Insights

J.S. Held Acquires Shechter & Everett to Expand Forensic Accounting Capabilities for Family Law Disputes in Florida

Read MoreThe COVID-19 pandemic caused unprecedented impacts around the world including stay-at-home orders, curfews, quarantines, and economic uncertainty. Businesses across the United States were forced to close their doors, limit hours of operations, and manage unpredictable financial losses. In an attempt to mitigate the impact of COVID-19, then-President Donald Trump signed the CARES Act into law in March 2020. The CARES Act intended to provide emergency assistance to individuals and businesses affected by the COVID-19 pandemic and included programs designed to quickly provide funds to individuals and businesses. [1]

While COVID-19 itself may no longer be headlining the news cycle, the investigation of potentially fraudulent activity related to COVID-19 funds as described herein continues to be a top priority for government enforcement agencies. With billions of dollars in potential fraudulent disbursements, various government agencies have implemented targeted programs and task forces to identify potential fraud and hold those responsible accountable. As of April 2024, the US Department of Justice had already seized over $1.4 billion in funds that were determined to have been fraudulently obtained.

In this article, we examine the establishment of COVID-19 Loan Programs, indicators of fraud related to the loan programs , the continuing investigation and prosecution of loan fraud cases, recent enforcement actions, recommendations for strengthening internal controls, and how to prepare for a potential audit in relation to a COVID-19 loan probe. This information is intended to help those involved in COVID-19 Loan Program fraud investigations.

As provided for in the CARES Act, the Small Business Administration (“SBA”) quickly implemented the Paycheck Protection Program (“PPP”) in April 2020, which made available fully guaranteed loans to small businesses, individuals, and nonprofit organizations affected by COVID-19. These loans were eligible for forgiveness if at least 60% of funds were spent on payroll costs, with certain limitations, and the remaining spent on eligible expenses such as rent, utilities, and other operating costs. The overarching goal was to help businesses keep their workforce employed during the pandemic and provide quick liquid funds to help mitigate financial losses. [2] PPP loans were offered in two rounds: between April and August of 2020 and between January and May of 2021. [3]

The SBA also offered the COVID-19 specific Economic Injury Disaster Loans (“EIDL”) from March 2020 to December 2021 to provide funding – specifically working capital to meet ordinary and necessary operating expenses – to help small businesses and other entities recover from the economic impacts of the COVID-19 pandemic. [4] The EIDL program was not a new program by the SBA, but instead the program was modified to support businesses impacted financially by COVID-19. Unlike PPP loans, EIDL funds were not eligible for forgiveness. However, these loans were offered with low interest rates and long-loan terms making them economically appealing to businesses. Additionally, the payments were deferred for the first two years, providing businesses with much needed flexibility during the pandemic. [5]

Given COVID-19’s immediate impact on the US and its economy and the view to quickly provide funds to businesses, the SBA recommended financial institutions prioritize speed over due diligence and provided assurance to lenders that they would be held “harmless” if they relied on the information applicants submitted to them. [6] This time-sensitivity in approving COVID-19 relief funds led the US government to waive most of its standard verification protocols required of lenders handling applications. Thus, banks and other financial institutions primarily relied upon self-certifications of applicants to make eligibility and approval decisions.

However, the government still required lenders to establish Bank Secrecy Act (“BSA”) anti-money laundering systems to conduct internal audits and flag suspicious customers. [7] Large, established banks mainly had pre-existing BSA compliance programs in place. Conversely, new entrants trying to handle high volumes of PPP loans in order to cash in on government processing fees had to implement new systems and generally did not have pre-existing BSA compliance programs in place. [8]

With little time to prepare and a powerful incentive to participate, many banks and other financial institutions were perfect targets for fraudsters looking to take advantage of a rushed and fragmented process.

Since the start of the COVID-19 pandemic, the SBA has disbursed about $1.2 trillion of COVID-19 EIDL and PPP funds. Specifically, the SBA has disbursed over $400 billion in COVID-19 EIDL funds and $800 billion in PPP funds. Of the $800 billion in PPP funds disbursed, approximately $763 billion has been forgiven. [9] There was rampant speculation almost immediately after these programs were implemented that there would be significant fraud throughout the programs due to the quick nature of approving loans and heavy reliance on self-certifications. As COVID-19 risks and impacts were mitigated and businesses returned to normal operations, the government began to investigate the usage of COVID-19 loan funds.

On June 27, 2023, the Office of Inspector General (“OIG”) published “COVID-19 Pandemic EIDL and PPP Loan Fraud Landscape” to provide an estimate of the potential fraud in the SBA’s pandemic assistance loan programs. [10] The OIG estimated that more than $200 billion ($136 billion in COVID-19 EIDL loans and $64 billion in PPP loans) of the $1.2 trillion in COVID-19 loan funds was disbursed in potentially fraudulent loans, representing about 17% of all funds. [11] The OIG concluded that due to the rush to swiftly disburse funds, the SBA weakened or removed the controls necessary to prevent fraudsters from easily gaining access to the SBA’s pandemic assistance loan programs and provide assurance that only eligible entities received funds. [12] This occurred even though early OIG reports warned of the importance of a strong internal control environment to mitigate fraud risk.

In order to strengthen internal controls, the OIG offered the following recommendations over the course of the SBA’s pandemic assistance loan programs:

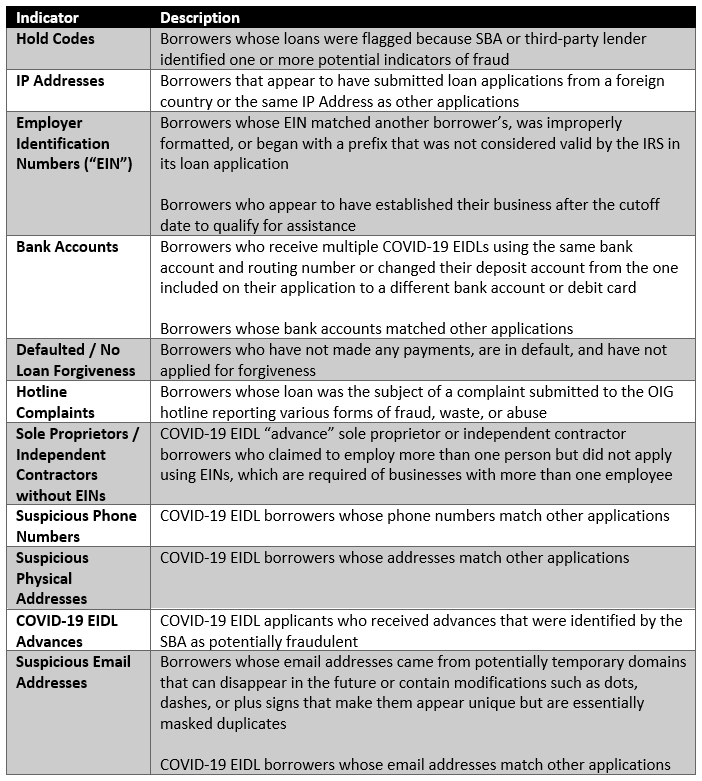

The OIG identified the following fraud indicators related to COVID-19 loans: [14]

Accordingly, the SBA implemented corrective actions, such as requiring tax transcripts for COVID-19 EIDL borrowers, flagging certain EIN prefixes, and requiring loan officer reviews for changed bank accounts prior to disbursements, among other actions. [15]

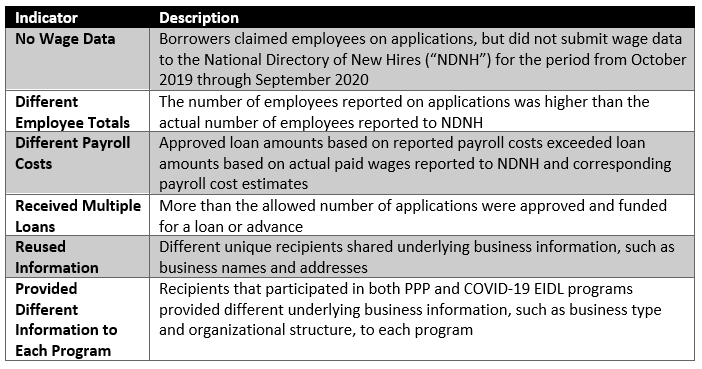

The GAO also reviewed the SBA’s disbursement of COVID-19 loan funds and recommended that the SBA ensure it has and utilizes mechanisms to facilitate cross-program data analytics and identify external data sources that could aid in fraud prevention and detection, and to develop a plan to obtain access to those sources. [16] The GAO identified the following additional fraud indicators for COVID-19 loans which could be identified through data analytics of loan documents: [17]

Initially, most COVID-19 loans were subject to a five-year statute of limitations for any applicable enforcement efforts, meaning that criminal or civil enforcement actions were required to be filed no later than five years after the offense was committed. Recognizing the potential magnitude of fraud in the COVID-19 loan programs, two bills were enacted and signed into law by President Joseph Biden in August 2022 to extend the statute of limitations to 10 years. [18]

The longer statute of limitations, which is consistent with the statute of limitations associated with bank fraud cases, gives the Department of Justice (“DOJ”) and other agencies more time to investigate large and complex COVID-19 loan fraud cases. [19] Additionally, the expanded statute of limitations provides the government additional time to consider investigations into lenders and other insiders in cases where key individuals may have facilitated fraudulent loans. [20]

According to the Internal Revenue Service’s Criminal Investigation Chief Guy Ficco: “In the last year alone, we have opened nearly 700 new COVID fraud investigations that collectively add up to $5 billion in potential fraud.” He also stated that while COVID-19 may no longer be top of mind to Americans, “the fraud committed through these different programs is very much top of mind…” [21]

As of April 9, 2024, OIG oversight of PPP and EIDL loan programs resulted in 1,255 indictments, 985 arrests, and 683 convictions. Over $8 billion in EIDL funds has been returned to the SBA by financial institutions and another $20 billion by borrowers. [22]

Also as of April 9, 2024, the DOJ’s nationwide effort to combat COVID-19 loan fraud has resulted in more than 3,500 defendants being criminally charged, and more than 400 settlements or court judgements totaling more than $100 million for civil charges. Additionally, DOJ prosecutors have seized over $1.4 billion in funding determined to be fraudulently obtained. [23]

The False Claims Act, which is a civil statute that is leveraged against companies for defrauding government agencies, is being used by the DOJ to try to recoup taxpayer dollars from CARES Act lenders. In 2023 alone, the DOJ resolved approximately 270 False Claims Act matters and recovered over $48.3 million specifically in connection with PPP fraud. [24]

The DOJ also uses the Bank Secrecy Act, which requires financial institutions to establish and maintain programs to detect and prevent money laundering, identify potential deficiencies in customer due diligence for loan applicants, and report fraud or other suspicious activity.

Federal prosecutors have been targeting businesses and individuals who may have violated the COVID-19 loan programs by:

These violators fall largely into two categories: individuals or small groups and coordinated criminal rings. [26] The most common criminal charges related to COVID-19 loan fraud are:

Initially, in May 2021, the DOJ created a specialized COVID-19 Fraud Enforcement Task Force to partner with other government agencies to identify and investigate potential instances of pandemic related fraud. In September 2022, the DOJ announced the creation of specialized “Strike Force teams”, with locations in Los Angeles, Sacramento, Miami, and Baltimore, to enhance efforts to combat and prevent COVID-19 related fraud. [28] In August 2023, the DOJ launched another two Fraud Strike Forces in Colorado and New Jersey. [29]

Much of the initial investigations and enforcement actions focused on so-called “low hanging fruit,” such as instances where applicants allegedly used funds for exorbitant personal purchases (vacation homes, expensive cars, etc.), created fictitious companies, and applied for loans for companies that did not exist prior to March 2020.

More recently, the task force has shifted its focus to more complex potential fraud schemes as well as the review of certain banks and financial technology companies (“fintechs”) that may have approved allegedly false COVID-19 loans to identify evidence that banks either ignored red flags, bypassed fraud-detection measures, or colluded with customers. [30] In Principal Deputy Assistant Attorney General Brian M. Boynton’s 2024 Federal Bar Association’s Qui Tam Conference Remarks on February 22, 2024, he identified that in April 2023, the DOJ filed claims against Kabbage, Inc., a fintech that processed PPP loan applications for lenders and underwrote PPP loans, alleging that the company miscalculated tens of thousands of PPP loans and knowingly failed to implement appropriate fraud controls. [31] In May 2024, Kabbage, Inc. agreed to resolve these allegations with the DOJ stating that it would receive a claim of up to $120 million in Kabbage, Inc.’s bankruptcy proceedings. [32]

In an example of enforcement related to banks, the DOJ settled with a regional bank in Texas and Oklahoma for allegedly processing an ineligible customer’s loan under the False Claims Act. [33]

Other recent enforcement actions demonstrate the focus on more complex fraud schemes and where multiple individuals were involved in the alleged fraud. Some examples of these include:

As the DOJ and other agencies continue to investigate and prosecute alleged fraud stemming from the COVID-19 loan programs, they will likely continue to become more sophisticated in their investigations and rely on data analytics and other potential fraud indicators to identify wrongdoing. While banks and fintechs relied heavily on self-certifications when approving loan applications, if there were blatant red flags or fraud indicators missed, these entities may also be subject to investigations and penalties. For banks and fintechs subject to these investigations, it is important to verify the effectiveness of identity verification programs and fraud prevention controls to support compliance with SBA requirements.

For businesses that received COVID-19 loan funds, it continues to be important to maintain and retain supporting documentation related to the initial loan application, usage of funds, and, specifically in the case of PPP, loan forgiveness. The loan agreements for both PPP and EIDL included certain loan covenants related to the segregation of loan funds, requirements related to the usage of the funds, and documentation to be maintained. They also provided certain stipulations on the business, for example, related to owner draws and usage of the assets of the businesses.

To prepare for a potential audit related to PPP or EIDL loans, it’s important for businesses to compile and maintain documentation related to loan application and the use of the loan itself. Examples of documentation that borrowers should generally retain include:

Since the statute of limitations was extended, businesses should retain documentation for a long enough period to cover potential government audits or investigations that may arise. Businesses should consider also including communications related to the COVID-19 loans that may support other official business documentation.

Like other types of inquiries or potential investigations from government enforcement agencies, businesses and individuals should consider hiring counsel to guide them through the nuances of a government investigation. While the DOJ has been vocal regarding the advantages of self-reporting potential fraud or improprieties and cooperating with their investigations, individual businesses need to evaluate the risks and rewards of doing so depending on their individual circumstances.

Forensic accountants play a critical role in supporting businesses, individuals, and lenders, along with their counsel, when faced with a government audit, investigation, or potential enforcement action. They have the expertise and training to perform complex financial analysis, large scale document review and data analysis, and fund tracing between multiple accounts and entities. Forensic accountants are also typically experienced in providing expert testimony and delivering presentations to enforcement agencies. For lenders in particular, forensic accountants are uniquely positioned to provide support due to the intersection between anti-money laundering systems and compliance with the nuanced requirements related to approval and distribution of Covid-19 loan funds.

We would like to thank our colleagues, Amy Yurish and Nicole McTernan, for providing insights and expertise that greatly assisted this research.

Amy Yurish, CPA, CFE, CFF, is a Managing Director who joined J.S. Held’s Global Investigations practice in March of 2022 as part of J.S. Held's acquisition of Ocean Tomo. She has significant experience leading major forensic services engagements, providing forensic accounting and dispute consulting services to both public and private sector clients in the areas of corporate investigations, financial statement analysis, auditor malpractice, technical accounting matters, purchase price disputes, and the calculation of economic damages. She assists counsel in all aspects of litigation and arbitration proceedings.

A Certified Public Accountant, Certified Fraud Examiner, and Certified in Financial Forensics, Amy has led forensic accounting matters and internal / external investigations including allegations of bribery and corruption including the calculation of disgorgement in Foreign Corrupt Practices Act matters, employee and executive fraud, asset misappropriation, accounting record reconstruction, improper payments, COVID-19 loan investigations, and other issues related to the interpretation and application of Generally Accepted Accounting Principles and Statutory Accounting Principles (GAAP).

Amy can be reached at [email protected] or +1 703 654 1453.

[1] https://www.sba.gov/sites/default/files/2023-06/SBA%20OIG%20Report%2023-09.pdf

[2] https://www.sba.gov/sites/default/files/2023-06/SBA%20OIG%20Report%2023-09.pdf

[3] https://www.gao.gov/assets/gao-23-105331.pdf

[4] https://www.sba.gov/sites/default/files/2023-06/SBA%20OIG%20Report%2023-09.pdf

[10] https://www.sba.gov/sites/default/files/2023-06/SBA%20OIG%20Report%2023-09.pdf

[11] https://www.sba.gov/sites/default/files/2023-06/SBA%20OIG%20Report%2023-09.pdf

[12] https://www.sba.gov/sites/default/files/2023-06/SBA%20OIG%20Report%2023-09.pdf

[13] https://www.sba.gov/sites/default/files/2023-06/SBA%20OIG%20Report%2023-09.pdf

[14] https://www.sba.gov/sites/default/files/2023-06/SBA%20OIG%20Report%2023-09.pdf

[15] https://www.sba.gov/sites/default/files/2023-06/SBA%20OIG%20Report%2023-09.pdf

[16] https://www.gao.gov/assets/gao-23-105331.pdf

[17] https://www.gao.gov/assets/gao-23-105331.pdf

[22] https://www.justice.gov/coronavirus/media/1347161/dl?inline

[23] https://www.justice.gov/coronavirus/media/1347161/dl?inline

[25] https://www.pagepate.com/experience/criminal-defense/federal-crimes/ppp-loan-fraud-charges/

[26] https://www.pandemicoversight.gov/news/articles/charged-ppp-scammers

[27] https://www.pagepate.com/experience/criminal-defense/federal-crimes/ppp-loan-fraud-charges/

[28] https://www.justice.gov/opa/pr/justice-department-announces-covid-19-fraud-strike-force-teams

[32] https://www.marketwatch.com/amp/story/kabbage-resolves-ppp-fraud-claims-for-120-million-17258f85

[34] https://www.justice.gov/opa/pr/nevada-man-convicted-112m-covid-19-fraud

[39] https://www.justice.gov/opa/pr/three-individuals-sentenced-35m-covid-19-relief-fraud-scheme

[40] https://www.justice.gov/opa/pr/covid-19-relief-fraudster-convicted-bank-fraud

[41] https://www.justice.gov/opa/pr/six-men-sentenced-roles-20m-covid-19-relief-fraud-ring

As the COVID-19 pandemic lingers on and subjects the globe — and its economy — to its unpredictability, there is renewed focus on how companies are coping with the troubled economy’s effect on operating results...

The purpose of this paper is to discuss some of the major work and financial matters forensic accountants focus on, including fraud investigations and insurance claims, and how they bring unique value to the process....

A guide to conducting forensic accounting and digital investigations, outlining critical steps, common pitfalls, and real-world case examples....