Insights

J.S. Held Acquires Shechter & Everett to Expand Forensic Accounting Capabilities for Family Law Disputes in Florida

Read MoreOverhead and profit (or O&P as it is most often referred to) is frequently a misunderstood term. It can often be the subject of misapplication and dispute, and in connection with the alleged custom and practice in the insurance claims world, has become the subject of class action lawsuits against insurers in numerous states.

In the insurance restoration and casualty reconstruction business, overhead and profit is often characterized as a standard by which deviation is not possible. This however is untrue and indeed defies both logic and economic reality. But before we get to the discussion of the insurance custom and practice O&P myth, we must first understand what O&P is, and how it gets applied in the real world.

From a general contractor or construction manager’s perspective, there are only two major cost categories associated with the “Cost of the Work” on any project:

Overhead, as it relates to a general contractor or construction manager refers to field office overhead or general conditions/requirements, i.e. project management staff and services. This is the amount by which a direct cost estimate is increased to account for the jobsite services of a general contractor or construction manager, and or for items not specifically aligned with a specific task of work, that may be required in order to allow for an orderly and coordinated installation of materials needed to complete work.

There are many forms of “overhead” type costs, which can broadly be put into the following categories:

Profit refers to the mark up applied by the contractor or construction manager to the total of

Together, the Overhead and Profit on a project are costs added to the project’s direct cost, to account for the services of the general contractor or construction manager.

Overhead and Profit will typically fluctuate with the market. When market conditions are not favorable to the contractor, (i.e. few construction projects being started) contractors decrease their profits to become more competitive and may take a job that will at least keep their staff busy. Overhead will be reduced as a contractor may put fewer staff on a job, and will further negotiate to have subcontractors incur more of the indirect costs at no additional cost, thus lowering overhead.

In order to understand what O&P is, some basic knowledge of construction terms is required. The following is a list of terms (representing costs), which must be accounted for in any construction project, whether it’s new construction, insurance restoration, repair, rehabilitation or reconstruction.

Remembering that two elements go into the cost of any construction project (direct and indirect costs), understanding what costs go into each of these categories will help to define exactly what O&P really is. For example, say a subcontractor is to furnish and install the following scope of work:

The subcontractor will include the cost to furnish, install and deliver equipment and appurtenances, labor including direct, fringe and burden to set and pipe the equipment, supervisory labor, materials and equipment (i.e. the general conditions and requirements necessary for the sub to complete its work if not provided by the GC/ CM), insurances, certain home office overhead, and profit.

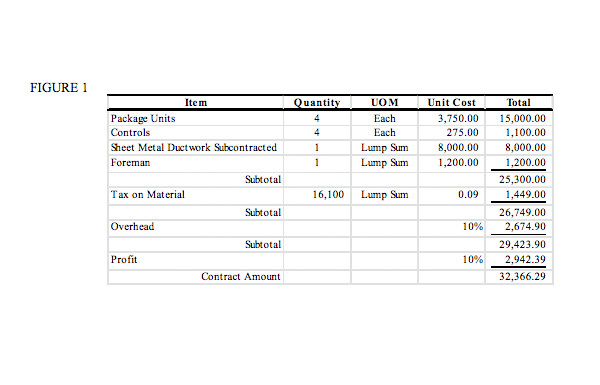

The HVAC subcontractor might express costs as illustrated in Figure 1, below:

Note in the above example that sheet-metal ductwork is “subcontracted”. A subcontractor can “subcontract” out portions of the work to other contractors, sometimes referred to as “lower tier” or “sub-sub” contractors.

In the case above, the sheet-metal subcontractor will approach pricing for his part of the work in the same fashion that the main sub-contractor did. Therefore, in looking at the sheet-metal cost of $8,000.00 this sub-sub contractor includes costs that account for their own overhead and profit. Indeed the sub-sub sheet-metal contractor is no different than the manufacturer of the equipment, the distributor of the equipment, the trucker of the equipment, etc. The entire supply chain is motivated by profit, and all along the way, everything is marked up by an amount sufficient to cover costs, plus an amount beneficial to the entity for being in business.

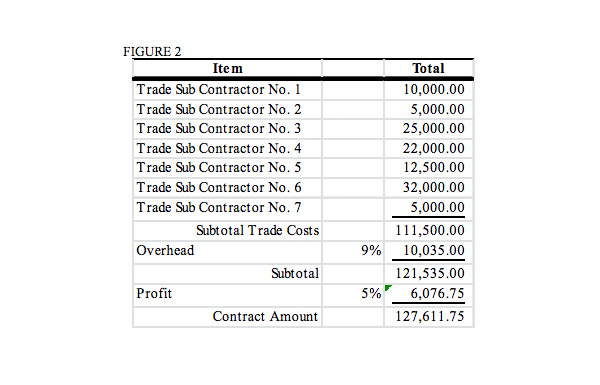

Now let’s add to the hypothetical project and assume that it has numerous trades such as concrete, steel, glass and glazing, drywall, finishes, mechanical, electrical, plumbing and fire protection. Each trade subcontractor and each lower tier sub-sub contractor will have marked up their portion of the project with the cost to cover their general conditions/overhead and profit. When there is a general contractor or construction manager on the project, the subcontract trade costs are added up, and the general contractor/construction manager will add its own costs.

Figure 2 illustrates costs that are typically marked up in a similar fashion by the general contractor or construction manager, wherein they layer their own overhead, plus desired profit margin on top of the direct subcontracted costs:

Thus, any construction project can have numerous layers of overhead and profit, from sub-sub-contractors to subcontractors to construction managers.

In the world of insurance repair, costs for projects that are estimated and agreed generally follow the format that applies unit costs to a quantified scope of work, then applies costs for overhead and profit where applicable.

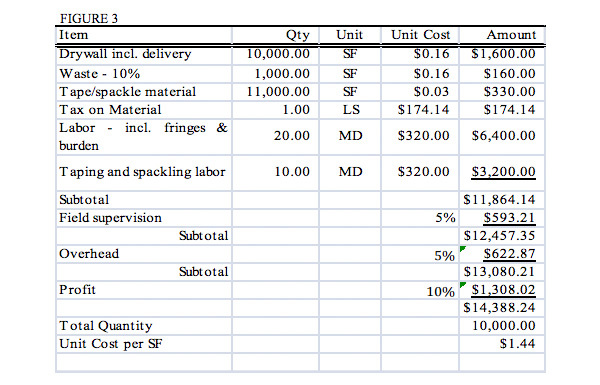

The unit cost is typically an expression of the trade subcontractors expected price to perform a scope of work, including all categories of costs noted in Figure 1, herein. A unit cost is typically established as described below in Figure 3, which illustrates how a drywall contractor might price the installation of 10,000 SF of drywall. Note that waste factors and sales tax on material are included in the unit price derived in Figure 3, although this may not always be the case.

In establishing the unit cost, the subcontractor makes the following computations some of which require judgment based on experience:

We have now described what is included in both the establishment of unit costs for construction trades and the costs that a general contractor or construction manager requires to coordinate the trades and make a profit. The next step is to determine two things:

Close your eyes and recall some of the beautiful music you have heard in your lifetime. Now, picture how each of the artists playing the instruments that make the music act in concert with one another to make the sounds you hear. Sometimes the musicians are simply left to play their instruments while at the same time being aware of what their collaborators are doing, and other times, the musicians are being “coordinated” by the person with the baton, who helps them play together in a way that produces the desired sounds. So it is with construction.

A general contractor or construction manager that does not “self-perform” trade work is nothing more than an experienced coordinator of construction projects. They assume the role of planning and scheduling the work, and coordinating the trades in such a manner as to provide for a single source, responsible for a workmanlike and diligent completion of a scope of work.

In the past, insurers were generally left to adjusters and experts to assess damage, determine costs and set the appropriate loss related repair cost for a property. Over the past twenty years, however, several software companies began developing programs, which allowed the user to input a “scope of work” into a computer using a system of codes. The software then applies a unit cost to the scope, and prices the estimate accordingly. Pricing data provided with these programs will often break down the cost of removal of damaged material from the reinstallation. The basic problems with these programs, of course, is that the user may not have the ability or expertise to “look behind” the unit cost to determine if material costs, waste factors, labor rates, productivity rates and markups are correct for the project in question.

While there is an argument that this has resulted in standardization, and many so called “restoration contractors” have endorsed pricing that accompanies the software, the danger is that the insurer has little ability to objectively determine what may be reasonable on a loss-by-loss basis. Therefore, it should be no surprise that computer programs will essentially “default” to standardized settings when adding overhead and profit (when required).

While there is no “custom and practice” in the insurance industry regarding when overhead and profit is applied (and in what percentages), insurers, adjusters and restoration contractors will often add 10% overhead and 10% profit (sometimes on a cumulative basis) on some losses. Sometimes, however, contractors will add many of the costs for general conditions and requirements as line items in their estimates, then add overhead and profit.

Depending on the number and amount of specified general conditions in the estimate, the overhead and profit may not be considered reasonable. Take for example, a fire to a commercial building that destroys about $100,000 in building components. One contractor adds $10,000 in general conditions and another contractor adds no general conditions. Clearly the amount of overhead and profit paid to each contractor should not be the same. For this reason, general conditions, overhead and profit must be objectively determined based on project size and duration, and the state of the market at the date and time of loss. This must be objectively considered on a “loss by loss” basis.

Further, as projects get larger in dollar volume, the amount of overhead and profit should decrease, as is the case in large commercial construction projects. This is essentially because when a larger dollar volume is installed in a project over time, the actual cost of General Conditions/Requirements expenses, expressed as a percentage of the cost to install materials is often less. For this reason, costs for larger projects must be objectively examined to determine the amount of fair and reasonable markup.

Overhead and profit is a “catch-all” phrase used to express markup on construction projects. Proper care should be taken to understand the project size, scope and duration so as determine a reasonable and accurate markup to allow the project to be completed in a proper fashion in a reasonable time frame. In the insurance repair world, overhead and profit should be adjusted when appropriate using the same criteria that is used for new construction.

We would like to thank Jonathon Held, Granger Stuck, and Lisa Enloe for providing insight and expertise that greatly assisted this research.

Jonathon C. Held is the Executive Chairman of the Board of Directors for J.S. Held LLC, a global consulting firm with more than 1,500 professionals on five continents. Mr. Held has had experience in evaluating many of the largest building losses in history, and has completed assignments on projects running into the Billions. He has testified in numerous matters as an expert witness, and has acted as appraiser, umpire, arbitration panelist and sole arbitrator in numerous disputed matters. Mr. Held is a frequent lecturer, and has authored a number of published articles and papers on subjects including valuation, appraisal, and builders risk.

Jonathon can be reached at [email protected] or +1 516 621 2900.

Granger Stuck is an Executive Managing Director in J.S. Held’s Builder’s Risk Practice. Mr. Stuck has worked on construction consulting and expert witness assignments throughout the country, as well as Thailand, New Zealand and Australia. Prior to joining J.S. Held, Mr. Stuck was employed by Mortenson Construction and Clark Construction in varying capacities. He has successfully completed more than $2.0 Billion in projects including one of the world’s largest Stadiums, an indoor arena, convention center, library, highway expansion, and office campus for one of the world’s largest software developers.

Granger can be reached at [email protected] or +1 206 895 9501.

Measuring delay from a loss under a builder’s risk insurance policy is perhaps the most complicated of all time element measures in the claims world. Setting aside the numerous complex issues of coverage, builders risk...

The concept of indemnification for loss is at the core of property insurance reimbursement. Insurance policies are designed to put the policyholder in the same position he or she would have been in had no...

We outline a clear and logical way to proceed with settling disputes through the appraisal provision of the policy of insurance....