Insights

J.S. Held Acquires Shechter & Everett to Expand Forensic Accounting Capabilities for Family Law Disputes in Florida

Read MoreInsurance claims for loss of inventory are generally examined by insurance carriers. The carrier will retain a forensic accountant who has the ability to quantify out of sight inventory losses. Out of sight inventory losses occur when the accountant is not able to physically count the damaged inventory. These types of inventory losses include, but are not limited to, damage from fires, floods, and theft. A recent example of a large inventory loss with insurance coverage occurred in March 2022. A cargo ship carrying an estimated $250 million of exotic cars, including Porsche, Audi, Bentley, and Lamborghini models sunk off Portugal’s Azores Islands. Insurance carriers often seek the assistance of forensic accountants to quantify such claims. Initially, the forensic accountant will be retained to quantify the loss of inventory. During their analysis, should a forensic accountant detect the possibility of fraud in a claim, it may prompt further investigation by the carrier.

This paper focuses on the two significant, but different, roles forensic accountants play in quantifying the inventory loss and how – in the normal course of the analysis – they may find instances of fraud that require further investigation. The authors first provide detailed guidance for forensic accountants in how to quantify inventory losses and offer insights into behavior that may indicate fraud stemming from such claims. They also explain the factors considered by carriers when hiring external accountants.

This discussion begins by defining some of the terms and potential players in inventory loss claims that are examined for potential fraud. First, what is an inventory loss? Generally, an inventory loss is the loss of inventory due to situations beyond the control of the company, such as theft or natural disasters (or fire fueled by lithium-ion batteries found in electric vehicles onboard the ship discussed above).

Second, what is forensic accounting and what does a forensic accountant do? The AICPA (the governing body of professional accountancy in the United States) defines forensic accounting as “…the application of specialized knowledge and investigative skills possessed by CPAs to collect, analyze, and evaluate evidential matter, and to interpret and communicate findings in the courtroom, boardroom or other legal or administrative venue.” [1] Therefore, professional accountants, mostly CPAs, conduct forensic accounting engagements. A subcategory of forensic accounting is fraud examination, which may be conducted by either accountants or nonaccountants.

Third, what is fraud? According to Black’s Law Dictionary, fraud is “a knowing misrepresentation of the truth or concealment of a material fact to induce another to act to his or her detriment.” The four major elements of fraud are: (1) false statement of a (2) material fact which is (3) willfully made with an (4) intent to deceive.

While fraud may not be present in every inventory loss claim, it is more often discovered in claims examined by forensic accountants who are both experienced and knowledgeable in fraud detection. The ACFE reported in its 2022 Global Study on Occupational Fraud and Abuse, Report to the Nations, that fraud is a global problem affecting all organizations worldwide. The 2022 study, covering 2,110 cases from 133 countries, found fraud caused total losses exceeding $3.6 billion USD. [2] The same study estimated that organizations lose five percent of their revenue each year to fraud. [3]

An inventory loss may trigger coverage through various policies with the business entity’s insurance carrier. The complexities for inventory loss claims arise when attempting to determine the value of the lost inventory, and whether such inventory is categorized as either raw materials, work-in-process, or finished goods.

Inventory is generally defined as goods held for sale by the business. However, forensic analysts also quantify business personal property losses for goods that are not held for sale. The valuation of such inventory is a reasonably simple process if the business only buys and then resells a product (e.g., a grocery store). It becomes more complex when the business buys raw materials (or parts) and turns those materials into a finished product to sell (e.g., a cellular phone manufacturer). The process of moving from raw materials inventory to finished goods inventory for sale is often referred to as the inventory life cycle. As materials/products move along the inventory life cycle, the inventory becomes more valuable.

Some, but not all, businesses utilize a periodic (as opposed to a perpetual) inventory system to value inventory. A periodic inventory system is a form of inventory valuation where the inventory account is updated at the end of the account period rather than after every sale and purchase transaction (perpetual system). This method allows a business to track its beginning and ending inventory balances within the accounting period and to determine the amount of cost of goods sold using an inventory formula.

Generally, periodic inventory systems utilize an annual (or quarterly) physical count to determine actual inventory. But both periodic and perpetual inventory systems use physical inventory counts to adjust for inventory loss (e.g., theft, obsolete inventory, etc.). Examples of entities employing periodic inventory systems include grocery chains, clothing stores, and manufacturing concerns. Typically, entities with more valuable inventory utilize perpetual systems, including auto dealers, homebuilders, and jewelry stores. Forensic analysts request perpetual inventory records if that is the system used by the business.

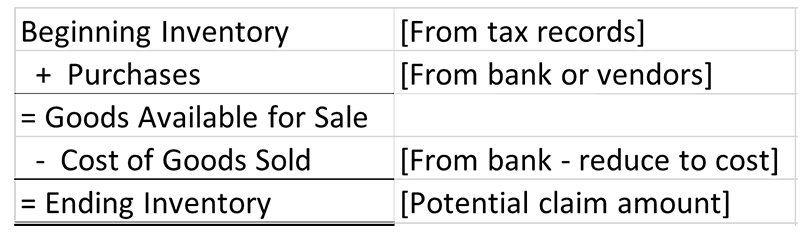

Users of the periodic inventory system utilize the following inventory formula to calculate ending inventory:

The inventory accounts are typically quantified as follows:

Beginning Inventory – The inventory stock at the beginning of the period. Beginning inventory may be verified by either the last physical inventory count or through the entity’s tax return (assuming a calendar-year end).

Purchases – Goods added to the physical inventory during the period. Purchases may be verified through an examination of purchase orders and/or receiving documents.

Cost of Goods Sold – Goods removed from the physical inventory during the period (generally through sales). Cost of goods sold may be verified through an examination of sales receipts, invoices, and shipping documents.

Ending Inventory – The inventory stock at the end of the period. Ending inventory may be calculated with the inventory formula or verified through a physical inventory count.

For manufacturing entities, inventory is further subdivided into the following categories:

Raw Materials Inventory – Goods that ultimately will be part of the manufacturing process but have not entered the production process. For a cellular phone manufacturer, these would be circuits, screens, housing components, etc.

Work-in-Process Inventory – Units in the production process that require additional work before becoming finished goods. For the cellular phone manufacturer, these would be partially assembled phones.

Finished Goods Inventory – Units that have been completed and are available for sale and ready to be shipped.

The first step in preparing an inventory loss claim is gaining an understanding of the loss and policy coverage. The relevant policy defines the actual coverage, loss calculation methods, and limits of coverage for inventory loss claims.

The most typical coverage for loss of inventory is replacement cost or selling price. Replacement cost may be defined as the amount it would cost the company to purchase the lost inventory. While this may be the same as the inventory purchase price, the cost may deviate depending on current market conditions. For instance, the replacement cost may be higher than the original purchase price during inflationary periods. The converse is also true.

Selling price coverage applies to finished goods only. The coverage allows for selling price less unincurred selling expenses. Unincurred selling expenses include discounts, commissions, packaging, and freight, among other costs. If the insured has loss of profits coverage, the computed margin on the lost inventory at the selling price needs to be taken as an offset to the lost profits calculation.

The second step in preparing an inventory loss claim is the compilation of relevant financial records. Such analysis may be performed internally by the business entity or by forensic accountants retained by the carrier (or both if there is a dispute regarding the claim amount). Supporting documentation, by inventory formula type, may include the following:

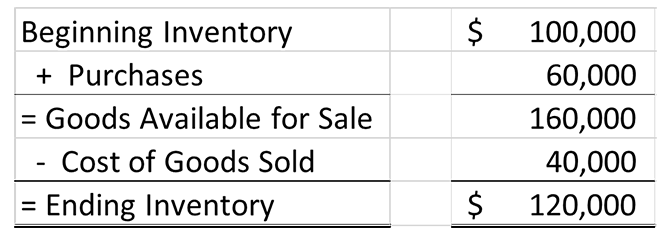

The inventory loss may be calculated as the ending inventory balance (after adjustments) as follows:

The third step in preparing an inventory loss claim is the analysis of the insured’s financial records as discussed above and calculating the loss. In addition to inventory records, an analysis should be performed of ancillary costs that are required to either transport the goods or put those goods in place. Such costs may include transportation, freight, taxes, and stocking fees. Depending on the sophistication of the entity’s accounting system, these costs may or may not be included in the relevant inventory accounts.

After the completion of the above analysis, the final step is to review findings to date for accuracy and completeness and assess the following areas:

RCoins, Inc., a business that specialized in the buying and selling of rare coins, submitted an inventory loss claim to XYZ Insurance Company with the following details:

Upon receipt of the assignment, the forensic accountant will generally research the business, the market, the competitors, market trends, and the general economy of the region where the business is located. Below are examples of documentation and information from the carrier and business that the forensic accountant may request:

The next steps are to evaluate the entity’s beginning inventory, purchases, and cost of goods sold accounts. The forensic accountant may perform such analysis as follows:

Therefore, ending inventory (i.e., value of the potential claim) may be calculated as follows:

As a final check, the forensic accountant should ascertain whether the ending inventory goods were on premises rather than in transit and whether ending inventory is equivalent to replacement cost. On versus off premise information can generally be found through a thorough analysis of the shipping and freight documents. In the RCoins Inc. case study, valuable coins would typically be specifically identified in the relevant documents. The forensic accountant may also consider whether the coins may be repurchased for amounts similar to the purchased amounts. If not, adjustments may be needed to adjust ending inventory to replacement cost (either up or down).

Fraud risk is listed later in the items above for the forensic accountant and the insurance company to consider, but such risks are certainly not the least important. In the RCoins example, there are several areas where a forensic accountant may uncover “red flags” of potential fraud, including:

If fraud is suspected (or detected) the insurance carrier should determine whether an investigation is warranted. Such an investigation is generally outside the scope of the forensic accountant retained for the original inventory loss analysis. The insurance carrier may utilize its own Special Investigation Unit (SIU) team or retain outside forensic accountants to assess the potential fraud issues.

According to the National Insurance Crime Bureau (NICB), other general indicators of insurance fraud in the inventory loss areas include the following [7]:

Inventory loss claims can be both complex to measure and have areas in which fraud exists. Insurance companies often bring in forensic accountants to quantify the out of sight inventory loss. Those who have significant experience recognizing fraudulent schemes may also detect activity that merit further analysis and investigation. When hired to investigate these matters, forensic accountants must know how to identify the various signs and patterns that indicate that a fraud has occurred or is ongoing. In these cases, forensic accountants are called on to gain a unique understanding of how the claimant’s business operates - specifically how income, expenses, profit, and loss on a historical basis is realized. With this information and insight into the financial circumstances of the insured’s financial situation, a forensic accountant can identify instances of fraud within an inventory loss claim.

We would like to thank F. Dean Driskell III and Peter S. Davis for providing insight and expertise that greatly assisted this research.

F. Dean Driskell III is an Executive Vice President in J.S. Held’s Economic Damages & Valuations Practice. He specializes in performing consulting services for clients involved in various types of accounting, economic, and commercial disputes as well as fraud and forensic accounting matters. With more than 30 years of experience in financial analysis, accounting, reporting, and financial management, Dean has served clients and their counsel in both private and public sectors, providing technical analyses, accounting/restatement assistance, valuation services, and litigation support across a variety of industries, and as an expert witness in litigation.

Dean can be reached at [email protected] or+1 470 690 7925.

Peter S. Davis, CPA, ABV, CFF, CIRA, CTP, CFE, is a Senior Managing Director at J.S. Held, specializing in Strategic Advisory. He has served as Receiver in regulatory matters brought by the SEC, FTC, Arizona Corporation Commission, the Arizona State Board of Education, as well as lenders and shareholders. His areas of expertise include understanding and interpreting complex financial data, fraud detection and deterrence, and determination of damages. Peter has provided expert testimony in numerous federal, bankruptcy, and state court matters.

Peter can be reached at [email protected] or +1 602 295 6068.

[1] AICPA Practice Aid 10-1, Serving as an Expert Witness or Consultant.

[2] ACFE 2022 Global Study on Occupational Fraud and Abuse, Report to the Nations, page 4. Report may be downloaded for free at https://www.acfe.com/report-to-the-nations/2022/.

[3] Ibid.

[4] The application of policy provisions is determined by and communicated to the forensic accountant by the insurance carrier.

[5] Personal tax returns are not generally requested for large commercial claims but may be useful in the assessment of potential fraud issues for smaller family-type business claims.

[6] Benford’s Law analysis is an analytical and statistical tool to predict expected digit frequencies in list of numbers. Such analysis may be utilized to predict fraudulent activity in large number sets, such as financial statements, general ledgers, etc. A full analysis of Benford’s Law is outside the scope of this discussion.

[7] NICB “Indicators of Property Fraud”

A guide to conducting forensic accounting and digital investigations, outlining critical steps, common pitfalls, and real-world case examples....

Forensic accountants assist in Marine Insurance cases in a variety of ways, regardless of the cause of loss or type of damages. The purpose of this paper is to discuss a variety of different marine...

Lost profit damages are calculated when a plaintiff’s business alleges that the defendant’s actions impaired its operations in some manner. Determining lost revenues is a critical component in calculating lost profits. Lost profits are based...