Insights

J.S. Held Acquires Shechter & Everett to Expand Forensic Accounting Capabilities for Family Law Disputes in Florida

Read MoreWhilst the United Kingdom (UK) no longer forms part of the European Union (EU), it remains part of Europe and still adopts common policies that were previously put in place. In fact, the UK energy sector is synonymous with its EU counterparts.

Whether Europe is on track to meet the 40% renewable target is not clear, particularly amidst the current uncertainties associated with dominating events, such as post-pandemic supply chain issues, fossil fuel supply reductions, and adverse weather. More notably, in response to Russian dominance, the EU has increased that target to 45% renewable energy by 2030.

This article focuses on the obstacles facing the UK and EU in meeting their goals of constructing more renewable energy projects, enabling them to significantly reduce greenhouse gas emissions. It examines the growth of renewables, the REPowerEU Plan of 2022 created to diversify Europe’s energy sources in response to the Russia / Ukraine conflict, the future of nuclear power, and the continued role of coal.

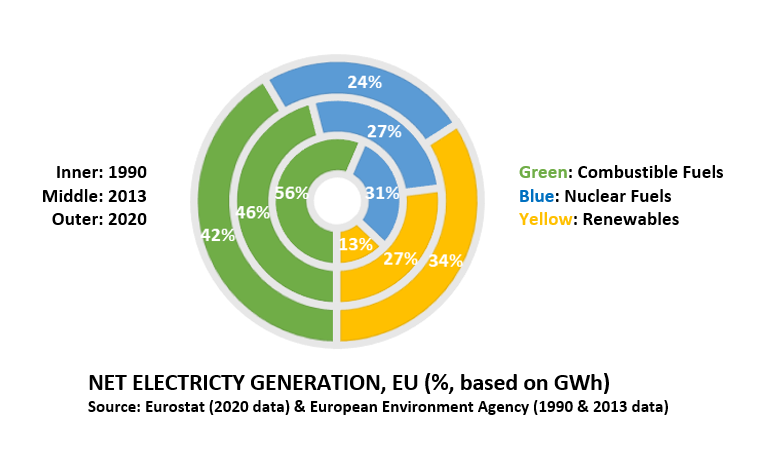

In the three decades between 1990 and 2020, the reliance on combustible fuels has dropped from 56% to 42% of the total energy generated in the EU. What appears more dramatic though, is the progression toward more renewable energy sources. Interestingly, by 2020, the proportion of energy produced by renewable sources, outstripped the proportion produced by nuclear sources in 1990.

The Fukushima accident in 2011 may have contributed to the decommissioning of nuclear power plants since then. Other differences might be explained, in part, through increasing awareness of climate issues and global commitments such as the Kyoto Protocol (1997), the goal of which is to reduce greenhouse gasses by 5% globally. Comparatively, the current initiatives driving the growth in renewable energy sources across Europe, are as follows:

Renewable energy remains a major growth industry driven by the directives above. In 2021, the EU alone consumed around 2,664 Gigawatt hours (GWh) of energy, of which approximately 15% is produced by wind turbines and a further 14% by hydroelectric projects, the latter of which is accounted for in renewable energy targets in the EU. The balance of renewable energy production is from solar and geothermal energy sources.

In 1982, the first wind turbines manufactured in Europe were delivered to California, at the same time a 5-turbine wind farm was installed on the Greek island of Kythnos. Since then, around 255 Gigawatts (GW) of wind farm capacity has been installed in the EU by 2023, which based on 1980’s technology, would require around 12.8 million of the 20-kilowatt (kW) turbines that were installed on the Greek island, such was the technical challenge faced at that time.

The UK, Germany, and Denmark led the way in supporting various EU wind farm projects, but it was German and Danish manufacturers that developed wind turbine technology that really unlocked the path forward.

What the German and Danish manufacturing models show is that the capacity of installed wind farms correlates with the advancement in turbine ratings. As Europe’s wind farms are 81% onshore, this means that rather than installing millions of wind turbines, a more reasonable approximation of 46,000 turbines would be required across Europe to provide the same 236GW capacity, based on current average turbine ratings.

Approximately 64% of the wind capacity in Europe is in five countries: Germany (64GW), Spain (28GW), the UK (27GW), France (19GW), and Sweden (12GW). Given the geographical advantage of being an island with plenty of coastline, the UK has a balanced split between onshore and offshore projects. Only the Netherlands, Denmark, and Belgium have similar profiles.

The technical difficulties in manufacturing and installation associated with offshore wind farms appear to have been largely overcome, thus opening the door to further offshore projects in the future. However, forecasters predict that onshore projects across Europe will remain prevalent.

On 6 March 2021, Denmark’s wind farms generated 98GWh, which was 99% of the energy consumption of Denmark that day. Over a typical year, the wind energy contribution averages approximately 44% of the country’s total energy consumption. Given that the EU has set a 40% renewable target by 2030, Denmark is meeting its target, which may explain why it ranked only eighth on the list of new installations (by Megawatt (MW)) in 2021.

Across Europe more generally, 15% of the annual energy consumption is met by wind farms. Accounting for other forms of renewable energy, Europe still needs to add somewhere in the range of 6% to 8% capacity to meet this renewable target. If this is to be wind energy, then around 115GW of wind farms would need to be built.

On 18 May 2022, the European Commission published the REPowerEU plan, which sets out measures to reduce dependence on imported fossil fuels and raises renewable energy goals from 40% to 45%. This means that on top of the 115GW target already established to reach 40% renewable target by 2030, Europe needs to construct a further 80GW to achieve 45%, meaning a total combined additional 195GW by the end of the decade.

In 2021, around 17GW of wind farm capacity was commissioned, which if repeated over the next eight years would add around 136GW of capacity by 2029. In order for the EU to meet the new REPowerEU plan, Europe will be required to commission at least 24GW capacity year on year. Forecasters predicted that 21.9GW of new installation was possible for 2022 yet only 16GW was achieved (although this was likely caused by slow regrowth in the construction market and global supply chain disruption as a result of the COVID pandemic and the war in Ukraine). More realistic predictions are that less than 120GW will be added by 2029.

Although the current focus is on building more and building bigger, there is the sleeping giant of the age of the installed network. The Kythnos wind farm was commissioned 40 years ago, this year. Given that turbines only have a 20 to 25-year lifespan, the industry needs to respond to the increasing maintenance costs and possible decommissioning. For every decommissioned turbine, capacity is removed from the network. Fortunately, the early turbines are lower capacity, and as a result, it is more likely they would be repowered than fully decommissioned. However, given that the turbine capacity reached around 4MW some 15 years ago now, the task of decommissioning will be a future headache for Europe.

Over the last several years, solar has overtaken wind as the main renewable energy industry in Spain. Although it is facing issues with network capacity, solar is also creating an interesting scenario in which energy prices plummet during daytime to close to 0 Euros per Megawatt hour while rising to extremely high rates during early morning hours or when there is no sun. This may only become more common in coming years.

In 2020, the EU produced only 42% of the energy that it consumed domestically, with the remaining energy coming from imported sources in the form of carbon-based resources – natural gas, crude oil, and coal. Specifically, 24% of the EU’s total energy needs originated in Russia, which included 46% of the EU’s natural gas imports, 26% of crude oil imports, and 53% of its hard coal imports. The balance – some 33% of the EU’s required energy – was produced from trading with countries outside the EU. The REPowerEU plan aims to reduce its dependence on Russian imports as well as its reliance on both nuclear and fossil fuel energy sources.

Finland’s newest nuclear power plant opened in May 2023, albeit its original completion date was 2009. Likewise, France’s 1,600MW Flamanville nuclear power plant’s original date to be operational has been pushed back to 2024, representing well over a decade of delays and a predicted overspend of $13 billion. These delays are, of course, problematic to investors, but perhaps welcomed by those who opposed nuclear power in the first place.

However, Europe has now had to consider “energy security” and this means promoting domestic solutions, such as bringing online nuclear power stations sooner. This is in direct conflict with the European Commission’s directive which left out nuclear power completely. Nearly half of the nuclear power stations in Europe are within France, and the next 13 new-generation reactors are not expected to come online until at least 35 years’ time. The concentration of nuclear power in France and the timescale associated with the development of nuclear power as a response to the Russian situation does not fit within the green deal. Therefore, Europe must push on with its renewables programme instead.

The EU’s “fit for 55” plan is an extension to the current proposed target of 45% to 55% renewable energy by 2050. The expectation is to significantly reduce natural gas consumption. However, commentators expect that due to the Russian situation, reducing gas supplies in a transitional period until other sources can be found, will mean that Europe will need to burn coal for a little while longer than expected.

This is evidenced by Germany’s recent decision to trigger stage two of its three-stage emergency plan, which involves reverting to burning coal for the production of energy. This decision appears to be unusual because gas storage levels in Europe are currently running around the average of what is expected for this time of year. If the same situation had not led to burning coal in previous years, then something else must be at play. As it turns out, the weather patterns in Europe are becoming more difficult to predict. This has resulted in Germany considering the impact that weather has on its energy infrastructure. Specifically, the level of water in the Rhine River becomes important as this is the key distribution channel for coal to Germany’s power plants. According to Bloomberg, the water level is already at 117 cubic meters per second (cms) triggering a “low water” alert and, if it drops to 80cms, it curtails traffic; and at 40cms it becomes impassable. Germany is therefore hedging the risk of a poor winter by burning coal, while holding gas storage levels.

In a similar way, the Meuse River water levels in France may lead to shortages in production at France’s largest nuclear power plant too. Interestingly, the issues that limit the use of nuclear power stations and prevent transport of coal in Europe are climatic effects. Ironically, the changing climatic conditions were essentially the catalyst for the advancement of renewable energy in the first place.

Europe continues to fall behind on its commitments of 40% renewables by 2030, and clearly even further behind the REPowerEU plan of 45% renewables. The EU has, as a result, committed to an extra investment of $221 billion between 2022 and 2027 to help achieve these goals. Other commentators suggest that investments in the range of $750 billion by 2035 may be necessary. This arguably makes renewable energy projects recession-proof, as the commitment is already there and has been for several decades.

In terms of construction, the industry is still recoiling from post-pandemic sluggishness. Supply chain issues are not likely to ease soon, and given that, high inflationary pressures will continue. However, the energy industry will see many new renewable energy projects out for tender in the next five years to meet the 2030 target.

We would like to thank Mark Mills, Enrique Abiega, and Garrick Jefferys for providing insight and expertise that greatly assisted this research.

Mark Mills joined J.S. Held in April of 2023 as part of J.S. Held’s acquisition of Aquila Forensics. As a Senior Managing Director in the Construction Advisory practice, Mark brings more than 20 years of experience in the construction industry working for sub-contractors (civils), main contractors, professional quantity surveyor (PQS) firms, and multi-disciplinary consultancies. He has been involved with many complex disputes including infrastructure developments (predominantly road and rail), marine developments, hospitals, large defense projects, major international airports, residential schemes, several hotels, luxury private residences, stadiums, and a film production studio. He has provided expert opinion and technical advice to a wide range of clients in litigation, mediation, arbitration, and negotiation matters. A member of the Royal Institution of Chartered Surveyors (MRICS), Mark specializes in managing and resolving construction disputes. He is also a member of the Chartered Institute of Arbitrators (MCIArb) and a member of the Society of Construction Law.

Mark can be reached at [email protected] or + 44 20 7072 5107.

Enrique Abiega is a Senior Managing Director in the Construction Advisory practice of J.S. Held Iberia, S.L. in Madrid. With a background as an industrial engineer, he has more than 19 years of international experience in dispute resolution / expert witnessing, contract and claim management, insurance claims, project management, and business development in the energy, engineering, construction, and infrastructure sectors. He has acted as lead expert witness in arbitration cases in Europe, Latin America, the Middle East, and Africa in construction and engineering projects, including, infrastructure, oil & gas, mining, and industrial plants, among other sectors. His matters include cases in ICC, ICSID and several other international and local institutions and giving oral testimony in Spain, Mexico, Chile, Peru, Argentina, Colombia, the United Arab Emirates, and more.

Enrique can be reached at [email protected] or + 34 91 917 5055.

This article discusses practical steps for implementing an ESG program....

In mid-November 2022, the European Parliament adopted the Corporate Sustainability Reporting Directive (CSRD), a major expansion of the 2014 Non-Financial Reporting Directive (NFRD). The new rules will quadruple the number of companies required to provide...

This article discusses possible ways to leverage the EU’s REACH and EMA regulations for product stewardship and reaching sustainability goals....