Insights

J.S. Held Acquires Shechter & Everett to Expand Forensic Accounting Capabilities for Family Law Disputes in Florida

Read MoreFollowing the easing of Covid pandemic restrictions, we are now facing a fresh “cost of living crisis” created by rising inflation and soaring energy bills.

The Guardian newspaper reported that forecourts at petrol stations face up to 3,000 attempted fuel thefts a month as fuel prices soar. Additionally, there was a 39% increase of non-payment between January and May in 2022 based on the figures from Forecourt Eye, a company that collects payments on behalf of about 1,000 garages around the United Kingdom. [1]

The insurance market is also predicting an increase in fraudulent claims as the cost-of-living crisis deepens [2]. For example, NFU Mutual, the UK's leading rural insurer has warned rising food prices will see livestock thefts increase. Furthermore, its rural crime claims pay-outs between January and March 2022 were more than 40% higher than the same period in 2021 [3].

As forensic accountants, we are directed to where a fraud has already been identified or where one has not, but it emerges during the normal claim review process. We also are asked to review unexplained physical losses which can often turn out to be innocent accounting errors.

Inventory losses are common in property claims but with the increase in warehouse cover being written under Marine policies, we are increasingly being involved in claims in this class of business. Moreover, since the Basis of Valuation is often selling price, the stakes are often higher.

This article focuses on mysterious disappearance of inventory, how to identify the difference between accounting error and physical theft, the accuracy of accounting records, and how to review the associated claims.

After physical inventory counts are undertaken, it is not uncommon for policy holders to identify a shortfall between their accounting records and physical inventory/stock on hand and assume the difference is a physical theft. They then file an insurance claim on the basis of theft, missing goods, or mysterious disappearance. One of the key questions in these cases is whether the shortfall identified is a physical theft or an innocent accounting error.

Inventory totals per the accounting records and the physical inventories on hand should match as the accounting records should mirror what the policy holder has in their warehouse. Differences arise between these two data sources due to reasons such as timing differences, physical count errors, unregistered returns, damaged goods, and more. Once identified, the accounting records of the physical inventory record should be adjusted to reflect the actual physical inventories on hand. When these adjustments are not made, they will cause variances between the accounting record and the physical inventory which may appear to be a physical loss but, in reality, are an accumulation of innocent accounting errors.

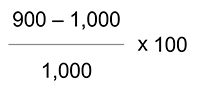

For example, there may be 1,000 items shown in the accounting records and only 900 items held at the warehouse. Therefore, it appears that 100 items are missing, and this could form the basis of a claim. However, if the accounting records have not been updated to account for 100 goods which in fact were sold or in transit but not recorded as such, there has not been a loss. It is just an accounting error.

An inventory variance rate is a measurement to show the accuracy of the accounting record compared to the physical inventory counted.

In the previous example, the variance is 10%.

What is a normal level of variance will depend on the type of company and industry.

Some experts view an inventory variance greater than 5% in the retail industry as significant [4] and in need of investigation. It is also important that these variances are corrected properly at the end of accounting period so that the variances do not accumulate over time.

For example, consider an alleged inventory theft claim where the policy holder had not conducted any physical inventory counts for more than five years. The policy holder subsequently undertook a physical count and found a 20% shortfall between the accounting records and physical count, and this formed the basis of the claim. The missing inventory volume is likely to include an element of accounting errors due to a lengthy period without checking for errors. Furthermore, a physical loss would have been prevented and detected sooner if the policy holder had conducted physical inventory counts at least annually and ideally more regularly.

Lack of proper internal controls usually leads to an increased risk of missing inventories and delayed detection. Based on the 2021 Global Fraud Survey [5] conducted by the Association of Certified Fraud Examiners (“ACFE”), the most common factor underlying the occupational frauds was a lack of internal controls. However, before jumping to the conclusion of the missing inventories being due to theft, there could be several internal control issues contributing to the missing inventories that are not due to theft. For example, poor accounting procedure (i.e., accounting errors as discussed above), an employee training issue, inaccurate counting procedures, poor handling of returns, or timing issues with the recording of goods in transit.

In most inventory loss reviews, we request the following information regarding the inventory control system to understand the normal controls and procedures in respect to the physical inventory. Below are examples of typically requested documents. If these are not available, we would ask for other material.

By reviewing the above, we can identify the normal level of inventory variances, whether these variances have been rectified, and whether a policy holder has good internal controls over its inventory. This helps us to determine whether the apparent stock loss is more likely to be an accounting error.

In a time of a cost-of-living crisis, insurers are expecting an increase in fraudulent insurance claims, including marine stock throughput claims. Our role as forensic accountants is to validate the actual loss being sustained via careful analysis and detailed review of the supporting accounting records. But it is not uncommon for alleged disappearances to turn out to be an accumulation of accounting and procedural errors.

We would like to thank Lumi Ishikawa and Joe Aldous for providing insight and expertise that greatly assisted this research.

Lumi Ishikawa is a Vice President in J.S. Held’s Forensic Accounting -- Insurance Services Practice. She joined the company’s London office in 2022 and specializes in large complex business interruption and inventory loss claims. Lumi prepares calculations and reports for use in insurance claims, mediations, and litigation disputes for companies in various sectors, including industrial manufacturing, renewable energy, marine (stock throughput), hospitality and leisure, and retail.

Lumi can be reached at [email protected] or +44 20 4574 5262

Joe Aldous is an Executive Vice President and leads the forensic accounting team in Europe as part of J.S. Held’s Forensic Accounting -- Insurance Services Practice. Based in London, he oversees all financial investigation services in the region for matters involving business interruption/loss of profits, delayed start-up (DSU)/soft costs, inventory loss, fraud, and economic damages. Joe is a Fellow of the Association of Chartered Certified Accountants and a Certified Fraud Examiner. He has been quantifying large complex business interruption/loss of profit claims (arising from fire, flood, windstorm, fraud, pandemic, and cyberattack) and preparing expert witness reports and calculations for courts, mediation, and arbitration for over 20 years.

Joe can be reached at [email protected] or +44 20 4534 0422.

Forensic accountants assist in Marine Insurance cases in a variety of ways, regardless of the cause of loss or type of damages. The purpose of this paper is to discuss a variety of different marine...

Insurance claims for loss of inventory are generally examined by insurance carriers. The carrier will retain a forensic accountant who has the ability to quantify out of sight inventory losses. Out of sight inventory losses...

The purpose of this paper is to discuss some of the major work and financial matters forensic accountants focus on, including fraud investigations and insurance claims, and how they bring unique value to the process....