Insights

J.S. Held Acquires Shechter & Everett to Expand Forensic Accounting Capabilities for Family Law Disputes in Florida

Read MoreDid you know that a residential structure is three times as likely to experience a flood than a fire over the 30-year life of a mortgage? In fact, flooding is the most common type of natural disaster in the United States and worldwide. Within the past five years, every state in the United States has experienced a flood event, yet only about 27% of American households have reported they carry flood insurance policies.

This white paper provides general knowledge about the Federal Emergency Management Agency’s (FEMA) National Flood Insurance Program (NFIP), including floodplain management, substantial damage, substantial improvements, and requirements for compliance. This paper is intended as a general overview, is not comprehensive in nature.

Legislation regarding floodplain management and protection dates back as early as 1824. At one time, the private insurance industry included coverage for flood losses, but it abandoned such coverage in 1929 following the Great Mississippi River Flood of 1927. A series of legislations regarding flood insurance were proposed after 1929, but all ultimately failed until The National Flood Insurance Act of 1968 (Title XII of the Housing and Urban Development Act of 1968 [PL 90-448]) was passed and the National Flood Insurance Program (NFIP) was created, providing the public with federally backed access to flood insurance.

Since the inception of the NFIP, other notable historical legislations affecting flood insurance have included:

Legislation regarding floodplain management and protection dates back as early as 1824. At one time, the private insurance industry included coverage for flood losses, but it abandoned such coverage in 1929 following the Great Mississippi River Flood of 1927. A series of legislations regarding flood insurance were proposed after 1929, but all ultimately failed until The National Flood Insurance Act of 1968 (Title XII of the Housing and Urban Development Act of 1968 [PL 90-448]) was passed and the National Flood Insurance Program (NFIP) was created, providing the public with federally backed access to flood insurance.

Since the inception of the NFIP, other notable historical legislations affecting flood insurance have included:

The NFIP is a voluntary federal program that provides residents living in participating communities affordable insurance to protect against flood losses. Participation in the NFIP requires communities to meet or exceed the floodplain management regulations and requirements set forth by the NFIP. The ultimate goal of the NFIP is to mitigate the impacts of flooding on private and public structures.

The four key elements of the NFIP are:

The NFIP identifies and maps flood risks on a Flood Insurance Rate Map (FIRM), which identifies the flood zones within each Special Flood Hazard Area (SFHA). The SFHA includes the areas with a 1-percent annual chance of being inundated by a flood, and the base flood elevation (BFE) is the elevation at which the 1-percent flood would occur. It is important to realize that each year approximately 20-25 percent of all flooding occurs outside of the SFHA in the “X” or other low risk zones. Flood maps for the entire United States can be accessed via the FEMA Map Service Center online website at msc.fema.gov.

Floodplain management is the operation of a community program of corrective and preventative measures for reducing flood damage by developing and enforcing requirements for zoning, subdivisions and buildings, and special-purpose ordinances.

In order for a structure to be eligible for flood insurance through the NFIP, it must be principally over dry land, and not over water. Flood insurance is available for all qualifying structures both within and outside of the SFHA.

One of the objectives of the NFIP is to prevent repetitive flood losses to structures. In order to mitigate the risk to repetitive loss structures, the NFIP established substantial improvement and substantial damage (SI/SD) requirements. The SI/SD requirements are the responsibility of the local community’s authority having jurisdiction including the floodplain manager and building official.

The NFIP and International Building Code (IBC) both define substantial improvement and substantial damage as follows [5]:

Substantial Improvement refers to any reconstruction, rehabilitation, addition, or other improvement of a structure, the cost of which equals or exceeds 50 percent of the market value of the structure (or smaller percentage if established by the community) before the “start of construction” of the improvement. This term includes structures that have incurred “substantial damage,” regardless of the actual repair work performed. The term does not, however, include either:

Substantial Damage refers to damage of any origin sustained by a structure whereby the cost of restoring the structure to its before damaged condition would equal or exceed 50 percent of the market value of the structure before the damage occurred. Work on structures that are determined to be substantially damaged is considered to be substantial improvement, regardless of the actual repair work performed.

Substantial improvement and substantial damage requirements only apply within a Special Flood Hazard Area (SFHA).

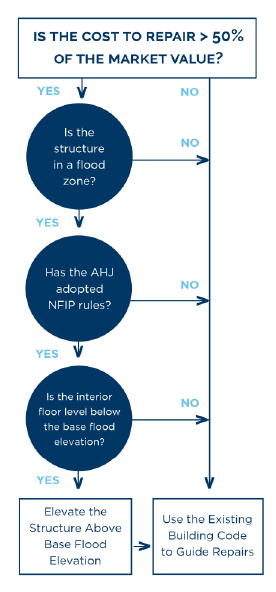

The requirements of substantial improvement and substantial damage are often misinterpreted, but it is important to understand exactly what triggers these requirements. In order for substantial improvement or substantial damage regulations to apply:

Per the chart below, If any of these requirements do not apply, the substantial improvement or substantial damage requirements are not triggered, and the current building code governs the improvement or repair. It’s important to remember that substantial improvement and substantial damage rules apply even when the property is not insured for flood coverage.

Substantial improvement and substantial damage determinations can only be made by local officials who are responsible for administering their floodplain management regulations or codes.

Improvement or repair costs are determined by itemized costs, building valuation tables, qualified estimates, owner-prepared cost estimates with supporting documentation, or FEMA’s Substantial Damage Estimator software. The pre-improvement or pre-damaged market value of a structure is determined using appraisals, values used for property tax assessments, estimates of a structure’s actual cash value including depreciation, and qualified estimates based on the professional judgement of a local official.

The elevation of the structure is determined using the FEMA Elevation Certificate (EC), which identifies the elevation of the structure above the Base Flood Elevation (BFE) for the specific geographic location. If an EC is not available or has not been previously recorded, one will be required to determine if the structure is indeed below the required elevation and, if so, how much it would need to be elevated to achieve compliance.

The FEMA publication P-758: Substantial Improvement/Substantial Damage Desk Reference provides further information and answers to frequently asked questions about substantial improvement and substantial damage. FEMA 213: Answers to Questions About Substantially Improved/Substantially Damaged Buildings is also a good resource for common questions related to SI\SD. Both publications are available online through the FEMA website [1] [6].

If improvements or repairs have triggered the requirements for substantial improvement or substantial damage, the structure must be brought into compliance with the floodplain management requirements for new construction based on the specific flood zone in which the building is located, with the NFIP requirements as the minimum standard and building code flood design requirements for new construction.

Substantially improved and substantially damaged structures are not required to be brought into full compliance with all the provisions of building code for new construction.

The minimum NFIP requirements for compliance include:

The standard NFIP flood insurance policy has coverage of up to $30,000 for Increased Cost of Compliance (ICC), which can be used to bring a substantially damaged structure into compliance; however, this coverage can only be accessed if the structure has sustained flood damage exceeding the 50% threshold. The ICC coverage can typically be used in four different areas, including floodproofing (non-residential structures only), relocation, elevation, and demolition. If a structure has been damaged by another peril (wind, tornado, fire, etc.), is located within the SFHA, and has triggered the requirements for substantial damage, the structure must still be brought into compliance with the flood requirements of the NFIP and building code, but no increased cost of compliance coverage can be accessed from a flood policy. In addition, the ICC amount cannot be combined to the policy coverage to exceed the maximum amount or policy limits of the coverage.

Improvements to non-damaged structures such as additions or owner-elected renovations, can also trigger the requirements of the 50% rule. In these instances, determination must be made as to the type of improvement, the relationship to the existing structures, and what elevation requirements will be required of both the new areas of construction as well as the existing building.

As floodplain management regulations continue to evolve, it is important for design professionals and insurance professionals to understand how to interpret these regulations. The substantial improvement and substantial damage definitions and requirements are arguably the most misinterpreted floodplain regulations. Many times, those involved in a project such as the design professional, contractor, or property owner are not aware of these requirements until their application for repair permitting is denied by the local building department. Knowing how to interpret and implement these requirements is critical for floodplain management compliance and for mitigating the risks from future flooding.

We would like to thank Erin Roberts, PE, CFM and Michael Rimoldi, CBO, CFM who provided insight and expertise that greatly assisted this research.

Erin Roberts is a Senior Engineer in J.S. Held’s Forensic Architecture & Engineering Practice. Erin has over five years of experience in the industry and has managed and completed projects in excess of 300 million dollars. She established her career in working for several engineering and design companies where she encompassed many roles. These roles included, but were not limited to, engineering design, inspection of new and existing buildings, structural damage assessments, business development, pre-construction, construction administration, and project management. Erin’s expertise is in structural damage assessments, hazard mitigation, and building code interpretation with regards to code-required upgrades to existing structures.

Erin can be reached at [email protected] or +1 470 989 6193.

Michael Rimoldi is a Senior Project Manager in J.S. Held’s Forensic Architecture & Engineering Practice. In addition to applying and interpreting the building codes, Michael is a licensed building contractor who has worked on both residential and commercial projects of various scopes. He is an ASFPM Certified Floodplain Manager and a credited reviewer of several FEMA construction-related documents including the Coastal Construction Manual, the Local Officials Guide to Coastal Construction and Natural Hazards and Sustainability for Residential Buildings. He has appeared on several national media outlets discussing building codes and construction including CNN, Good Morning America, and The Weather Channel.

Mike can be reached at [email protected] or +1 813 390 3935.

[1] Federal Emergency Management Agency. (2010). FEMA P-758: Substantial Improvement/Substantial Damage Desk Reference. Federal Emergency Management Agency. https://www.fema.gov/sites/default/files/documents/fema_nfip_substantial-improvement-substantial-damage-desk-reference.pdf

[2] Federal Emergency Management Agency. (2017). NFIP Desk Reference Guide For State Insurance Commissioners and Others. Federal Emergency Management Agency.

[3] Federal Emergency Management Agency. (2020). National Flood Insurance Program Elevation Certificate and Instructions. https://www.fema.gov/media-library/assets/documents/160

[4] Insurance Information Institute, Inc. (2017). Facts + Statistics: Flood Insurance. Retrieved from Insurance Information Institute: https://www.iii.org/fact-statistics-flood-insurance

[5] International Code Council. (2017). 2018 International Building Code. County Club Hills, IL: International Code Council Inc.

[6] Federal Emergency Management Agency. (2018). FEMA P-213: Answers to Questions About Substantially Improved/Substantially Damaged Buildings. https://www.fema.gov/sites/default/files/2020-07/fema_p213_08232018.pdf

[7] The American Institutes for Research. (2005). A Chronology of Major Events Affecting The National Flood Insurance Program. The American Institutes for Research Completed for the Federal Emergency Management Agency.

While some hazards are readily visible and easily noticeable, others are hidden. Whether it’s a roof evaluation or a major fire to a manufacturing plant, being properly prepared for site hazards with adequate equipment for...