Melissa Impastato, LEED AP Melissa leverages her expertise in builder’s risk claim evaluation to clarify how general conditions should be distinguished, measured, and validated in complex loss scenarios.

Matt Weismuller, PE Matt draws upon his background in construction planning and scheduling to explain how general conditions should be assessed across repair and delay periods in builder’s risk claims.

Megan Rac Megan applies her experience in construction scheduling and damage evaluation to show how delays and time-driven impacts inform the treatment of general conditions in builder’s risk analyses.

Overview

When there is a change in project scope or work duration, a general contractor or construction manager typically claims additional general conditions. These costs are developed in one of several ways: (1) as a percentage of the total cost of a change order, (2) calculated using a preset contract rate, or (3) as actual incurred costs directly resulting from additional contract work.

In a builder’s risk claim, the policy, not the construction agreement, will determine entitlement for a policyholder to be reimbursed for claimed general conditions costs. Prior to undertaking the review of claimed general conditions costs, it is important to gain clarity from the adjuster and insurer(s) regarding covered general conditions expenses, and to follow these instructions during the review. The following is intended to summarize our experience reviewing additional general conditions costs in a builder’s risk claim.

A general contractor will often submit a builder’s risk claim, subject to the contractual guidelines for a change order, which may arise during the course of construction. After a loss, this involves first establishing the scope of work related to the loss event, then assembling pricing to make repairs to damaged property that is the subject of the construction contract. Very often, the general contractor will claim costs for the “additional time” that their staff spends managing the claim and loss-related repairs. However, one major difference often seen in the claims world relative to a typical construction change order is that a contractor’s claim may include general conditions expenditures, which, although arguably necessary, are not demonstrated to be incremental or quantifiable increased costs to the overall construction project. General conditions costs that appear to be either duplicative to the original construction costs and/or not incurred are often not compensable by the insurer(s). The intent of the builder’s risk policy is to provide coverage that will indemnify or make a policyholder whole, but not put them in a better position. A general contractor who repairs a property loss in conjunction with performing base contract work may not incur an incremental increase in their cost as a result of the loss event. Since a large component of general contractor expenses consists of salaried staff, time spent managing the claim during the period of repair may already be included in, and covered by, the original project’s budget. Therefore, only those general condition costs that represent actual incremental increases to the overall project should be considered in a builder’s risk claim.

In the event of a delay in the project’s completion caused by or resulting from a loss, the actual increase in general conditions expenses may be incurred during the delay period and are not incurred for making physical damage repairs. In such a case, the issue of whether these expenses are compensable under a builder’s risk delay endorsement (or similar delay coverage) requires a determination by the insurer.

The evaluation of general conditions can be a common source of disagreement during the claims process, and this paper seeks to clarify which types of general conditions costs should be reviewed in the evaluation of a builder’s risk claim.

It is important to note that the analysis of general conditions is a complex topic that is typically a significant discussion point during the analysis of a builder’s risk claim. The views included herein regarding general conditions represent our opinion based on our experience as construction industry experts, having reviewed construction-related insurance claims. Thus, what follows is a helpful guideline for both insureds and insurers seeking to understand these complex issues:

Background

Before discussing the analysis of general conditions in a builder’s risk claim, it is important to establish what general conditions are and what types of costs they constitute on a construction project. General conditions are a subset of the broader category, often referred to as overhead and profit (sometimes referred to as markup, which may include general conditions and fees), which is noted in the excerpt from “The What, When & How Much of General Conditions (Overhead) and Markup (Profit)” below:

Introduction

Overhead and profit (or OH&P as it is often called) is frequently a misunderstood term. It can be the subject of misapplication and dispute, and, in connection with the alleged custom and practice in the insurance claims world, has become the subject of class action lawsuits against insurers in numerous states.

In the insurance restoration and casualty reconstruction business, OH&P is often characterized as a standard by which deviation is not possible. This, however, is untrue and indeed defies both logic and economic reality. But before we get to the discussion of the insurance custom and practice OH&P myth, we must first understand what OH&P is, and how it gets applied in the real world.

From a general contractor or construction manager’s perspective, there are two major cost categories associated with the “Cost of the Work” on any project:

Direct Costs, which are the costs necessary to furnish and install the permanent elements of the project, such as structure, exterior envelope, interior finishes, vertical transportation, mechanical/electrical/plumbing systems, etc.

Indirect Costs, which include general conditions or overhead, and markup (fee or profit), are the costs associated with the jobsite management of the project, including items such as project management staff, jobsite trailers, telephones, administrative as well as temporary roads, temporary utilities, permits, fees, general hoisting, safety, and cleaning, not specifically associated with individual elements being erected. Indirect costs can be referred to as general conditions, general requirements, or field office overhead, and can also include costs associated with and delineated in the general and supplemental conditions of the contract, and (typically) Division 1 of the specifications. These documents outline the work rules and obligations set forth and required by the contract. Markup, fee, or profit is intended to cover a portion of general and administrative (G&A or home office overhead) costs and provide profit for the contractor or construction manager. G&A costs are not associated with a specific project, but account for the contractor's business operating expenses, including estimating and preconstruction services, accounting, and marketing.

Overhead

Overhead, as it relates to a general contractor or construction manager, refers to field office overhead or general conditions/requirements, i.e., project management staff and services. This is the amount by which a direct cost estimate is increased to account for the jobsite services of a general contractor or construction manager and/or for items not specifically aligned with a specific task of work, which may be required to allow for an orderly and coordinated installation of materials needed to complete the work.

There are many forms of “overhead” type costs, which can broadly be put into the following categories:

G&A or “home office” overhead; or field office overhead, which is generally synonymous with general requirements/conditions noted above.

General requirements, which are the costs associated with Division 1 work rules that a general contractor or construction manager must follow. These are also often referred to as “general conditions” and include project management staff and supplies, temporary services and utilities, safety, and cleanup (among other items).

Profit

Profit refers to the markup applied by the contractor or construction manager to the total of:

The direct cost estimate.

The general conditions/requirements estimate, and certain G&A costs.

Overhead & Profit

Together, the overhead and profit (In some contracts, such as construction management contracts, this can be referred to as “general conditions and fee”) on a project are costs added to the project’s direct cost, to account for the services of the general contractor or construction manager.

Overhead and profit will typically fluctuate with the market or the type of contract. When market conditions are not favorable to the contractor (i.e., few construction projects are being started), contractors decrease their profits to become more competitive and may take a job that will at least keep their staff busy. Overhead will be reduced as a contractor may put fewer staff on a job and will further negotiate to have subcontractors incur more of the indirect costs at no additional cost, thus lowering overhead.

Definitions

In order to understand what OH&P is, some basic knowledge of construction terms is required. The following is a list of terms (representing costs), which must be accounted for in any construction project, whether it’s new construction, insurance restoration, repair, rehabilitation, or reconstruction:

Permanent materials ‐ Materials that will become a permanent part of whatever is being constructed.

Temporary materials – Materials necessary to construct a project but are neither permanent nor reusable. An example of temporary materials might be plywood and framing used to form concrete footings.

Craft or trade labor – Skilled and unskilled labor used to install (and support the installation of) materials.

Disposable tools and equipment – Small tools and equipment necessary to install materials that may not be reusable (i.e., small tools, saw blades, etc.).

Re‐usable equipment – Equipment used to support the installation of materials. These can be as insignificant as a rolling scaffold and as large as a tower crane.

Subcontractor – Trade contractor responsible for handling a single or a small number of trades. Subcontractors typically hire the skilled and unskilled labor that is required to install materials they are “contracted” to install. They supply the equipment and supervision necessary to coordinate the installation, direct costs and overhead, and “mark up” their costs to account for their own risk and to meet their profit requirements.

General contractor – Responsible for planning and coordinating the work of tradespeople, general contractors may self‐perform certain work and are contracted directly to the owner. They hold and are responsible for entering into subcontract agreements for trade work.

Construction manager – Typically provides the same services as a general contractor, does not typically self‐perform work, and is the “agent” of the owner. In certain circumstances, a “CM” may not hold the subcontract agreements.

Direct labor cost – The hourly (or daily) amount paid directly to craft/trade labor.

Fringe benefits – Costs (which are often applied to each hour worked) that are typically provided by an employer or required by union collective bargaining agreements, to be paid directly to the labor union.

Labor burden – Costs borne by the contractor (or subcontractor) for each hour (or day) that a craft/trade laborer is paid. These include such costs as workers' compensation insurance, social security taxes, disability, Medicare taxes, etc.

General & administrative or home office overhead – Costs of running the subcontractor’s, general contractor’s, or construction manager’s business.

Profit/fee – Usually reflected as a percentage (but sometimes a fixed amount), which represents the subcontractor’s, contractor’s, or construction manager’s compensation for completion of the work.

Construction contingency – A factor, sometimes applied by a subcontractor, contractor, or construction manager to account for risk and/or non-quantifiable (but required) scope of work.

Remembering that two elements go into the cost of any construction project (direct and indirect costs) and understanding what costs go into each of these categories will help to define exactly what OH&P really is. For example, say a subcontractor is to furnish and install the following scope of work:

Procurement of HVAC air handlers, condensers, controls, ductwork, etc., based on the project requirements. This material may include waste factors for certain materials (wire, sheet‐metal, conduit, etc.).

The subcontractor will include the cost of furnishing, installing, and delivering equipment and appurtenances; labor, including direct, fringe and burden, to set and pipe the equipment; supervisory labor; materials and equipment (i.e. the general conditions and requirements necessary for the sub to complete its work if not provided by the general contractor/construction manager); insurances; certain home office overhead; and profit.

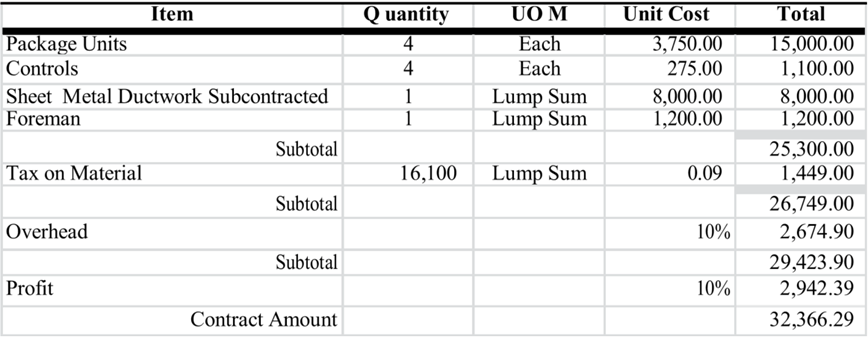

The HVAC subcontractor might express costs as illustrated in Figure 1, below:

Figure 1

Note in the above example that sheet‐metal ductwork is “subcontracted.” A subcontractor can “subcontract” out portions of the work to other contractors, sometimes referred to as “lower tier” or “sub‐subcontractors.”

In the case above, the sheet‐metal subcontractor will approach pricing for their part of the work in the same fashion that the main subcontractor did. Therefore, in looking at the sheet‐metal cost of $8,000, this sub‐subcontractor includes costs that account for their own overhead and profit. Indeed, the sheet‐metal sub-subcontractor is no different than the manufacturer of the equipment, the distributor of the equipment, the trucker of the equipment, etc. The entire supply chain is motivated by profit, and all along the way, everything is marked up by an amount sufficient to cover costs, plus an amount beneficial to the entity for being in business.

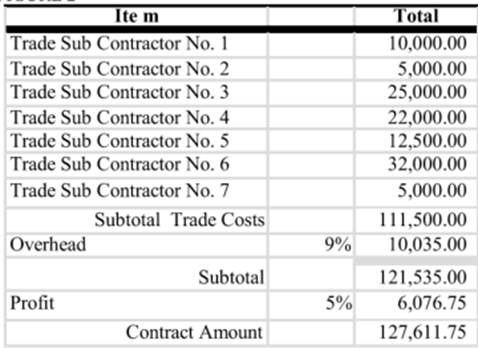

Now let’s add to the hypothetical project and assume that it has numerous trades such as concrete, steel, glass and glazing, drywall, finishes, mechanical, electrical, plumbing, and fire protection. Each trade subcontractor and each lower-tier sub‐subcontractor will have marked up their portion of the project with the cost to cover their general conditions/overhead and profit. When there is a general contractor or construction manager on the project, the subcontract trade costs are added up, and the general contractor/construction manager will add its own costs.

Figure 2 illustrates costs that are typically marked up in a similar fashion by the general contractor or construction manager, wherein they layer their own overhead, plus the desired profit margin, on top of the direct subcontracted costs.

Figure 2

Thus, any construction project can have numerous layers of overhead and profit, from sub‐subcontractors to subcontractors to construction managers.

Insurance Repair Costs and Markups

In the world of insurance repair, costs for projects that are estimated and agreed generally follow the format that applies unit costs to a quantified scope of work, then applies costs for overhead and profit where applicable.

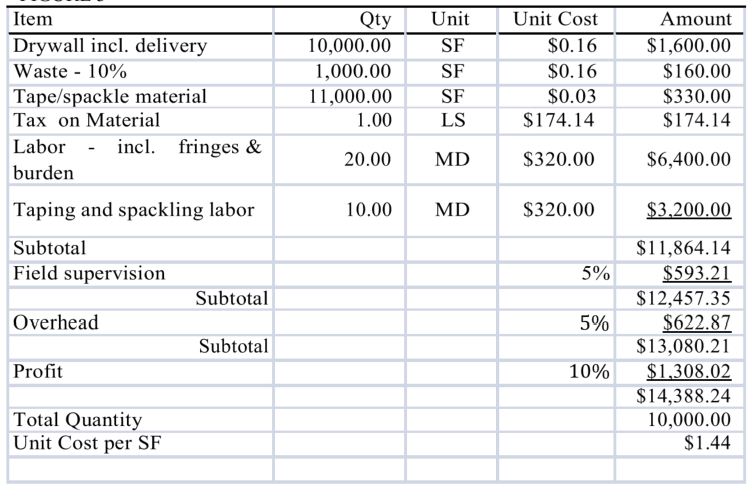

The unit cost is typically an expression of the trade subcontractor’s expected price to perform a scope of work, including all categories of costs noted in Figure 1, herein. A unit cost is typically established as described below in Figure 3, which illustrates how a drywall contractor might price the installation of 10,000 ft2 of drywall. Note that waste factors and sales tax on material are included in the unit price derived in Figure 3, although this may not always be the case.

In establishing the unit cost, the subcontractor makes the following computations, some of which require judgment based on experience:

Total quantity of required materials, including waste.

The cost of labor.

The expected productivity rate for the installation of materials, which can change job‐by‐job based on site conditions, complexity of the work, etc.

The risk factors of estimating errors or unknown conditions.

The state of the construction market at the time (i.e., how busy is the contractor, how much does he or she “need” or “want” the job, etc.).

Figure 3

We have now described what is included in both the establishment of unit costs for construction trades and the costs that a general contractor or construction manager requires to coordinate the trades and make a profit. The next step is to determine two things:

When is a general contractor or construction manager required?

How much OH&P is reasonable?

Evaluation of General Conditions in a Builder’s Risk Claim

Historical Policy Guidance in the Evaluation of Claimed General Conditions

While general conditions are often well defined and understood to be a specific type of cost in the construction industry, and are often defined in contracts, they often create confusion in the context of an insurance claim. Builder’s risk policies are typically clear when it comes to defining the various types of costs allowable. These can include hard costs, extra expenses, delay in completion costs, etc. One of the main difficulties in assessing claimed general conditions costs is that, depending on the unique circumstances of each claim, they can appear to fall into multiple different categories of allowable costs based on the policy language. This section will discuss some typical scenarios often encountered in claims submissions, followed by our methodologies for analyzing these types of costs.

Typical Scenarios When Evaluating General Conditions

Scenario 1 – A Claim for General Conditions During the Period of Repair, and There Is No Delay to the Project Due to the Claimed Event

It is not uncommon that a contractor will submit general conditions as a percentage of the repair cost during the period of repair (not the period of delay). In many cases, claimed general conditions costs are not an incremental increase to the overall project, meaning that there were no staffing and indirect expenses that went above and beyond what was already included or planned for in the construction agreement for contract work. In these cases, a request for additional general conditions is typically excluded, particularly because it would represent a windfall to the contractor who has not “incurred” any additional expense. In the event the contractor was named as an additional insured under the policy, the result of considering such costs would constitute enrichment.

An exception to this case comes in the event that a contractor either adds staff specifically to manage the loss-related repairs or if the contractor elects to keep certain staff on the project longer than planned in order to manage the repairs. These cases are more straightforward to analyze because the insurers will likely view this as an incremental increased cost that would not have been incurred in the absence of the loss event (unless it was determined that other non-loss-related delays necessitated additional staff and other expenses). In these cases, if the contractor incurred incremental general conditions, and those costs are directly necessary and related to repairs required by a loss event, then those costs may be considered compensable.

Scenario 2 – A Claim for Extended General Conditions During the Period of Delay Only

If these claimed costs would not have been incurred but for the loss event, these are legitimate general conditions (defined as “extended” general conditions when there is a delay), and we would typically measure these costs in our analysis. These are time-element related costs that require a critical path schedule analysis, and the time associated with the costs is the period of delay, not the period of repair. Such costs, when incurred, are subject to a coverage determination.

Scenario 3 – A Claim for General Conditions During the Period of Repair and the Period of Delay

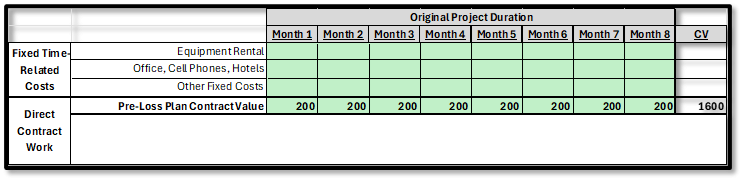

Figure 4 below shows a project’s original planned value for the contractor’s fixed general conditions cost for an eight-month project. These costs generally represent the fixed costs for the project management team to be in the field directly contributing to and managing the installation of project work. For simplicity, we have utilized a $200 general conditions cost to perform each month of planned project work.

Figure 4 – Original general conditions budget for staffing.

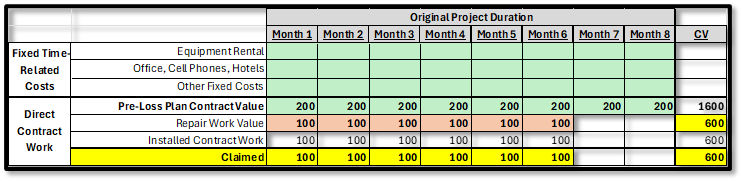

After a few months on the project, a loss event happens that requires direct repair work. Instead of being able to focus 100% on the performance of project work, the project management team now has to split its time between project work and loss-related repairs. This results in 50% of the project work being installed during the repair period, so the project management team can only complete $100 of the planned $200 in project work costs. Therefore, the Insured has reasoned that they will claim 50% of the project management costs spent during the period of repair because they were costs related to the performance of repair work. As shown in the figure below, the Insured is claiming a total $400 in such costs.

Figure 5 – Forecasted allocation of general conditions costs to loss event (start of project).

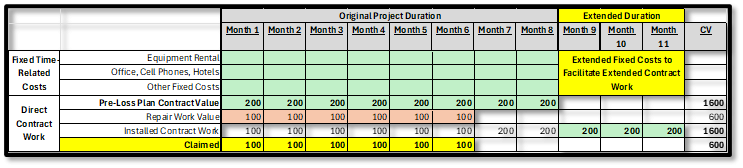

Since only half of the project work could continue being installed during the period of repair, a value of $400 in unperformed contract work is deferred beyond the POR. As the contractor was only able to work half-time on the project, the displaced project work that wasn’t performed still must be performed, resulting in a two-month extension (delay) to the project as shown in Figure 6 below.

Figure 6 – General conditions claimed costs during period of repair.

The insured has already claimed the $400 in redirected project management costs to perform loss-related repair work for Months 4 through 7 (yellow) during the period of repair. However, because of the 2-month delay, the contractor is now also claiming another $400 in “delay” costs (deferred project work costs) for Months 9 through 10 (green), for a total claim of $800, as shown in the figure below.

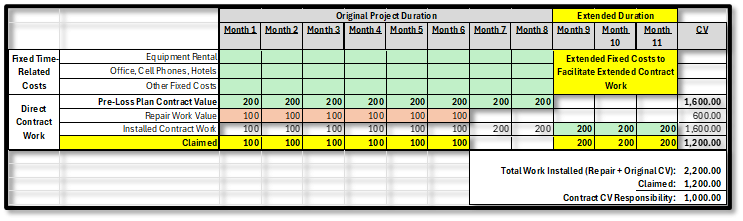

Figure 7 – General conditions claimed costs during period of repair and period of delay.

This claimed amount, if paid, reduces the contractor’s responsibility for installing/performing their original contractual budget of $1,600. By paying the Insured $800 instead of $400, the contractor has effectively had the carriers pay for $400 of the contractor’s original budget that was required regardless of the loss event (Total Work – Total Claimed = $1,200 spent by the contractor to perform all project work instead of their intended budget of $1,600. The carriers have paid for part of the Project work in addition to the repair work).

If the Contractor is going to claim an allocation of their regular project management budget during the period of repair, they would not be entitled to extended project management costs as they have already been reimbursed for the value of displaced/deferred project management work. Now they would perhaps be entitled to extended fixed costs such as office rent, cell phones, etc., but not the direct project management costs they claimed during the period of repair. The contractor’s claim for both allocated general conditions and extended general conditions is a duplicative request, and only one or the other should be claimed. Similar to Scenario 2, these are time-element related costs that require a critical path schedule analysis.

Documentation Required for the Evaluation of General Conditions

Whenever a claim for general conditions is presented, there are specific documents we expect to receive in order to validate the costs. Regardless of the types of general conditions costs presented, we will request the contractor’s pre-loss general conditions budget/estimate, owner/general contractor agreement, pre-loss pay applications, and planned staff charts. These are used to establish the pre-loss general conditions and serve as the baseline for evaluating incremental costs. They are also used to establish monthly rates to be used in measuring extended general conditions. In the case of an extended general conditions claim, which implies a delay, we will minimally also request the contractor’s construction schedules in native format in order to perform a critical path delay analysis and to establish whether the loss event caused a delay. Once a delay is measured, extended general conditions can be reviewed.

As with any claim, we present to the adjustment teams or insurers our analysis of the claimed amounts and rely upon construction experience to determine what seems fair and reasonable and what costs were actually incurred due to the delay. Ultimately, we must defer to the insurers or the adjustment team to make final decisions on what gets paid to an insured, as coverage determinations can have an impact on our analysis.

Conclusion

In summary, the goal of the analysis should be to determine the number of general conditions that are fair and reasonable. Typically, insurers are looking to understand the costs that were actually incurred. There are specific documents, such as staffing plans and pre-loss budgets for general conditions, that can assist in the valuation of general conditions for a loss event. In the absence of these types of documents, we can lean on the pre-loss daily report and contract rates to make a determination on cost. General conditions are often presented in one of a few ways: as a shift in fixed costs from owner to insurer, as an incremental cost, or as a delay-related cost.

Incremental costs during the period of repair can be legitimate. Fixed general conditions during the period of repair are not typically viewed as fair and reasonable, especially if the contractor was already getting paid for these costs by the owner (duplicative). Caution should be taken to ensure that general conditions costs are not paid for twice—once in the period of repair, and again during the period of delay. Extended general conditions are associated with a claim for delay, and a critical path delay analysis must be performed before extended general conditions can be measured.

Disclaimer: We at J.S. Held do not interpret, underwrite, or place policies. The intent of this article is to offer our expertise regarding situations such as those hypothetically described within.

Acknowledgments

We would like to thank our colleagues Melissa Impastato, Matt Weismuller, and Megan Rac for providing insights and expertise that greatly assisted this research.

Melissa Impastato is a Managing Director in J.S. Held’s Builder's Risk practice. She has been a construction professional for nearly 20 years and has extensive experience with project management, general contracting, and construction operations. Melissa’s area of expertise concentrates on construction planning and scheduling, cost evaluation, and business planning. Prior to joining J.S. Held, Melissa was a Vice President of Operations for Urban Investment Partners (UIP), a vertically integrated owner/developer/contractor specializing in multi-family investments. She also spent 15 years at Clark Construction Group, one of the nation’s top contractors as well as the largest privately held general contractor.

Matt Weismuller is an Assistant Managing Director in J.S. Held’s Builder’s Risk practice. Matt has been a construction professional for over a decade and has extensive experience with project management, general contracting, construction operations, and construction consulting. His areas of expertise include construction project planning and construction scheduling, cost evaluation and constructability. Matt offers a depth of understanding that only comes from having been intimately involved in all phases of construction: from the earliest planning and scheduling phases to the start of foundation work, and through to final inspections. This results in high-quality analysis that benefits his clients with reliable recommendations.

Megan Rac is a Managing Director in J.S. Held’s Builder’s Risk practice. Megan is an experienced construction advisory specialist with a background in planning and scheduling for major contractors, owners, and engineers. She has consulted on complex domestic and international projects, assisting contractors and owners throughout the project lifecycle to effectively manage the recovery of time and additional costs, defend against claims, and avoid formal disputes. Her expertise includes the analysis of construction damages considering the impact of design changes, change orders, delays, disruptions, inefficiencies, and accelerations. Her work in the construction arena has also involved issues such as terminations, defaults, and integration of damages within a schedule delay.

Overhead and profit (or O&P as it is most often referred to) is frequently a misunderstood term. It can often be the subject of misapplication and dispute, and in connection with the alleged custom and...

A case study illustrating considerations in insuring a renovation project under a builder’s risk policy and strategies for avoiding complications after a loss....

Read real-life builder's risk claim case studies, uncover the pivotal roles of key players, & gain insights into risk management processes that safeguard project continuity and financial stability....

INDUSTRY INSIGHTS

Keep up with the latest research and announcements from our team.