Insights

J.S. Held Acquires Shechter & Everett to Expand Forensic Accounting Capabilities for Family Law Disputes in Florida

Read MoreCarbon offsets are used by sustainability managers to make progress toward a company's greenhouse gas (GHG) emissions reduction targets. Carbon offsetting allows companies to reduce their carbon footprint by supporting projects that reduce or remove GHGs from the atmosphere. These projects can include activities such as renewable energy generation, reforestation, and conservation of natural resources. By purchasing carbon offsets, companies can mitigate their own emissions and contribute to the reduction of global GHG emissions. Additionally, carbon offsetting can also provide companies with a way to demonstrate their commitment to sustainability to consumers, shareholders, and other stakeholders.

In 2022, corporations purchased and retired a total of 155 million carbon offsets. This is a decrease from 2021. The decrease in market volume can be attributed to growing criticism of carbon offsets by investors and the media. Despite this, the overall supply of offsets still rose slightly by 2%, with projects in 77 different countries issuing a total of 255 million carbon offsets. The supply of offsets related to avoided deforestation dropped significantly by 32%, such as major projects in Peru, Indonesia, and Kenya, which did not issue offsets in 2022.

On the other hand, reforestation and agriculture supply both saw increases, but these increases were not enough to offset the drops seen in other areas. Uneven project activity across different GHG reduction types suggests that the overall market for carbon offsets is facing challenges and uncertainty.

Despite this uncertainty, a new Bloomberg report on the long-term outlook for the voluntary carbon market (VCM) is projecting that market value could surge in the coming years. Under a bullish scenario, the total market value could approach $1 trillion as early as 2037. As companies strive to achieve net zero emissions, demand for offsets is expected to increase dramatically. The potential for growth in supply is also significant, with the potential for an increase of up to 60 times depending on the scaling of carbon removal and nature-based solutions.

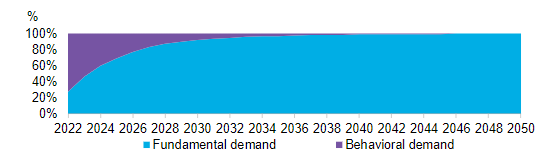

Demand for carbon offsets will rise in the coming years as companies work toward their net zero goals. The demand can be classified as either behavioral or fundamental. Behavioral offset demand occurs when companies buy carbon offsets to differentiate themselves from their competitors or to claim carbon neutrality. This type of demand is common in consumer-facing sectors like airlines and retail companies that provide customers with the option to offset their purchases for an additional fee. It is also common in companies that offer green alternatives to their products. For example, bundling offsets with fuel can create products like “green gas” or “carbon-neutral LNG.” Behavioral offset demand is expected to decrease over time as companies shift toward long-term net zero goals (see Figure 1).

Unlike behavioral demand, fundamental demand is a method used to determine a company's residual emissions on the path to achieving net zero emissions. Companies that set net zero targets will typically seek to reduce their emissions as much as possible through activities such as clean energy procurement, electric vehicles, and business model changes. The company’s remaining emissions would then need to be offset by purchasing offsets to reach net zero emissions. The number of offsets needed will vary based on the company, its net zero targets, and its gross emission reduction progress.

It is expected that the demand for emissions reductions through behavior changes will decrease from 181 million tonnes of CO2 equivalent in 2023 to zero in 2050 as companies shift toward achieving net zero goals. This is expected to be replaced by an increasing demand for emissions reductions through fundamental changes, reaching a forecasted 1.1 billion tonnes of CO2 equivalent in 2030 and 5.4 billion tonnes of CO2 equivalent in 2050. Fundamental demand is less affected by price changes and will become dominant over the long term.

On the supply side, it is predicted that the supply of emissions reductions will greatly increase, surpassing 8 billion tonnes of CO2 equivalent by 2050, primarily through nature-based solutions such as avoided deforestation, reforestation, and sustainable agriculture. Focusing on removal efforts will lead to increased investment in technologies like direct air capture (DAC) and bioenergy carbon capture and storage, bringing the expected supply to 9.8 billion tonnes of CO2 equivalent by 2050.

In 2022, there were several announcements that could support growth and trust in the offset market, such as government interest in regulating offset markets, company-led buying initiatives, and the development of rating agencies. The US Commodity Futures Trading Commission (CFTC) expressed interest in regulating the voluntary carbon offset market, but the impact of such intervention is uncertain due to the global nature of the market. The Lowering Emissions by Accelerating Forest finance (LEAF) coalition, which includes companies like Amazon, Nestle, Salesforce, Unilever, and GSK, set out to direct $1 billion of investment into protecting tropical forests and has since surpassed that goal by 50%. The Integrity Council for the Voluntary Carbon Market (ICVCM) released its draft of the Core Carbon Principles, which outlines the criteria offsets to meet to be considered high quality, but it has been met with some criticism. Rating agencies, like BeZero and Sylvera, are increasingly being used to score projects on their quality, providing useful information to buyers and brokers when trading offsets.

Compliance markets, where entities are required to reduce their emissions to specific levels and purchase allowances for anything over these levels, have historically been distinct from the voluntary carbon markets. However, the distinction between the two is becoming less clear in 2022 as more compliance markets are starting to accept voluntary carbon market offsets. Some North American markets such as California and Canada allow companies to meet a portion of their mandates with domestically produced offsets. The UK is also considering a similar structure for carbon removal, which would be a departure from the EU, where offsets have been banned since 2012. Some markets in the Asia Pacific region, including Australia, South Korea, and China, permit offsets in their compliance markets. The growing overlap between compliance and voluntary markets could lead to competition for the same pool of supply.

The Bloomberg report forecasts carbon offset prices under three scenarios, Voluntary Market, Bifurcation and Removal, each of which are discussed below.

Voluntary Market Scenario

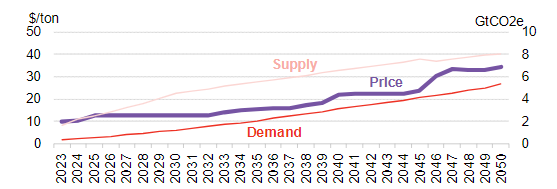

In the voluntary market scenario, it is assumed that there will be no significant changes in the offset market, and companies will continue to purchase all types of offsets. Prices in this scenario would be low, with supply being almost four times greater than demand in 2030. Offsets would cost only $13 per tonne in 2030, valuing the market at a mere $15 billion, and increasing to $35 per tonne in 2050 (see Figure 2). This scenario would also drive a lot of supply and liquidity, which is beneficial for traders, exchanges, and financials.

However, with so much supply, the market would represent low-quality projects that lack additionality. As a result, the VCM could fail to achieve the most crucial goal of the market: drive emission reductions. This scenario would also negatively impact sectors that require significant investments, such as technology-based removal and high-quality nature-based solutions, which have the potential to make the biggest decarbonization impact in the long term but will remain expensive without financing and deployment at scale. Emerging technology such as DAC would fail to receive the necessary investment. Nascent sectors, such as blue carbon, would also be impacted negatively. However, events that reduce supply or increase demand, such as the Russia-Ukraine war and the emergence of compliance markets, could end up having the unintended consequence of being beneficial to the offset market by increasing offset prices.

Bifurcation Scenario

The bifurcation scenario predicts that the offset market will split into two, with a smaller market for high-quality, expensive credits and a larger market for everything else. Even if the market remains unchanged, as described in the voluntary market scenario, some companies will still opt for higher quality offsets. These higher quality offsets will be marked by more robust additionality claims. The likelihood of this happening increases in the voluntary market scenario, as companies will need to work harder to differentiate their offset portfolio for investors.

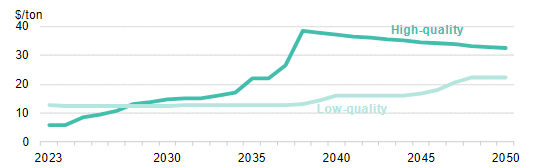

Under this scenario, some companies will demonstrate a willingness to pay a premium to avoid negative press around their offset purchases to avoid negative reputational risk. Determining what is considered high-quality and low-quality in the offset market will be crucial for price discovery. According to the report, a market that is divided by the definition of quality would reach its highest price of $38 per tonne in 2038. However, this price would be insufficient to persuade investment in technology-based removal methods such as DAC. A market that is of low quality would see prices reach a peak of $22 per tonne in 2050 (see Figure 3).

The difference between these markets would depend on how inclusive the definition of “high-quality” is. The work of groups like ICVCM is essential as it would create a clear distinction between good and bad offsets. The likely outcome from the bifurcation scenario is a separation in the market, where a smaller, less liquid market for high-quality carbon offsets would exist, and the remaining low-quality supply would exist in a more dynamic, low-price market. This is like other commodity markets, such as in oil markets, where light crude, which yields more gasoline or jet fuel, trades at a premium to heavier crude which yields more bunker fuel. The report suggests that this type of product differentiation in the VCM would represent a natural evolution of the offset market.

Prices in a bifurcated market would be too low to drive any meaningful climate benefits. In fact, 2050 pricing is even lower than in the voluntary market scenario. Over-supply would also be an issue. In a low-quality market, demand is high enough to only consume two-thirds of the available supply. If definitions around good quality are more inclusive, supply could be even greater. A high-quality market could work if there's enough demand to sustain it. Such a market would depend on investor pressure to purchase high-quality offsets, as companies might opt for cheaper, low-quality offsets if prices go up. Verra, the largest offset registry, fears that almost none of the current supply in the offset market would meet the core carbon principles laid out by ICVCM, which could be a near-term risk to this bifurcated market. Therefore, the bifurcation scenario highlights the importance of defining quality to keep the market balanced.

Removal Scenario

The removal scenario assumes that companies can only buy offsets that focus on removing carbon to achieve net zero goals. Only credits that store or sequester carbon at levels that wouldn’t otherwise occur would be permitted. This would include offsets from nature-based solutions such as reforestation and agriculture, as well as technology-focused removal methods such as DAC and bioenergy carbon capture and storage. Offsets that are classified as avoidance, which prevent emissions that would have otherwise occurred, would be excluded. This scenario, if realized, would lead to a temporarily undersupplied market.

The elimination of avoidance-based credits in the market would nullify supply from activities such as avoided deforestation (REDD+) as well as clean energy and clean cookstoves. This crackdown on avoidance offsets is being led by third-party initiatives, investors, media, and those who believe that avoidance offsets serve as a cover for heavy-emitting industries. The Science Based Targets Initiative (SBTI) is perhaps the biggest indirect proponent of a removals-only carbon offset market. The SBTI only allows a company to claim alignment with their definition of net zero if the company neutralizes residual emissions with removal offsets. Avoidance credits, which prevent emissions that would have otherwise occurred, are not permitted for use against a company’s direct emissions. However, it's worth mentioning that SBTI still allows for the use of avoidance offsets for interim use or for use outside of a company's value chain.

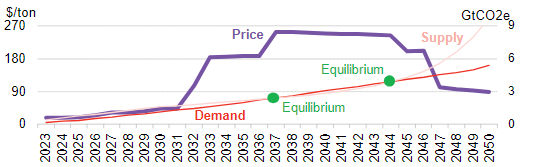

A removal scenario would send offset prices to new highs. However, the price increases gradually to give buyers time to prepare. Under this scenario, the cost of carbon offset credits would increase significantly, with prices reaching $42 per tonne in 2030, $254 per tonne in 2037, and eventually dropping to $88 per tonne in 2050. The market is estimated to be valued at $953 billion annually when prices peak in 2037 and $476 billion in 2050 (see Figure 4).

Under a removal scenario, the marginal price is set by DAC technology. Although the technology only makes up a small percentage of total removal offset supply in 2033, at less than 1%, it gradually increases over time. By 2040, DAC will make up 8% of the offset market and by 2050 it will be 63%. In September 2022, CarbonCapture announced the development of the first large-scale commercial DAC project, known as “Project Bison.” With the implementation of policies such as the Inflation Reduction Act in the US, the outlook for DAC supply has significantly improved in recent months. Carbon removals resulting from DAC will rise to 6.1 billion tonnes of CO2 equivalent in 2050 (compared to 2.8 billion tonnes in the previous report). Additionally, prices for DAC are also expected to decrease faster, reaching a low of $88 per tonne in 2050 (compared to $99 per tonne in the previous report).

The high prices could make it difficult for most companies to participate in the market. As in the bifurcation scenario, this could lead to a split in the market with a small group of buyers seeking expensive removal offsets, and a larger group purchasing cheaper avoidance offsets. In a hypothetical avoidance market, offsets like REDD+, clean energy, and clean cookstoves would be cheaper early on, but with prices eventually reaching $32 per tonne in 2050, valuing the market at $100 billion.

Carbon offset market insights, such as those offsets in this long-term outlook, are important for sustainability managers because they provide valuable information that can help inform their decision-making and strategy-planning when it comes to carbon offsetting. By staying up to date on the latest trends and developments in the offset market, managers can gain a better understanding of the overall supply and demand for offsets, as well as the different types of projects that are available. They can also learn about the relative costs of different offset options, which can help them make more informed decisions when it comes to budgeting and allocating resources. Additionally, market insights can also provide managers with information about the potential reputational risks and benefits associated with different offset projects, which can help them evaluate the potential risks and benefits of investing in different types of offsets.

Experts can help source high integrity offset credits that allow for removal and permanent sequestration technologies to be scaled up commercially. They also work with carbon offset purchasers to understand the carbon footprint of their operations and supply chains and direct those purchases toward permanent negative emissions—the only true form of carbon offset. Those that prepare for the future will be best positioned for success. If you need help sourcing high-quality carbon removal credits to neutralize your “hard-to-abate" emissions, JS Held’s team of experts is here to help you on your journey. We can also help companies that are just starting out to understand their carbon footprint and identify carbon abatement options.

We would like to thank Steven Andersen for providing insight and expertise that greatly assisted this research.

Boards of Directors are the lynchpin to effective sustainability programs. Effective sustainability programs can only be created and maintained when there is consistent support from the management team. Without an open and apparent management team...

We discuss the options proposed by ECCC, the scope of the proposed emissions cap, and what to expect from upcoming ECCC communications regarding the emissions cap decision....

In September 2022, the U.S. Environmental Protection Agency (EPA) Region 1 issued a decision to use its Clean Water Act (CWA) Residual Designation Authority (RDA) to require National Pollution Discharge Elimination System (NPDES) permits for...