Insights

J.S. Held Acquires Shechter & Everett to Expand Forensic Accounting Capabilities for Family Law Disputes in Florida

Read MoreAsset managers need companies to provide climate risk disclosure that is clear, precise, and tailored to specific sustainability guidelines. While there are numerous third-party frameworks that asset managers are using, the Task Force on Climate-Related Financial Disclosures (TCFD) provides the most widely endorsed climate change reporting framework. Company disclosure in line with the TCFD framework is becoming a requirement by shareholders. Sustainability managers can begin preparing today by understanding the disclosure requirements and building their climate data management systems.

In 2016, the G20 Finance Ministers and Central Bank Governors became concerned that climate change was a risk that could potentially lead to financial instability. They were also concerned there was inadequate and inconsistent disclosure standards. Given these concerns, the Financial Stability Board’s (FSB) chair, Mark Carney, was tasked with reviewing how the financial sector can better account for climate-related issues. The Task Force, chaired by Michael Bloomberg, was asked to develop voluntary, consistent climate-related financial disclosures that would be useful to investors, lenders, and insurance underwriters in understanding material climate-related risks. Following a public comment period in 2017, the TCFD released its final recommendations report and supplemental materials including:

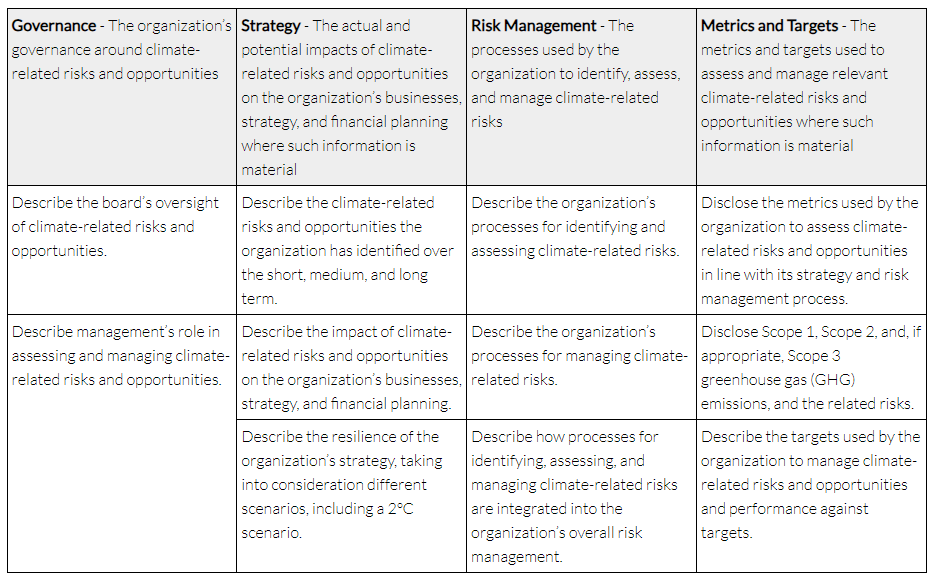

The Task Force structures its recommendations around four key areas (see Table 1).

Companies are unlikely to face divestment or dissenting shareholders immediately, but TCFD disclosure for all intents and purposes is no-longer optional. There will be time for companies to fall in line with reporting expectations, and this is more likely to be driven by regulators than investors.

Companies should start now before full compliance with sustainability disclosure standards is required. This is an iterative process. Starting now with an imperfect disclosure is better than waiting until the internal practices and procedures are in place.

Sustainability managers should consider taking the following steps:

We would like to thank our colleagues Andrea Korney and Steven Andersen for providing insights and expertise that greatly assisted this research.

Andrea Korney is Vice President of Sustainability for J.S. Held’s ESG & EHS Digital Solutions group. Throughout her career, Andrea has demonstrated her passion for inclusive stakeholder relations in the mining and energy sectors, focusing on reducing barriers and creating opportunities for diverse employees, business owners, and industry partners through policy and regulation influence, workforce development, and sustainability outreach. Andrea’s 25+ years of experience in energy and metals extraction includes longstanding roles in oil & gas, power generation, and mining across North America and Russia. Her focus in these roles has included HR, corporate services, global supply chain and logistics, stakeholder relations, Native American relations, and government affairs.

Andrea can be reached at [email protected] or +1 725 567 0668.

Stay up to date on the latest trends & developments in the carbon offset markets & gain a better understanding of the supply & demand for the different offsets available....

The new clean fuel regulations in Canada aim to lessen carbon intensity of transportation fuel by 2030. This paper discusses how primary fuel suppliers can prepare and comply with the forthcoming regulations. The following information...

We discuss the options proposed by ECCC, the scope of the proposed emissions cap, and what to expect from upcoming ECCC communications regarding the emissions cap decision....