Insights

J.S. Held Acquires Shechter & Everett to Expand Forensic Accounting Capabilities for Family Law Disputes in Florida

Read MorePorts and terminals serve as the primary infrastructure for movement of goods and commodities in and out of a country and therefore play a vital role in global trade. As well as facilitating trade, ports and terminals also provide employment (such as processing and handling of goods and port-related services) and contribute to the general development of the country or region in which they are located. Without the availability of ports, transportation of goods to and from different nations would be more inefficient, which could negatively impact the global economy.

The supporting port infrastructure such as cranes, silos, tank farms and connectivity rivers, canals, road, rail, and air routes, also play a crucial part in today’s modern intermodal and multimodal distribution hubs.

It therefore follows that any interruption to that network (either insured or uninsured) could have significant financial knock-on effects.

This article defines the categories of ports and terminals and examines the most frequent types of situations that result in damage and the ensuing business interruption insurance claims. In addition to giving specific examples of such claims, it also discusses what documentation generally is needed when filing a business interruption claim.

Port congestion has recently had a negative impact on the economy with instances of port congestion in various parts of the world including the United States, Europe, and Asia. There are a variety of factors which have contributed including Covid-19, Brexit, weather events, industrial action, labour shortages, demand spikes, customs delays, and the Russia / Ukraine conflict.

Other recent examples of damages at ports and terminals include:

Other high profile maritime incidents – including the Ever Given cargo ship Suez Canal blockage [8]; the Ever Forward Chesapeake Bay grounding [9], and the Felicity Ace fire [10]– illustrate the potential values at risk passing through ports each day and the potential exposures.

The types of interruption which can arise at ports and terminals can include:

Construction Phase – Damage to jetties, breakwater, quay walls (known as “wet works”) which can be susceptible to extreme weather and sea conditions, and onshore risks such as warehouses, buildings, and handling equipment. Reclaimed land can also be susceptible in the event of liquefaction.

Delay in Start-Up – If a piece of equipment being transported by sea and destined for a project is dropped or damaged (e.g., during loading or unloading) then it can potentially give rise to a Delay in Start-Up (DSU) claim.

Port Blockage – This is when the channel is blocked by debris, or a stricken vessel, or alternatively a build-up of sand / siltation following a weather event. Often siltation from land run-off / landslip / subsidence may be excluded, or policies could require certain conditions to be complied with, such as: regular dredging, provision of depth data at the point of underwriting; and for the weather event to be of a certain type (e.g., Beaufort scale 8 or above).

Damage to cranes – A loss of a quay crane or gantry crane or other port infrastructure can impact the throughput of cargo or containers and negatively impact revenues. The impact could be more keenly felt if bottleneck equipment is damaged, or the incident occurs at a quay of greater depth to handle larger draft vessels (e.g., if only one quay is able to berth cape-size vessels).

![Container Ships / Cargo / Bulk Carrier / Supertankers [11]](/uploads/Picture3_2023-04-14-134306_xlny.jpg)

Damage to port infrastructure – For example, this is damage to specific handling facilities such as grain silos and conveyors, roll-on-roll off (RoRo) features which can result in significant interruption, should damage occur to specialist equipment.

Damage at a third-party concession – Some areas of the port may be leased to third party companies such as warehouses or storage tanks. Incidents such as fire damage to a warehouse may mean a loss of stock to the third party, but also could result in a loss of movement tariffs and charges, and stevedoring revenue to the port itself; if it results in an interruption to that business and vessels do not call as a consequence.

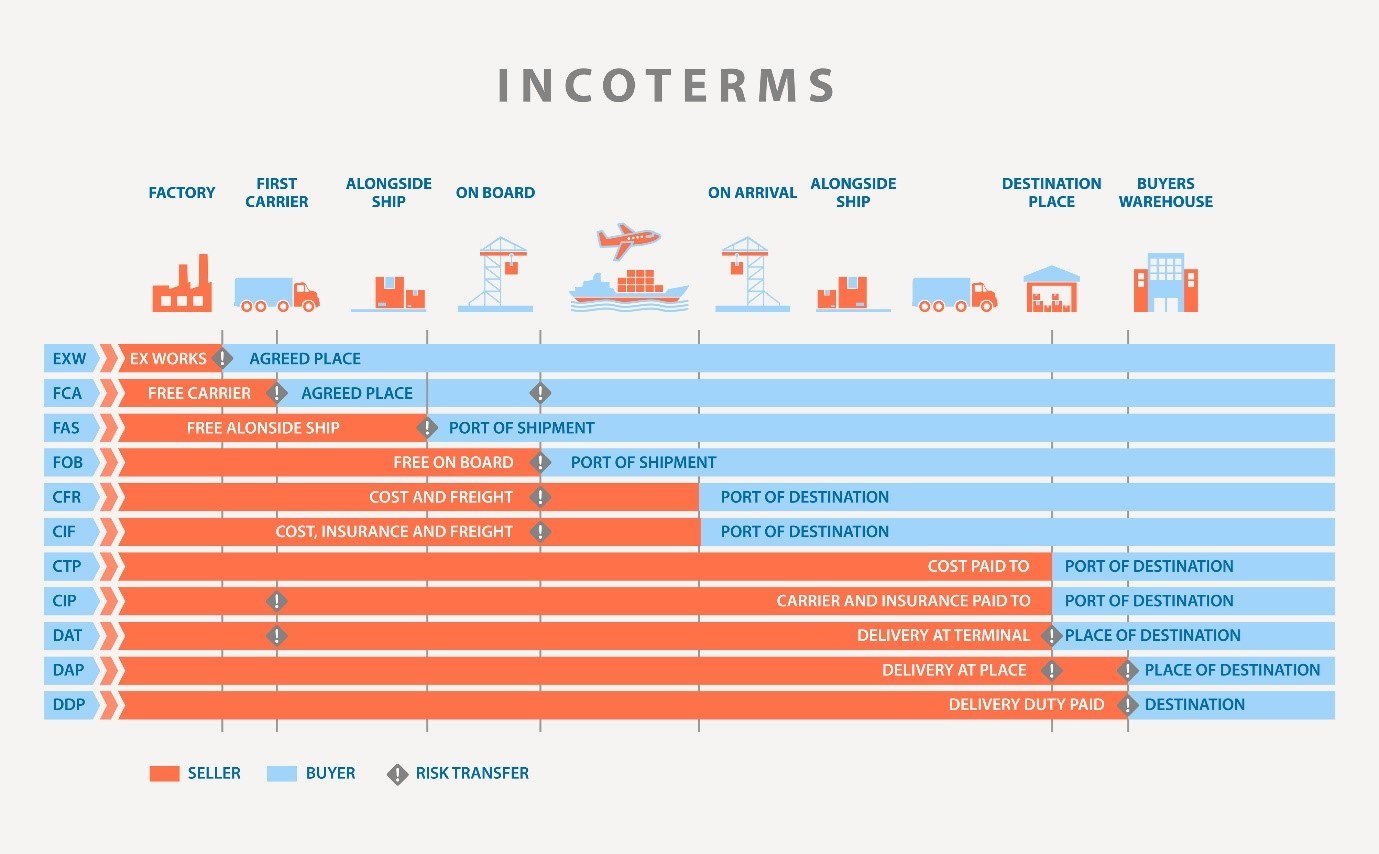

Stock or Cargo damage – It is important to check who has the responsibility to insure based on the International Commercial Terms (Incoterms) in the next graphic below. This may impact which policy responds and the basis of valuation (e.g., marine cargo policies can often be at selling price, whereas others may be valued at replacement cost). If the marine cargo policy includes a selling price valuation, it is already compensating the insured for any loss of profit element. Therefore, this may be relevant in the event a separate claim is made for business interruption.

The measurement and magnitude of loss can vary greatly depending on the specific circumstances of loss, such as the type of port (container / car terminal / break bulk or general cargo / dry bulk including grain or minerals / liquid bulk including petroleum, chemicals, or edibles) and the facilities available. Where significant constraints exist, this can negatively impact the loss and limit the ability to mitigate.

The loss of turnover or loss of profit calculation may differ depending on the revenue generation mechanism in place, whether it be:

Some shipping lines or beneficial cargo owners may have preferential terms. As a result, a customer-wise or product-wise analysis may be required, especially in the event of a partial loss.

Much of the port infrastructure and equipment cost is fixed in nature. However, some costs may cease or reduce in consequence such as labour or utilities costs associated with usage.

With respect to property damage, depending on the size and / or complexity of the claim, it may be beneficial to engage a forensic accountant to consolidate supporting restoration cost invoices. It also may be useful to retain construction advisory professionals such as quantity surveyors or project monitoring services to support evaluation of buildings or infrastructure damage. Where the restoration of damage is critical to the loss of income, timeline experts also may be vital to monitor the critical path and ensure works remain on track.

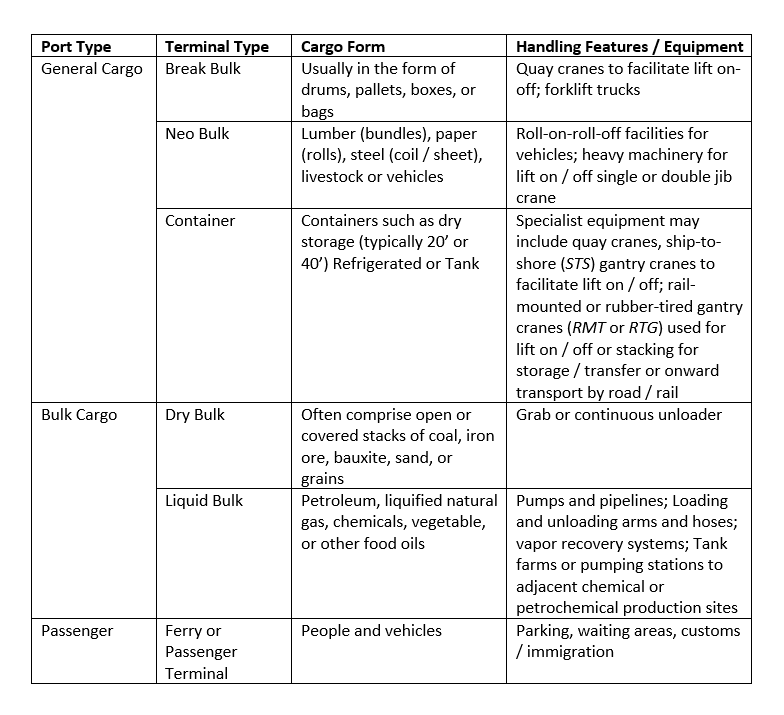

Whereas historical ports may have comprised single wharves or loading areas, modern ports and terminals encompass multimodal transportation hubs linking sea, river, road, rail, and air. While most are situated on the coast, ports can be found further inland such as Hamburg and Duisburg in Germany. Some ports are multifunctional, whereas others can specialize in specific goods, cargo, or passengers. Typically, ports are categorized as follows:

Each come with its own risks such as dust control being vital at dry bulk terminals and resulting in the use of dust covers, fogging or sprinkler systems. Grain terminals may have silos, conveyors, sieves, and bucket elevators to help calibrate the grain or allow treatment / fumigation prior to onward transport.

The capacity of terminals is determined by numerous factors, such as:

Terminal operation can be optimized by:

These constraints can be considered in the measurement of business interruption losses, by looking at historical throughput and handling statistics to establish a baseline level of operation and explore the possibility of loss mitigation depending on the damage sustained.

The extent to which the loss can be mitigated depends on the circumstances of the loss.

For example, a container port with multiple terminals and quay cranes would likely be able to mitigate the loss of a damaged quay crane by simply diverting vessels from one terminal to another. Meanwhile, a general cargo concession with a single crane, which incurred damage, may result in the diversion of the vessel to another concession either at the same port or a port nearby.

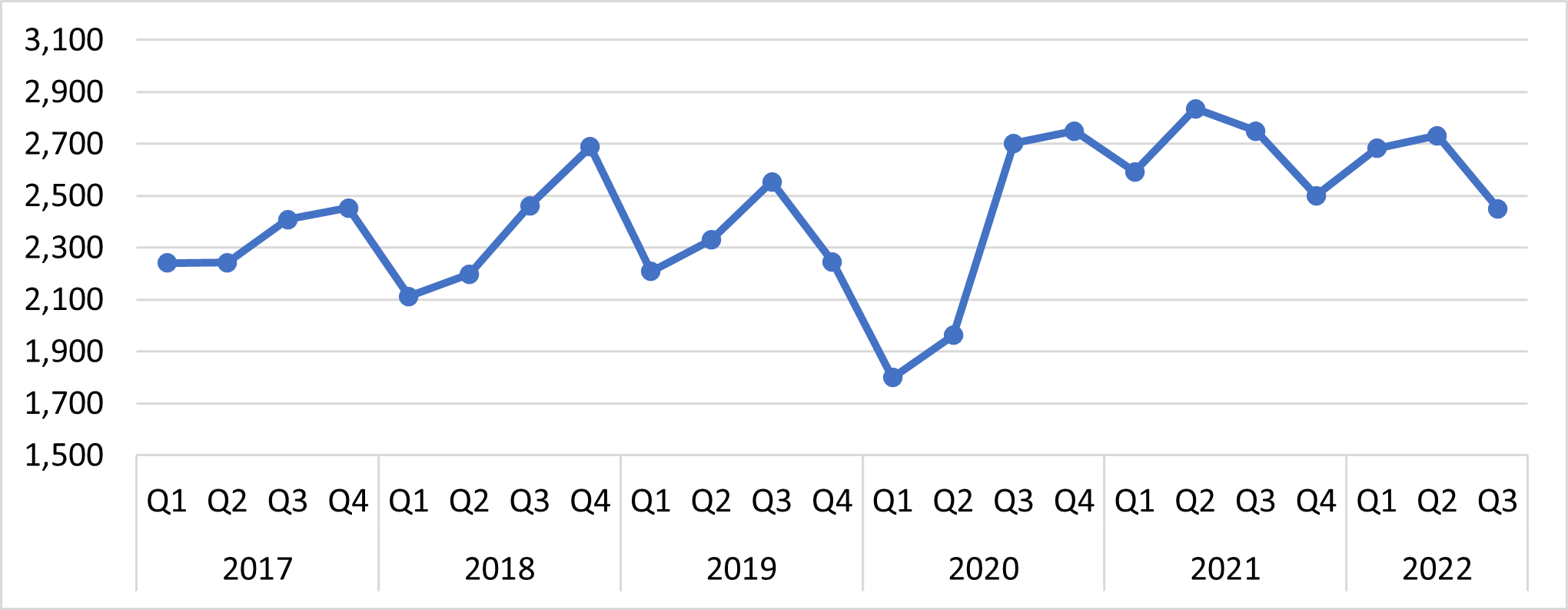

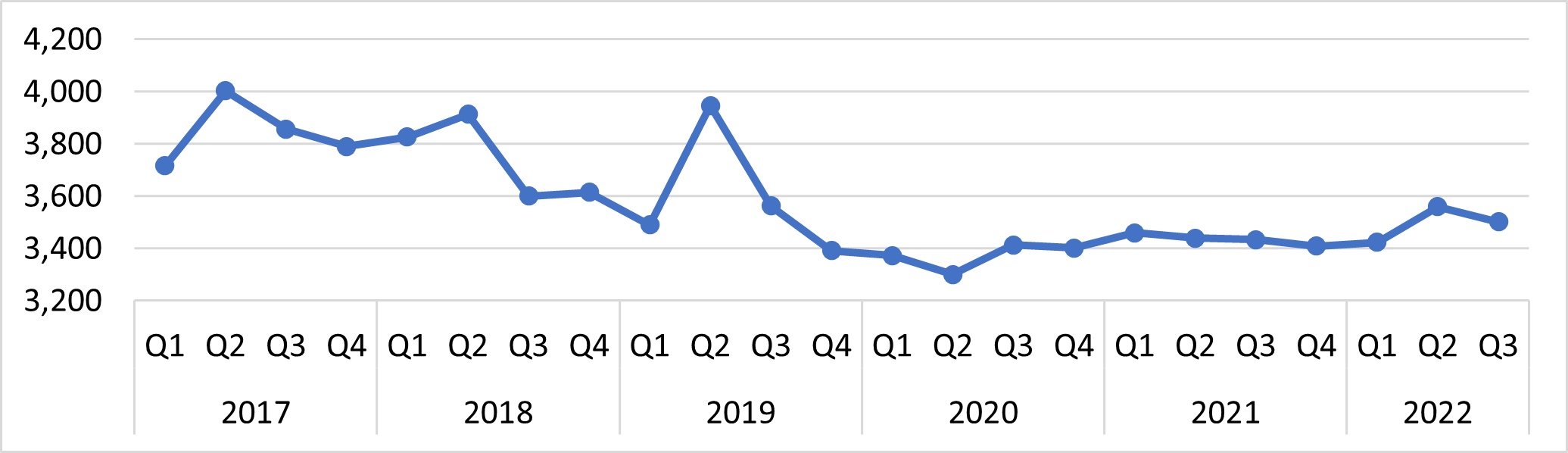

The operating capacity of the port could also play a part in the extent to which a loss can be mitigated. Figure 1 shows the throughput at Los Angeles container port in thousands of twenty-foot equivalent units (TEUs). A clear drop in Q1 2020 can be seen, showing the effects of Covid-19, whereas during 2021 and 2022, throughput was consistently higher than pre-Covid, therefore more likely that damage could result in a revenue loss.

Conversely, Figure 2 shows that Jebel Ali Port in Dubai is currently operating below its capacity with extra capacity due to be added in future with the addition of Terminal 4 [12] to facilitate further expansion. Recent publicized incidents such as the Centaurus Quay Crane collision [13] and Ocean Trader explosion [14] were said to have minimal operational effects.

While not all incidents result in business interruption insurance claims, here are some examples of ports and terminals claims over the years:

Example 1:

Coal was being transported from mines by rail to Port A. The coal delivery was impacted by damage to the railway line and had to be diverted to Port B. The coal handling revenue was therefore earned by Company B (which operated the coal terminal at Port B) rather than Company A (which operated the coal terminal at Port A). This led to a contingent business interruption loss to Company A.

Example 2:

A grain terminal suffered a fire, damaging grain silos and associated conveyors. The loss of handling and storage revenue was not as significant as it could have been due to the timing of the incident which did not coincide with the peak seasonality for harvest. Review of berthing plans, historic grain handling volume data, and storage statistics facilitated projections of the “but-for” revenue position.

Example 3:

A container quay crane was hit by a container ship in the process of berthing, causing the crane to collapse. Excess capacity was available across the remaining container terminals, meaning losses were limited to increased costs such as inter-terminal transfers (ITT). The losses would have been much larger had the port been at or close to throughput capacity.

Example 4:

Siltation of channel following a cyclone resulted in the inability of the port to handle cape-size vessels. This resulted in a loss of imports until the required dredging work was carried out. Calculation of financial losses were undertaken on a without prejudice basis due to the concurrent legal dispute about the cause of the channel blockage and whether the policy had been triggered.

Example 5:

Quayside equipment was damaged following a cyclone, resulting in a loss of imports as vessels were diverted to other ports in the vicinity. A claim was also submitted for loss of exports. However, upon further investigation, the drop in exports post loss was followed immediately by a spike in activity once the damage had been rectified. After further discussion with the insured, the agreed goods for export remained at the port and were exported at the next available opportunity.

Example 6:

A vessel hit a loading arm at a petroleum storage terminal causing irreparable damage, with a lead time of six to 12 months for replacement. One of the remaining loading arms was converted from black oil (e.g., crude oil, furnace oil, fuel oil, tar, and asphalt) to white oil (refined petroleum products such as gasoline, benzene, kerosene, and diesel fuel) to mitigate the loss as the majority of the demand (and hence revenue generation) related to white oil petroleum product handling and storage. The business interruption loss was therefore limited to the additional cost of parts and labour for the conversion but represented a small percentage of the potential loss when considering the exposure of lost fuel handling income and tank storage revenues. Black oil handling was effectively sacrificed during the maximum indemnity period. However, it successfully mitigated around 90%-95% of the potential loss.

Example 7:

Fire at a petroleum tank farm resulted in damage to gasoline products. During the course of the firefighting, the loss was mitigated by evacuating product to adjacent undamaged tanks. The measurement was complicated by firefighting water being comingled with petroleum product which had to be considered when observing the tank measurements and readings. Finished product was also evacuated back to tanks containing crude oil, resulting in some discussion in relation to the valuation and reprocessing.

Example 8:

A cyclone caused damage to a chemical manufacturing facility and the adjacent port. Stock was damaged at both the factory site and to goods outbound and feedstocks inbound. A detailed study was undertaken in relation to the incoterms of the products to determine the transfer of risk, thus enabling the correct apportionment between separate stock and marine cargo policies and the respective valuations.

When evaluating a business interruption under Ports and Terminals coverage, we would typically review:

Of course, the documentation required can vary on a case-by-case basis, tailored to the circumstances of loss. As always, it is prudent to have off-site or cloud back-up in the event of catastrophic loss.

Sometimes claims are presented for ICW such as increased internal moves or inter-terminal transfers (ITT). One example would be a workaround to avoid a loss of handling revenue. As the amounts charged may be intercompany (i.e., between one department and another), it is important to examine the basis of the charges to ensure allocations of fixed costs and / or profit elements are not being included if it is a group policy.

Sometimes other costs claimed such as dredging / re-dredging or demurrage may be specifically excluded; sub limited or subject to certain conditions (e.g., periodic provision of dredging records / hydrological and / or hydrodynamic surveys); although they are sometimes put forward on the basis that it has mitigated a reduction in turnover, which could require careful consideration by Insurers.

Prior to any potential claim happening, companies should consult with their broker to ensure appropriate cover is in place. Additionally, contracts should be updated on a regular basis including relevant extensions and values. Typical coverage can include:

It is also important to have a business continuity or recovery plan, identifying key risks faced and the planned emergency response, crisis management, IT system recovery, process, and equipment resumption. Consider potential loss scenarios or what-if analysis.

Risk managers can identify in advance who or which department is responsible for gathering data and information to prepare and provide evidence for the claim. From a property damage or increased costs perspective, separate ledger accounts, collation of purchase orders, and invoices can all assist in tracking loss-related costs. Providing evidence of the business interruption loss may require collation of operational, revenue and other accounting data. It would be ideal and prudent to identify certain personnel ahead of time and give them some indication about the type of records required to substantiate the costs and losses incurred.

Prompt notification of the claim allows early appointment of loss adjusters and experts by the insurance company. Preserve evidence, whether that be CCTV footage, photographic substantiation, or accounting records. In resuming operations as quickly as possible, be sure to communicate with the adjuster on planned work and expenditure to ensure no misunderstanding.

The critical role of ports and terminals to the economy is clear, and the interruption to operations can be costly from a loss of revenue or property damage perspective. Although the risks may be mitigated and / or transferred via appropriate insurance programmes, as you can see from the examples above, claims do happen.

Retaining a forensic accountant early can provide tremendous value to the claims review process. Given their unique skill sets and experience managing large or small ports and terminals claims globally, they can prove to be invaluable resources for insurance companies, independent adjusters, and law firms.

We would like to thank Daniel Thorpe and Deborah Ford for providing insight and expertise that greatly assisted this research.

Daniel Thorpe is an Executive Vice President in J.S. Held’s Forensic Accounting – Insurance Practice. Based in Dubai, UAE, he has more than 15 years of experience, having specialized in forensic accounting since 2006. Prior to joining J.S. Held, Daniel opened and established the regional office of another forensic accounting firm in the Dubai International Financial Centre and has quantified some of the largest Business Interruption, Delay in Start Up / Advanced Loss of Profit claims in the Middle East and Africa (MEA) region over recent years. Prior to that, Daniel was based in London and Asia. He had extensive involvement in catastrophe losses in Japan and Thailand. Daniel has worked extensively in the areas of powergen (fossil fuels and renewables), petrochemical manufacturing; metals, alloys, and compounds; food and beverage manufacturing; automotive manufacturing; hotel and resorts; ports and terminals; and retail.

Daniel can be reached at [email protected] or +971 4 881 3199.

Deborah Ford is a Vice President in J.S. Held’s Forensic Accounting - Insurance Services Practice. Deborah specializes in forensic accounting and the analysis of economic damages. With nearly 20 years of experience, she provides expert forensic accounting services for insurers, adjusters, and attorneys in the U.S. and overseas. She specializes in the financial evaluation of damages for diversified matters dealing with quantifying business interruption, extra expense, cargo/marine, subrogation, and insurance defense. She has been involved in over 750 cases, including claims of up to $500 million. Her industry experience includes, but is not limited to aerospace, apartments, casinos, construction, distribution, gaming, government, health services, hospitality, hospitals, life sciences, manufacturing, professional services, restaurants, retail, and warehousing. She has testified as an expert witness in California, Delaware, and federal courts.

Deborah can be reached at [email protected] or +1 949 390 7473.

[1] https://www.bbc.com/news/world-middle-east-53668493

[3] https://www.bbc.com/news/world-middle-east-61950965

[4] https://www.reuters.com/news/picture/deadly-bangladesh-container-depot-fire-b-idUSKBN2NO08J

[6] https://www.reuters.com/business/fire-indonesias-pertamina-refinery-complex-extinguished-2021-11-13/

[7] https://splash247.com/ship-capsizes-at-indian-port/

[8] https://www.bbc.com/news/business-56559073

[10] https://www.bnnbloomberg.ca/porsches-and-lamborghinis-lost-at-sea-may-be-worth-155-million-1.1726520

[11] Graphics adapted with permission from The Geography of Transport Systems, Jean-Paul Rodrigue. For container ships. TEU refers to 20-foot equivalent units.

[12] https://www.dpworld.com/en/uae/ports-and-terminals/jebel-ali-port

[13] https://www.porttechnology.org/news/watch_cma_cgm_containership_collides_with_dpw_quay_crane/

Forensic accountants assist in Marine Insurance cases in a variety of ways, regardless of the cause of loss or type of damages. The purpose of this paper is to discuss a variety of different marine...

Insurance claims for loss of inventory are generally examined by insurance carriers. The carrier will retain a forensic accountant who has the ability to quantify out of sight inventory losses. Out of sight inventory losses...

The purpose of this paper is to discuss some of the major work and financial matters forensic accountants focus on, including fraud investigations and insurance claims, and how they bring unique value to the process....