Insights

J.S. Held Acquires Shechter & Everett to Expand Forensic Accounting Capabilities for Family Law Disputes in Florida

Read MoreThis article is a tool for stakeholders involved in infrastructure projects. It conveys knowledge about the complexities of builder's risk claims, offering insights into risk management strategies, good practices, and the claims process. By presenting fictionalized real-life case studies, the article enhances understanding and collaboration among project owners, contractors, insurers, and legal professionals, enabling informed decision-making and effective management of risks and claims throughout the construction phase of infrastructure projects.

The concept of builder's risk insurance revolves around providing coverage for potential losses that occur during the construction or renovation of a building or infrastructure project. Builder's risk insurance can also cover losses caused by delays in construction projects due to covered perils, which makes it especially significant in infrastructure projects.

This type of coverage offers comprehensive protection against unforeseen and accidental damages, subject to policy exclusions and limitations. Here are the key aspects of builder's risk insurance and its significance in infrastructure projects:

Overall, builder's risk insurance plays a vital role in infrastructure projects by providing financial protection, ensuring project continuity, and minimizing potential losses and liabilities associated with construction-related damages or delays. Its significance lies in safeguarding the interests of the parties involved and supporting the successful completion of construction projects.

J.S. Held does not interpret policies or adjust claims, and the intent of the descriptions above regarding coverage and claims is general industry information

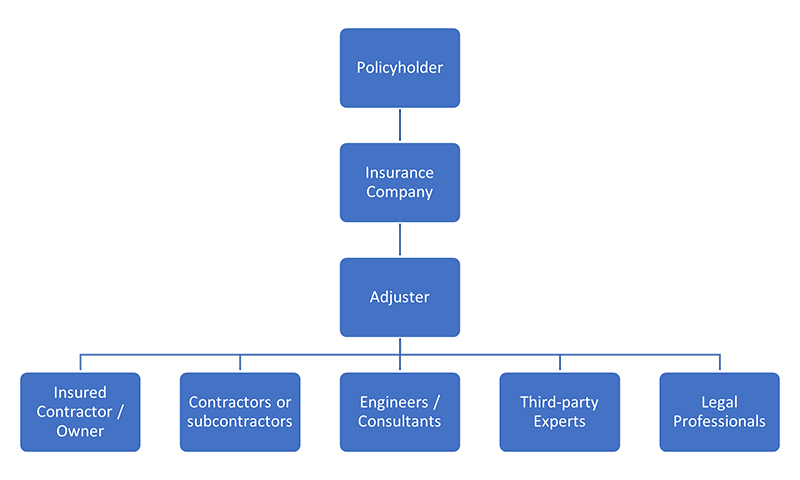

In a builder's risk claim, several key players are typically involved, each with their specific roles and responsibilities.

Navigating Through the Roles of Policyholders and Insurers

It's important to note that the specific players and their roles may vary depending on the circumstances of the claim and the policies and procedures of the insurance company. The roles described below provide a general overview of the typical players involved in a builder's risk claim. The main players in a builder's risk claim can include:

The following is a generic description of the roles and responsibilities of the involved parties in a typical builder’s risk claim to create a common knowledge base for readers to follow this paper. They, in no way and shape, can be considered a legal definition of the role of the parties.

Policyholder

The policyholder is the entity that purchased the builder's risk insurance policy and has the primary responsibility of notifying the insurance company about the claim, providing relevant documentation, and cooperating throughout the claims process. The policyholder is typically the owner or the main general contractor of the infrastructure project (insured).

Insurance Company

The insurance company underwrites the builder's risk insurance policy. They assess and process the claim filed by the policyholder. The insurance company's role includes investigating the claim, determining coverage, evaluating the damages or losses, and negotiating a settlement. In larger infrastructure projects, typically more than one insurance companies are involved (insurer(s)).

Owner / Insured Contractor

In some cases, the insured contractor or project owner may be directly involved in the claims process. They provide relevant information, documentation, and assistance to the insurance company or claims person during the investigation and evaluation of the claim. Their role may also involve collaborating with the claims person to resolve issues or disputes related to the claim.

Adjuster

The construction claims person or adjuster represents the insurance company and is responsible for handling the builder's risk claim. Their role includes assessing the claim, investigating the damages, determining liability, quantifying losses, negotiating settlements, and ensuring adherence to the policy terms and conditions. They typically retain other professionals on behalf of the insurer(s) to assist them in the loss adjustment.

Contractors or Subcontractors

Contractors or subcontractors who are involved in the construction project may play a role in the claims process. They may provide information, documentation, or expert opinions related to the damages, repairs, or delays. They may also be responsible for carrying out repairs or restoration work as part of the loss remediation.

Engineers / Consultants

Depending on the nature and complexity of the loss/claim, engineers or other specialized consultants may be engaged to assess the damages, evaluate the structural integrity, provide expert opinions, or assist in the quantification of losses. Their role is to provide technical expertise and support in the claims evaluation process.

Third Party Experts

In certain situations, third-party experts may be involved, such as forensic accountants, loss adjusters, and specialists in specific fields related to the claim. They assist in assessing the damages, determining the cause of the loss, or providing expert opinions to support the claim evaluation process.

Legal Professionals

In cases where there are disputes involved in the claim, legal professionals may be engaged to provide legal advice, negotiate settlements, or represent the parties involved in legal proceedings related to the claim.

A builder's risk claim refers to an insurance claim made to cover damages or losses that occur during the construction or renovation of a building. The anatomy of a builder's risk claim typically involves several key components:

Builder's risk claims in infrastructure projects present unique considerations and challenges compared to other types of construction projects due to their scale and complexity. Here are some factors to consider:

Obtaining appropriate builder's risk insurance coverage for infrastructure projects is crucial when considering these unique factors and increased risk factors. Adequate coverage should address the specific risks associated with the project, including the scale, complexity, duration, and environmental factors to mitigate potential financial and operational impacts.

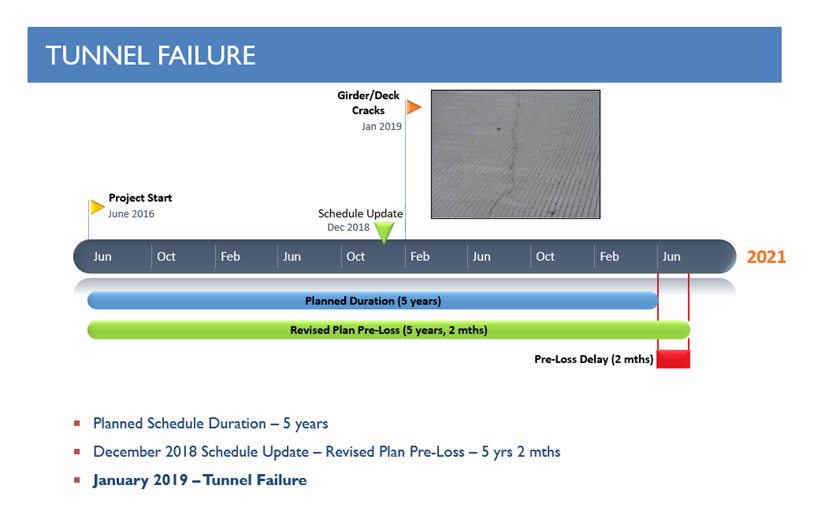

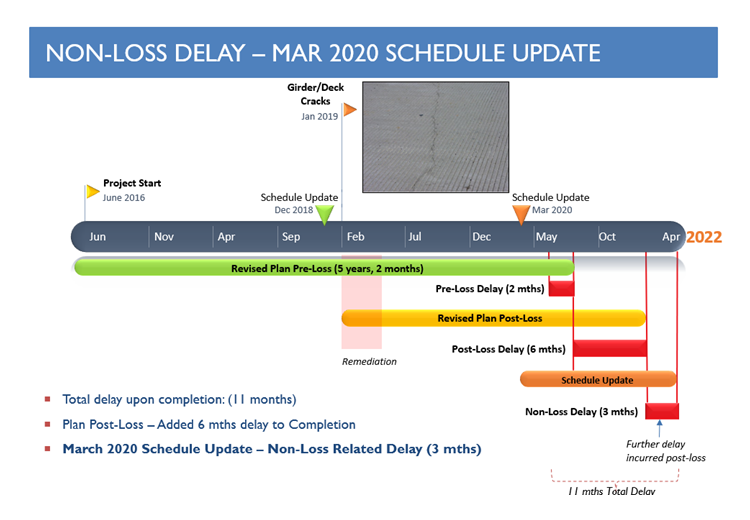

We will now look at a fictionalized case study where a major loss event occurred on an infrastructure project triggering an assessment by a forensic engineer and a delay expert to assess the claim and resultant damages.

Project Background and Overview of “Northeast Big Move”

Claim Incident

Immediate Response

Expert Evaluation

Cause of the Loss

Damages and Schedule Impact

Claims Negotiation

Settlement

Challenges and Lessons Learned

Builder's risk insurance is essential in infrastructure projects to ensure continuity of the project in case of an incident. This article reinforces the importance of understanding the anatomy of builder's risk claims in infrastructure projects and emphasizes that a comprehensive understanding of the process, key players, and unique challenges enables stakeholders to navigate claims effectively and protect their interests. It is important to work with experienced claims professionals who have expertise in infrastructure projects and who understand the unique challenges and requirements, such as:

By implementing these practical tips and good practices, policyholders, contractors, and insurance companies can streamline the claims process and avoid common pitfalls in builder's risk claims for infrastructure projects.

We would like to thank our colleagues Martin Hoey and Farhood Nowzartash, PhD, for providing insight and expertise that greatly assisted this research.

Martin Hoey is an Assistant Managing Director in J.S. Held’s Builder’s Risk practice. Martin brings over 15 years of experience in construction, insurance, and cost consulting environments to the Builder’s Risk team at J.S. Held. His expertise includes project management, project controls, project administration, contract negotiation, and commercial management of construction projects through the project life cycle stages, from pre- to post-construction. Martin possesses a comprehensive understanding of construction scope, time, and cost, supporting his ability to clarify and resolve complex issues and manage the construction claims process. Martin is a leader and independent thinker who understands the impact of unforeseen circumstances and events on the course of construction, as well as the importance of establishing “cause and effect” relationships to substantiate entitlement and liability.

Martin can be reached at [email protected] or +1 226 779 2495.

Dr. Farhood Nowzartash is a Senior Vice President and Canada Lead in J.S. Held’s Forensic Architecture & Engineering practice. He is a qualified expert witness in Civil/Structural Engineering with a specialty in the forensic investigation of complex construction claims/litigation matters, the standard of care assessment and root cause analysis. He has over 25 years of experience in structural design and construction, including reinforced and pre-stressed concrete, structural steel, formworks, and wood structures. He has been an active member in the design process of multi-story and high-rise buildings, low-rise commercial buildings, bridges, oil and gas pipelines, sports complexes, stadiums, earth shoring, and concrete shoring. In addition, he has extensive experience with forensic investigations, large-scale commercial losses, industrial losses, building systems, surface water management, structural failure analysis, seismic hazard assessment, building rehabilitation, and stress analysis of component failures using Finite Element Modeling.

Dr. Nowzartash can be reached at [email protected] or +1 416 458 2496.

Measuring delay from a loss under a builder’s risk insurance policy is perhaps the most complicated of all time element measures in the claims world. Setting aside the numerous complex issues of coverage, builders risk...

Over the course of the last two decades renewable energy has been a subject that has found its way into discussion from the family dinner table to the top of global political initiatives and policies...

While there are some similarities between Builder’s Risk and Property Damage claims, there are also numerous differences in the way they are managed and evaluated. Some questions that often arise when a claim occurs on...