Insights

J.S. Held Acquires Shechter & Everett to Expand Forensic Accounting Capabilities for Family Law Disputes in Florida

Read MoreOriginal publication: AICPA & CIMA FVS Eye on Fraud. © 2022 Association of International Certified Professional Accountants. All rights reserved.

As the COVID-19 pandemic lingers on and subjects the globe — and its economy — to its unpredictability, there is renewed focus on how companies are coping with the troubled economy’s effect on operating results. Because an uncertain economy is fertile ground for fraud, regulators, stakeholders, auditors, and forensic accountants are on alert for an increase, in both volume and severity, of financial statement manipulation.

The fraud schemes likely to be perpetrated in this time of heightened risk are much the same schemes that have long been around. They are not new; these types of schemes predate the pandemic and will likely outlive it. What is new, however, is the heightened pressure felt by corporate managers to minimize the damage caused by revenue shortfalls and declines in asset values. Many executives, as they perpetrate misrepresentations and manipulations, may rationalize these frauds as temporary, just a little help until a return to economic stability and market certainty.

Among struggling companies, current economic conditions particularly give rise to fraud schemes like fabricating fictitious or inflated revenue, overstating valuations, making misleading disclosures, and failing to record asset impairments. On the other hand, companies that are performing better than market expectations might be tempted to hold back revenue to create so-called cookie jar reserves for later use.

Among the many possible motivations for financial statement manipulation, the most common include the following:

Financial statements are manipulated for familiar reasons. When such fraud is committed, there are usually three conditions present: (1) incentive (or, put another way, pressure), (2) opportunity, and (3) a willingness to rationalize and excuse the crime.

Historically, financial statement manipulation is more prevalent at the C-suite level. Management is typically involved as either an active perpetrator of the fraud or a complicit party. Executives and upper-level management may also set the tone to mid-level management and those lower on the org chart that things must get done whatever the cost and turn a blind eye when results don’t pass the smell test based on the current economic climate or individual business circumstances. These executives might not always be the perpetrators, but the tone they set — along with unrealistic sales goals and revenue targets — can be enough to induce some employees to compromise their values and break the law, telling themselves that cooking the books is no big deal.

Financial statement manipulation is typically done to make a company’s performance look better than it truly is in an attempt to weather a period of poor performance. However, as mentioned earlier, the inverse also happens, where a company sets out to make its performance look worse. Publicly traded companies, sensitive to both external and internal pressures to meet analyst and market expectations, can be especially susceptible to this temptation. During economic downturns (such as the one brought about by the coronavirus), when the market may anticipate poor performance, companies that do unexpectedly well might be incentivized to hold back sales and revenue to create cookie jar reserves they can dip into when, sometime down the road, they struggle to meet certain earnings targets.

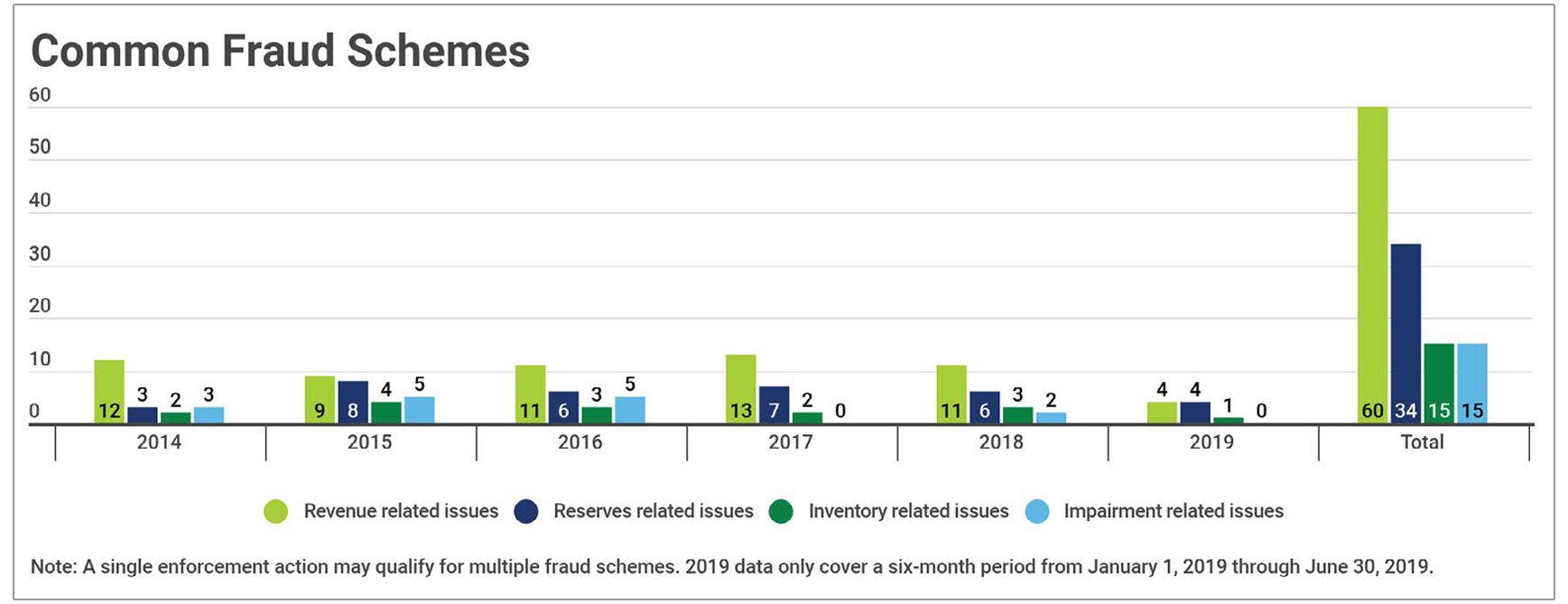

In January 2021 the Anti-Fraud Collaboration (AFC) published the report Mitigating the Risk of Common Fraud Schemes: Insights from SEC Enforcement Actions. This study classifies common financial statement fraud schemes based on analysis of relevant enforcement actions by the SEC from 2014–2019. The industry sector that the SEC charged most often with financial statement fraud was technology services. Other sectors frequently subject to SEC enforcement included finance, energy, manufacturing, and healthcare.

The AFC’s report found that the most common types of fraud were improper revenue recognition, reserves manipulation, inventory misstatement, and impairment issues. Improper revenue recognition took the top spot in every year studied; in 2019 (of which the first six months only were studied) it shared first place with reserves manipulation.

Historically, the application of U.S. generally accepted accounting principles (GAAP) has been based on a rules-based framework providing stringent, industry-specific accounting guidance. However, the new revenue recognition standard, FASB Accounting Standards Codification (ASC) 606, Revenue from Contracts with Customers, utilizes a principles-based framework and replaces earlier GAAP guidance on revenue recognition. Because it provides one comprehensive standard for accounting for customer-contract revenue that is more consistent with international standards, FASB ASC 606 theoretically

simplifies the model for accounting for revenue. However, due to its principles-based focus, there are increased opportunities for different applications and interpretations by management and senior accounting personnel when implementing FASB ASC 606. This increased ambiguity allows for the possibility of manipulations that may not be readily detected by ordinary audit procedures.

Because revenue historically has been the area most frequently subject to manipulation, it is imperative that accountants understand how their clients have adopted FASB ASC 606 and recognize the red flags for financial statement manipulation. With a principles-based framework, it is especially important to evaluate whether accounting for a specified area is applied consistently across financial reporting periods. Relatedly, it is crucial to obtain an understanding of any changes in how the standard is applied during a given period and to evaluate whether such departures are justified.

Revenue recognition is most widely manipulated, but financial statement fraud can involve virtually any account on an entity’s books and records. Some of the most frequently perpetrated fraud schemes are discussed presently. For further information on business fraud risks, the AICPA Forensic and Valuation Services Section has published Fraud Risk Frameworks. This guide is designed to help practitioners identify fraud risks and schemes pertaining to the business, consumer, and government sectors.

The AICPA has also published the Forensic & Valuation Services Practice Aid: Forensic Accounting — Fraud Investigations (available by logging into the FVS Online Professional Library), which provides illustrative information related to financial statement misrepresentation. It’s a valuable source of information for accountants performing financial statement fraud investigations.

Revenue Recognition

Many of the most egregious fraud schemes involve the manipulation of revenue and the timing of its recognition. Such schemes have a direct impact on an entity’s bottom line and, as discussed earlier, usually involve artificial increases or decreases to revenue with the goal of meeting analyst expectations or smoothing earnings.

Common schemes include the following:

In an investigation of revenue recognition fraud, red flags can include unusual jumps in revenue at the beginning or end of a reporting period, significant returns that immediately follow period-end, unusual trends in sales, revenue growth during general economic downturn, altered records, increased revenue without a corresponding increase in cash flow, and top-side or unauthorized journal entries.

Expense Recognition

Expense manipulation is usually an effort to understate expenses to fraudulently improve bottom-line earnings. This might be done in combination with revenue-account manipulation or done discretely to expense accounts. Common schemes include the following:

Red flags for manipulated expense recognition can include changes in capitalization or amortization compared to historic accounting, top-side or unauthorized journal entries, revenue increases without corresponding expense increases, inventory values changing at a different rate than sales, significant changes in ratios with no business justification, and related-party transactions.

Asset Valuation

Asset accounts and the valuation of such are sometimes manipulated. During economic downturns, management might fail to write down or write off impaired assets, resulting in overstated assets on the balance sheet.

Red flags can include a lack of valuations for assets that, given economic conditions, are likely impaired, changes to assets’ useful lives, unusually high accounts receivable, and significant changes in ratios with no business justification.

Liability Reporting

Balance sheets are sometimes manipulated when management fails to appropriately record liabilities or holds significant off-balance-sheet liabilities, all of which presents an entity as being in a healthier financial condition than is true.

Red flags include significant off-balance-sheet transactions, related-party loan agreements, write-offs of related-party loans, and invoices and expenses inconsistent with changes in liabilities.

Misleading Disclosures

Although disclosures have no impact on actual financial statement accounts or bottom-line earnings, they are vital to the financial statements and to understanding the financial health of an entity. Disclosures should include the information necessary to give users of the financial statements a clear picture of an entity’s financial condition. To do this, the financial statements must disclose how events and conditions (such as the pandemic) have affected business operations. Sometimes, management may not manipulate the financial statement accounts themselves but instead present disclosures that are misleading.

Additional red flags to be aware of follow:

While an individual red flag is not dispositive of fraud, its existence could indicate that there are more to be found. At the very least, it should sharpen an accountant’s focus and herald further analysis to determine whether there is any wrongdoing or inaccurate reporting.

The Kraft Heinz Company — Expense-Management Scheme

On September 3, 2021, the SEC charged the Kraft Heinz Company in an expense-management scheme that occurred from 2015–2018. In addition to charging the entity itself, the SEC charged the former chief operating officer and the chief procurement officer for their involvement and misconduct in the scheme. According to the SEC, in its attempt to manipulate expenses, Kraft Heinz recognized unearned discounts from suppliers and maintained false and misleading supplier contracts. This misconduct resulted in improper reductions in the cost of goods sold reported, which in turn resulted in misstated revenue figures. Kraft Heinz was ultimately required to restate several years of its financial statements and corrected over $200 million in improperly recorded cost savings. [1]

HeadSpin Inc. — Revenue Manipulation

On August 25, 2021, the SEC charged Manish Lachwani, the former CEO of HeadSpin Inc., a private technology company, for engaging in a scheme to falsely inflate certain of the entity’s financial metrics and for falsifying its internal sales records from 2018–2020. Mr. Lachwani held significant control of the operations and financials at HeadSpin and was charged with defrauding investors of approximately $80 million by falsely inflating the entity’s valuation to over $1 billion. One way that Mr. Lachwani accomplished this was by recording potential deal amounts that he had just discussed with customers as if they were guaranteed transactions and future payments; he also altered real documents and created fictitious documents to fraudulently increase customer invoices to higher amounts. [2]

Under Armour, Inc. — Revenue Manipulation and Disclosure Failures

On May 3, 2021, the SEC charged Under Armour, Inc., with misleading investors related to its revenue growth and disclosures related to future revenue prospects. The SEC found that starting in late 2015, Under Armour began to “pull forward” existing orders totaling around $408 million that customers had ordered and requested for shipping in future quarters. The entity then misleadingly attributed its revenue growth to various other factors instead of disclosing its pull-forward practices for recording sales and revenue. By manipulating the timing of revenue, Under Armour was able to meet analyst expectations. The company failed to disclose that future revenue was uncertain due to the acceleration of sales and orders placed. [3]

The Cheesecake Factory, Inc. — Misleading Disclosures Regarding COVID-19 Impact

The SEC demonstrated its focus on false disclosures when it settled charges in December 2020 with The Cheesecake Factory, Inc., for making misleading disclosures about the impact of COVID-19 on its business operations and financial condition. This was the first enforcement action by the SEC specifically related to misleading disclosures of the financial impact of the pandemic. The SEC stated that The Cheesecake Factory indicated in filings that its restaurants were “operating sustainably” during the pandemic despite these statements being materially false; in fact, the company was losing significant money (about $6 million in cash per week) and had predicted minimal cash remaining based on its operating results. [4]

We would like to thank Amy Yurish for providing insight and expertise that greatly assisted this research.

Amy Yurish is a Managing Director who joined J.S. Held in March of 2022 as part of J.S. Held's acquisition of Ocean Tomo. She has significant experience leading major forensic services engagements, providing forensic accounting and consulting / expert witness services to both public and private sector clients in disputes involving financial reporting, complex accounting, fraud allegations / bribery and corruption, and economic damages issues. She assists counsel in all aspects of litigation and arbitration proceedings.

A Certified Public Accountant, Certified Fraud Examiner, and Certified in Financial Forensics, Amy has been involved in dispute matters related to principles of asset misappropriation, bribery and corruption including the calculation of disgorgement in foreign corrupt practices act matters, accounting record reconstruction, improper payments, financial reporting, contract disputes, auditor malpractice, and other issues related to the interpretation and application of Generally Accepted Accounting Principles and Statutory Accounting Principles.

Amy can be reached at [email protected] or +1 703 654 1453.

[1] U.S. Securities and Exchange Commission, “SEC Charges the Kraft Heinz Company and Two Former Executives for Engaging in Years-Long Accounting Scheme,” press release no. 2021-174, September 3, 2021, https://www.sec.gov/news/press-release/2021-174.

[2] U.S. Securities and Exchange Commission, “SEC Charges Former CEO of Technology Company With $80 Million Fraud,” press release no. 2021-164, August 25, 2021, https://www.sec.gov/news/press-release/2021-164.

[3] U.S. Securities and Exchange Commission, “SEC Charges Under Armour Inc. With Disclosure Failures,” press release no. 2021-78, May 3, 2021, https://www.sec.gov/news/press-release/2021-78.

[4] U.S. Securities and Exchange Commission, “SEC Charges the Cheesecake Factory for Misleading COVID-19 Disclosures,” press release no. 2020-306, December 4, 2020, https://www.sec.gov/news/press-release/2020-306.

Insurance claims for loss of inventory are generally examined by insurance carriers. The carrier will retain a forensic accountant who has the ability to quantify out of sight inventory losses. Out of sight inventory losses...

Business interruption claims are generally closely scrutinized by insurance carriers and can range from thousands of dollars to claims exceeding $100 million. Insurance carriers often seek the assistance of either internal or external forensic accountants...

A guide to conducting forensic accounting and digital investigations, outlining critical steps, common pitfalls, and real-world case examples....