with more than 5,000 employees in subsidiaries, or more than 10,000 workers in direct and indirect subsidiaries. By contrast, Germany requires companies with as few as 1,000 employees in that country to engage in environmental and human rights due diligence as of January 1, 2024. In any case, the EU’s CSRD and Corporate Sustainability Due Diligence Directive – if fully adopted in 2024 – will synchronize ESG laws in EU countries when it takes full effect.

Meanwhile, India’s Business Responsibility and Sustainability Reporting (BRSR) Core mandates ESG disclosures for the top 1,000 listed companies on the Securities and Exchange Board of India. The BRSR Core includes India-specific considerations including job creation in smaller towns, wage distribution by location, and value chain information.

Not everyone supports corporate ESG policies. Several attorneys general and state treasurers in the US have questioned corporate reliance on ESG factors, rather than on shareholder profits, when making investment decisions on state pension funds. Separately, some investors have filed lawsuits stating that ESG goals, and the use of ESG mutual funds or divestment from fossil fuel investments, were inconsistent with the fiduciary duty to obtain the best possible return on investments.

Conversely, some US states, such as New York, are requiring state retirement funds to transition portfolios to net zero emissions, apply minimum standards for climate action, develop evaluation tools for ESG, and formally integrate climate risk assessment into the investment process. Furthermore, new litigation around directors’ liabilities for failing to follow their statutory ESG duties is starting to appear and may grow more widespread.

The CSRD will require companies to have their sustainability reporting independently audited and certified starting in 2024. The goal of this new reporting mandate is to curb “greenwashing,” the growing practice by companies of overstating their sustainability metrics. Additionally, in the UK, the Financial Conduct Authority is proposing new rules on greenwashing to ensure ESG claims by companies and financial firms stand up to scrutiny, consumers are not misled, and there is effective competition.

More substantial penalties may be levied in 2024 against companies that violate ESG laws and policies, as evidenced by recent notable examples. The US SEC created an ESG Task Force and has imposed fines against companies such as Brazilian multinational mining giant Vale, which agreed to pay USD 55.9 million for ESG violations. Financial firms – such as the asset management arm of Goldman Sachs and BNY Mellon Investment Adviser – also paid penalties of USD 4 million and USD 1.5 million, respectively. Deutsche Bank subsidiary DWS Investment Management Americas, Inc. agreed to pay a USD 19 million penalty for greenwashing violations in which it made misstatements about its ESG investment process.

ESG commitment has resulted in stronger corporate performance, according to a study by the NYU Stern Center for Sustainable Business which examined the relationship between ESG and financial performance in more than 1,000 research papers from 2015 to 2020. Additionally, accurate and transparent ESG-related disclosures that meet regulatory requirements are helping to bolster company reputation, while also helping to avoid litigation driven by regulators and pro-ESG shareholders.

As the US and EU work to build strategic political partnerships with developing countries in Africa, South America, and Asia to secure future supply of critical minerals, the environmental and social components of ESG are particularly significant. Advanced technologies require more natural resources from developing countries – such as Indonesia or the DRC – to meet growing demand. Consequently, extractive industries and their buyers have an opportunity to apply ESG principles throughout the supply chain. Companies that participate in the global mineral marketplace may seek to reduce corporate risk associated with mineral resource development and usage by strengthening ties with the local communities and addressing local issues and grievances associated with development.

While ESG regulations are facing backlash in some regions, carbon reduction goals are also creating new opportunities for companies engaged in green and renewable energy projects and technologies. In the US, for example, the Inflation Reduction Act provides USD 369 billion for clean energy and climate-related projects. At the same time, the EU is attempting to transition to climate neutrality through its Modernisation and Innovation Funds.

In the World Economic Forum’s Global Risks Perception Survey 2019-2020 of its members, the WEF found that environmental issues accounted for five of the top 10 economic risks in both likelihood and impact over the next decade. Despite opposition to ESG in certain areas, investors, shareholders, consumers, and even employees are increasingly recognizing the value of companies committed to sustainability and related goals. Companies that start early to utilize ESG data and reporting will ensure that proper risk management and governance processes are in place and can expect to gain a competitive advantage.

If you have any questions or would like to further discuss the risks and opportunities outlined in this Featured Topic, please email [email protected].

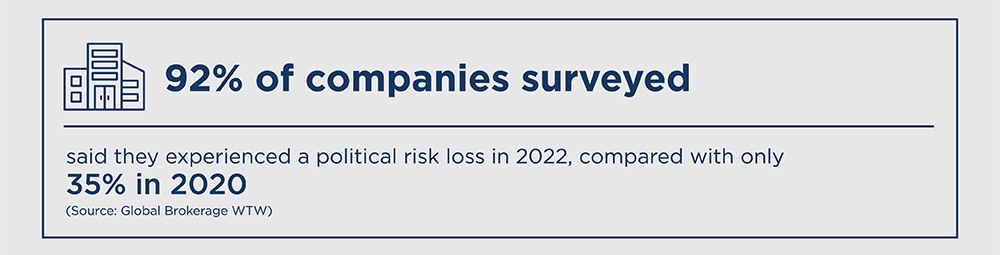

All investments are subject to shifts in business climate and geopolitics and the whims of the investor and host government alike. For global businesses in 2024, government intervention is increasingly a real and critical concern that must be recognized and addressed. This can include greater state control over the investment itself (up to outright expropriation) or other demands from the investor that rebalance the economics of the investment, such as higher royalties.

Businesses investing abroad will need to stay aware of the prevailing political trends and be alert to early warning signs that an investment environment may change - for the better or worse.

The risk of sudden radical actions by governments increases during politically fraught times, such as ahead of competitive elections. Although autocratic rule can bring stability, a swing to a more autocratic or nationalistic regime could increase the risk of hostile actions. This is especially true if investor-state tensions are already high and/or the government is looking to bolster its legitimacy with an appeal to the national interest.

Some governments may be tempted to deflect any resulting discontent among the population toward “greedy” foreign investors, exacerbating any difficulties the investor is already experiencing in convincing locals of the benefit of its investment.

Governments facing financial pressure could be more tempted to increase their revenue intake from foreign investors. Examples include a government struggling to balance its budget or experiencing a fall in foreign exchange reserves. At a minimum, the risk of the government revoking or failing to honor contracts with foreign suppliers will increase.

Where there are tensions and heightened geostrategic competition between the host government and the investor’s home jurisdiction, areas of increased risk will include sensitive sectors such as critical minerals, AI, energy storage, and related technology (e.g., the "internet of things").

Restrictions on social media usage may also be possible especially as AI becomes more powerful, heightening the threat from geopolitical adversaries in so-called “information wars.”

Beyond the most obvious, direct forms of investment protection, such as bilateral investment treaties, investors may get further reassurance from concrete indications of firm bilateral co-operation, such as free-trade agreements. This, coupled with a jurisdiction’s track record in maintaining relative rule of law and generally staying “above the fray” of the current geopolitical fracturing, could lessen the risk of an investment getting caught up in any geopolitical dispute. Sometimes, however, investors may reason that the potential return on investment outweighs the risk of investing in less stable jurisdictions and/or in highly sensitive sectors. Extra preemptive steps to protect their investments could include:

The high demands for minerals essential to the energy transition mean investors need to make themselves stand out. Many commodity producers are seeking commitments from investors to add value downstream, such as in processing and manufacturing, as well as extraction. Becoming indispensable in this manner can help curb any temptation by the government to derive greater value from investors in other, more intrusive ways.

Commodity or critical metal-producing countries that have strong political and trading / investment relations with one’s host country or its allies are safer investment choices than in jurisdictions more hostile to the West. The US and EU are notably increasing policy and financial support for critical minerals and related industries.

Tariffs and other protectionist measures and increased state involvement (in cooperation with investors) are far more common than the most aggressive forms of government intervention, such as forced divestment and outright expropriation.

Businesses committed to and skilled at taking the needs of local communities and governments into account and listening to their concerns will usually be better placed to allay any issues as they arise, compared with peers who disregard local sentiment.

Before reacting instinctively to hostile rhetoric by officials, investors should consider that politicians – especially at politically troubled times – may speak rashly to boost their populist credentials without any intention of acting on their words. The media also has a tendency at times to sensationalize greater government intervention and make plans appear more onerous and hostile than they may be in practice. A nuanced understanding of the political landscape and outlook, and with the likely trajectory of planned legislation, will therefore be essential and advantageous.

There is likely to be increased demand for policies covering expropriation – including creeping expropriation such as increased tax rates – as well as contract frustration, war, and violence risk.

One example of government intervention is illustrated by the ongoing litigation stemming from asset seizures and forced discounted sales in Russia. Similarly, lawyers specializing in IP and corporate restructuring / re-domiciliation can expect increased demand for their services.

If you have any questions or would like to further discuss the risks and opportunities outlined in this Featured Topic, please email [email protected].

We would like to thank our experts for their contributions in the inaugural J.S. Held Global Risk Report.

For more information, contact [email protected].

This communication may contain forward-looking statements. These statements are based on J.S. Held’s current expectations and are subject to risks, uncertainties, and other factors that could cause actual results to differ materially from those expressed or implied by such forward-looking statements. Forward-looking statements speak only as of the date they are made, and we undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events, or otherwise. This material is for informational purposes only and is provided ‘as is’ without any warranties and J.S. Held assumes no liability for errors, omissions, or any actions taken based on this material.

Our experts provide commentary and analysis on the October 2023 attack by Hamas on Israel, and how recent events will effect the rest of the Middle East and beyond....

This article focuses on the obstacles facing the UK and EU in meeting their goals of constructing more renewable energy projects, enabling them to significantly reduce greenhouse gas emissions. It examines the growth of renewables...

Innovations in AI and machine learning can aid forensic investigation procedures, advancing the detection of fraud & other financial threats....