Insights

J.S. Held Acquires Shechter & Everett to Expand Forensic Accounting Capabilities for Family Law Disputes in Florida

Read MoreThe Canadian federal government has developed the Clean Fuel Regulations (CFR) to increase incentives for the development and adoption of clean fuels, technologies, and processes with the goal of making transportation fuel (gasoline and diesel) less carbon intensive. By 2030, the carbon intensity of these fuels is set to decrease by approximately 15% below 2016 levels and, overall, will deliver up to 26 MT of GHG (greenhouse gas) reductions.

The CFR will replace the current Renewable Fuel Regulations (RFR). The key difference between the CFR and RFR is a focus on lifecycle GHG emissions rather than volumetric blending requirements for renewable fuels. Low carbon fuel programs already exist in California, Oregon, Washington, and the province of British Columbia. However, the CFR is the first national low carbon fuel program in North America.

To support the ramp-up of the CFR, the government of Canada is providing $1.5 billion toward a Clean Fuels Fund (the Fund). The Fund will support domestic production and adoption of low-carbon fuels such as biofuels. The federal government is also supporting clean hydrogen production through the Fund by investing in early-stage opportunities highlighted in the national hydrogen strategy.

The CFR will take a lifecycle approach to regulating GHG emissions. This involves tracking and reducing emissions at all stages of the fuel lifecycle, including extraction, processing, distribution, and use. The regulated entity will be the primary fossil fuel suppliers. This includes producers and importers. Primary suppliers will be required to reduce the carbon intensity of fuel by 3.5 gCO2e/MJ in 2023. Carbon intensity reduction requirements will increase by 1.4gCO2e/MJ per year to ultimately reach 14 gCO2e/MJ in 2030.

To provide primary suppliers with compliance flexibility, the CFR establishes a credit market. In this market, credits are awarded to companies that produce or use clean fuels, such as biodiesel or renewable natural gas. These credits can then be bought by companies to help them meet their regulatory obligations related to reducing carbon emissions. A credit market also helps to drive carbon intensity reductions at the lowest possible cost. To comply, primary suppliers must create or purchase credits. If parties have extra credits, they can bank them for future compliance or sell them to the market.

The CFR is expected to create a market signal for investment in low carbon intensity fuels and technologies such as producers of biofuels. Biofuel feedstock providers such as farmers and foresters will also see opportunities as demand for low-carbon fuels increases. However, it should be noted that not all biofuel feedstock and production processes are created equal. The feedstocks and processes that have the lowest carbon intensity will create more CFR credits and will, therefore, be more valuable to primary suppliers.

The CFR will also extend a market signal beyond just the liquid fuel supply chain. The regulation will promote advanced vehicle technologies like electric vehicles. Credits can be generated by changing network operators and charging site hosts. All revenue associated with residential and public electric vehicle charging must be reinvested back into charging infrastructure, electrical distribution infrastructure, or financial incentives for consumers.

The regulations establish a credit market to allow fuel suppliers the flexibility to meet carbon intensity reduction requirements in a cost-effective way. Each credit represents an emission reduction of one tonne of GHG or tCO2e.

Credits can be generated in three ways:

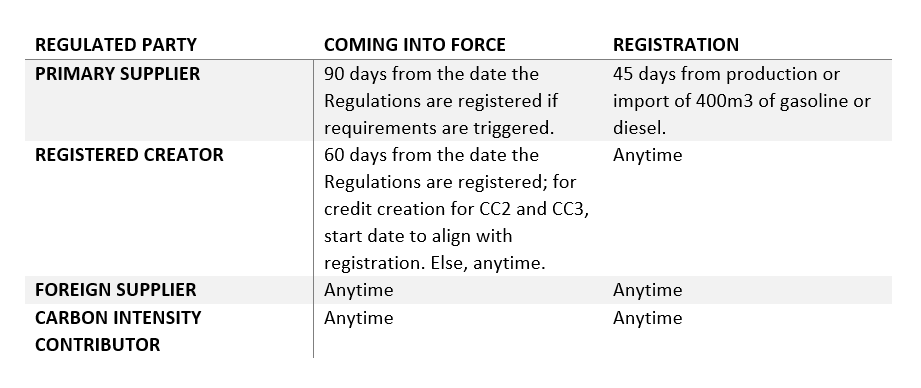

Beginning July 6, 2022, following the release of the final CFR, certain elements of the regulation came into force. This includes:

Beyond certain elements of the regulation that are currently in force, regulated entities should seek to familiarize themselves with the Fuel LCA (lifecycle assessment) Model including the Specifications for Fuel LCA Model CI Calculations (which provides instructions for calculating carbon intensity values of fuels, energy sources, and material inputs for the purpose of creating credits) and CFR Data Workbook (a spreadsheet that helps convert applicant data to ensure compatibility with the Fuel LCA Model). The model allows users to calculate carbon intensity (CI) for the purposes of creating credits under the CFR. The model will be used by registered creators, foreign suppliers, and carbon-intensity contributors. There are three main components of the model:

In addition to the model, CC1 credits that are generated under the CFR must adhere to prescribed quantification methods which include:

Experts can help assess a company’s greenhouse risk exposure to understand the importance of the issue to its operations. Additionally, for businesses that supply, import, or produce fuel in Canada, here are some steps to take to prepare for the CFR:

The Canadian federal government has developed the CFR to reduce the carbon intensity of transportation fuel by 2030. These regulations will replace the current Renewable Fuel Regulations and focus on lifecycle GHG emissions rather than volumetric blending requirements for renewable fuels. To comply with these regulations, primary suppliers must create or purchase credits; a credit market has been established to allow fuel suppliers the flexibility to meet carbon intensity reduction requirements cost-effectively. The Clean Fuels Fund has been created to support domestic production and adoption of low-carbon fuels, and this regulation will extend a market signal beyond just the liquid fuel supply chain to promote advanced vehicle technologies like electric vehicles. The CFR will create opportunities for biofuel feedstock providers. Those with the lowest carbon intensity will create more credits and will, therefore, be more valuable to primary suppliers. Overall, these regulations are expected to create a market signal for investment in low carbon intensity fuels and technologies and will deliver up to 26 MT of GHG reductions.

It is important to have experts assess a company’s greenhouse risk exposure to understand the importance of the issue to its operations. Such experts can help set greenhouse gas targets throughout a business’s operations, identify reduction and efficiency opportunities, develop economics and tracking of abatements, and deploy field sensors and automated technology to validate that actual performance meets expectations.

We would like to thank our colleagues Chris Davin and Steven Andersen for providing insights and expertise that greatly assisted this research.

Chris Davin is a Senior Vice President and ESG & Digital Solutions Service Line Lead within J.S. Held’s Environmental, Health & Safety (EHS) practice. Chris has spent over 10 years in the EHS industry, with specific experience in EHS management systems, information management systems, and process optimization. He also has an extensive background in Information Technology (IT) consulting, IT architecture, and software development. Chris brings together his background in EHS information systems with organizational strategy and leadership capabilities to offer consultancy that is holistic and oriented for the long term. Chris advises his clients on various EHS and ESG issues, including needs and gap assessments, software selection and implementation, data management and visualization, and enterprise integration.

Chris can be reached at [email protected] or +1 368 209 1004.

We discuss the options proposed by ECCC, the scope of the proposed emissions cap, and what to expect from upcoming ECCC communications regarding the emissions cap decision....

In September 2022, the U.S. Environmental Protection Agency (EPA) Region 1 issued a decision to use its Clean Water Act (CWA) Residual Designation Authority (RDA) to require National Pollution Discharge Elimination System (NPDES) permits for...

The Environmental Protection Agency (EPA) Office of Land and Emergency Management (OLEM) oversees policy and guidance for the EPA’s hazard response and waste programs. [1] In October 2022, OLEM released its Environmental Justice (EJ) Action...