Insights

J.S. Held Acquires Shechter & Everett to Expand Forensic Accounting Capabilities for Family Law Disputes in Florida

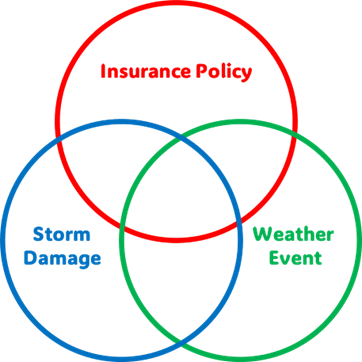

Read MoreProfessional meteorology, as it relates to insurance claims handling and the litigation process, is becoming increasingly recognized, and the employment of meteorologists within the insurance industry is growing. But what does meteorology have to do with storm damage insurance claims? A simple Venn diagram explains the key, but often overlooked, reason: the storm(s) that are claimed matter.

Figure 1 – A basic illustration of the overlap between insurance, storm damage, and weather events.

Ultimately, there are three main facts that must apply for a storm damage insurance claim:

Simply put, no two factors for a storm damage insurance claim alone provide a full picture of insurance carrier liability when considering coverage for a storm damage insurance claim. A storm must result in covered damage during an applicable insurance policy coverage period.

In this article, we discuss the role of forensic meteorologists when consulting on matters of storm damage related claims and disputes. This information is intended to assist insurance adjusters and attorneys in resolving claims and related disputes concerning storm damage in an accurate, timely, and cost-effective manner.

Meteorologists are not tasked with considering policy coverage or identifying the claimed damages; rather, they assist clients in determining the weather events that may or may not apply to the policy for the claimed loss.

Most meteorologists are not damage experts, nor do they testify to the causation or nature of claimed damages. However, sometimes a distinct correlation between claimed damages and severe weather can be drawn, such as the path of a tornado, or a significant flooding and/or storm surge event.

Likewise, insurance adjusters are policy experts, appraisers are appraisal experts, and building consultants, architects, and engineers are damage experts. While it is important that these professionals correlate weather events to claimed damages and insurance policies, the best source of weather information and expertise is a weather expert—a meteorologist.

Despite the rising popularity of enlisting the help of meteorology experts in insurance claims and litigation, one of the most common reasons meteorologists are not retained is because of the perception that “the damage (or lack thereof) speaks for itself.” No doubt, if both parties agree on everything related to the claim, then this is a reasonable assertion.

However, when the damage and/or policy application (including appraised value) is disputed by involved parties, the third circle of the insurance claim Venn diagram (the weather event) can provide vital evidence that ultimately supports or conflicts with certain facts of the insurance claim as presented.

Consider the following frequently encountered scenarios:

These instances are just a few of many where a credentialed forensic meteorologist can assist in the insurance claims and litigation process. These examples also demonstrate the incredible synergy between insurance adjusters and appraisers, damage experts, and meteorologists.

In some of the most contentious insurance claims in which forensic meteorologists are retained, the damage itself is very much disputed, and, therefore, the application of the policy hangs in limbo, as does the potential financial liability. However, once weather experts are retained to provide scientifically accurate weather opinions, these insurance claims often result in a timely and agreeable resolution.

If you or your organization are engaged in a storm damage claim at risk of becoming stalled, prolonged, or otherwise complicated due to a dispute regarding the facts of a weather event or storm(s), be sure to enlist the help of expert forensic meteorologists early in the process to avoid or reduce unnecessary additional resolution time or costs.

We would like to thank our colleague Daniel Schreiber, CCM for providing insights and expertise that greatly assisted this research.

Daniel Schreiber is a Senior Vice President in J.S. Held's Forensic Meteorology service line. He is a Certified Consulting Meteorologist with over 10 years of experience in military, aviation, and severe weather operations. Mr. Schreiber has provided consulting and expert services for both plaintiff and defense law firms, as well as insurance adjusters, appraisers, umpires, and policyholders throughout North America. He has been consulted and/or retained as an expert in over 850 matters and has testified in both depositions and during trials in state and federal courts. He regularly plays an integral role in multi-million-dollar insurance disputes and injury/wrongful death lawsuits from coast to coast. Before joining J.S. Held, Dan was a highly successful meteorology business owner.

Dan can be reached at [email protected] or +1 830 453-0255.

How meteorology consultants help evaluate the risk of future severe weather events and work with forensic accountants to ensure that losses are accurately represented in insurance claims....

Consulting with a professional meteorologist regarding reported (or conversely, unreported) storm events is fundamentally crucial to understanding a storm’s occurrence (or lack thereof) for insurance claims. Find out why....

We discuss hazardous weather events by geography in the US, and why considering these events is important for understanding underwriting risks and handling post-storm insurance claims....