Insights

J.S. Held Acquires Shechter & Everett to Expand Forensic Accounting Capabilities for Family Law Disputes in Florida

Read MoreCalifornia wine country has been devastated by multiple wildfires in recent years, and the region will likely experience more fires for years to come. Wineries are impacted by the fires in many ways, but some of the most sizeable and complex claims relate to the destruction/damage of wine inventory.

The purpose of this paper is to:

Starting in the early hours of August 16, 2020, Northern California experienced a weather phenomenon, described by a state fire official as “a historic lightning siege.”[1] Over a 72-hour period, California was hit with nearly 11,000 bolts of lightning that triggered fires engulfing over a million acres of land (collectively referred to as the Lightning Complex fires).[2]

One of the regions most affected by the fire is the famous California wine country of Napa and Sonoma. The LNU Complex fires include multiple fires burning in the region, have caused thousands of people to evacuate, and, so far, have damaged almost 1,500 structures.[3]

The region is no stranger to dealing with wildfires, having experienced several substantial wildfires over the last few years, including:

Other California winegrowing regions have also been impacted by wildfires in recent years, including:

These wildfires represent some of the largest and most destructive in state history,[4] with experts attributing them to the effects of climate change, increased development, and unsuccessful fire management strategies.[5] Whatever the reason, wildfires are likely to continue to impact California wineries in years to come.

The wildfires result in a wide variety of claims including business income losses, property damage, extra expense, crop damage, and inventory losses. This article will address claims related to the impact of the fire on wine inventory.

Wine does not have to be destroyed outright to be affected by a fire. In fact, the wine-making process can be impacted in several other ways.

Smoke Taint

The most common issue we see leading to wine-related claims after a wildfire event is smoke taint. Simply put, this means the wine tastes “smokey” with an “ashy” aftertaste. Although there is no evidence this is harmful to consumer’s health, unsurprisingly, a blind sensory study described by the Australian Wine Research Institute showed that “consumers gave very low liking scores for a smoke affected wine compared to an unaffected wine.”[6] Wine tasters often describe the flavor as that of burnt rubber, or akin to licking an ashtray.

In some cases, the winery may attempt to filter and process the wine to remove the smoke taint; however, this process can also affect the quality of the wine. Ultimately, if the wine is significantly smoke tainted, the winery will not want to sell the wine under their labels.

How Does Smoke Taint Occur?

Smoke taint can occur as a result of direct contact with smoke residue or through contact with aroma compounds released by fires. The aroma compounds, known as volatile phenols, permeate grape skins and bond with sugars in the grape to form glycosides. The glycosides do not have a smokey aroma;[7] however, during fermentation (and over time when barreled or bottled), the glycosides break down, releasing the phenols and the smokey flavor. As a result, the smoke taint may not be detected for months or even years after the loss event.

Whether or not grapes become smoke tainted can be impacted by a variety of factors, including:[8]

How Is Smoke Taint Detected?

In most incidences, smoke taint is initially detected when the wine is sampled by the in-house winemaker at the winery. After smoke taint has been detected, the winery typically sends samples to a third party for testing, where they will test for six volatile phenols that lead to the smoke taint.

In some circumstances, a third party may also be asked to conduct a taste test of the wine to provide a description of the palatability of the wine as well as the level of perceived smoke taint. This is particularly common in situations where the third-party testing only shows a “mild” level of smoke taint based on the phenol markers.

Other Possible Effects of the Wildfires on Wine

Grapes used in winemaking can also be impacted in the following ways:

In most incidences, we will take the following steps to value wine:

Our first step is to review the grape weigh tags for the impacted wine. This allows us to verify both the volume of the wine and the grape varietal.

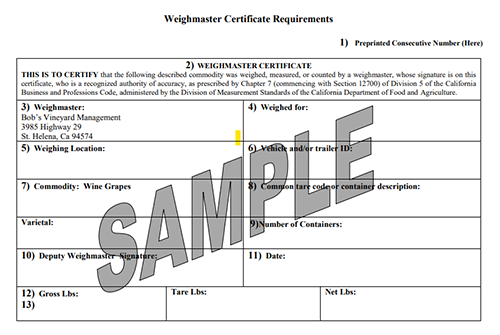

What Is a Weigh Tag?

During a normal harvest, after grapes have been picked from the vine, they will be taken to a weigh station where they will be weighed, and a weighmaster certificate (commonly known as a “weigh tag”) will be produced, showing information including the weigh date, grape varietal & appellation, and net weight.

Why Are Weigh Tags Important?

The weighing process is heavily regulated, and weight tags are mandated for all California wineries by both the Alcohol & Tobacco Tax & Trade Bureau (“TTB”) and the California Alcoholic Beverage Control (CA ABC).

Weighing scales must have a “Legal for Trade” designation and must be registered with the local agricultural office, and the “weighmaster” must be licensed by the state.[11]

The TTB considers a weigh tag a “source document” and will use them as documentation in the event of an audit of a bottled wine, which tracks the wine’s details back from the wine label to the weigh tags.[12]

It should be noted that when valuing wine, we also review inventory records and tank reports; however, for the reasons above, the weigh tag is considered a key source document.

To establish the projected selling value of the wine, we first must establish which program the wine would have been allocated to. The “wine program” is the term for what you see on the label of the wine and will often specify the vineyard, if the wine is a single vineyard, or may have a blend name if the wine is from multiple vineyards.

If the wine has already been bottled at the time of loss, this analysis is not necessary, as the wine is already in a bottle with a label, so nothing is up for debate. However, if the grapes/wine were destroyed or the wine is still in the tank or barrel, it is necessary to determine the program allocation. Our role involves scrutinizing the insured’s projected allocation to see if it is consistent with:

In some cases, the insured is able to provide a blending history showing that grapes harvested from the impacted vineyard and block have been used in the same wine program for several years, making it relatively easy to project the program allocation.

In other cases, things can get more complicated, as illustrated in the following scenarios:

Most insurance policies state the wine should be valued at “projected sales value less unincurred costs.”

Projected Sales Value

Once we have established the program allocation (see Step 2), we then review sales records for the applicable wine program. This is to establish both the average selling price of the wine and the sales channel.

Wine is sold through different sales channels that are typically categorized as:

Typically, prestigious and expensive wines will be sold entirely through DTC channels. As the wines reduce in quality and price, more is sold through wholesale channels.

Determining the sales channel is important, as DTC wine will achieve a higher price than wine sold via wholesale channels. This can become a contentious issue if the insured claims that the impacted wine vintage would have a different DTC v. wholesale allocation compared to previous vintages of the same wine. For example, they may argue that due to an aggressive marketing campaign, they would have sold more of the wine through their online shop.

Unincurred Costs

To calculate unincurred costs we review both production and selling costs. Where the wine is in the production process will dictate the unincurred costs we need to review. For example, if the wine has already been bottled, we will focus on selling expenses. If the wine was in the barrel, we will need to include the costs to bottle and any costs that would be incurred while the wine was in the barrel.

Unincurred production costs may include the cost of the barrel, bottle, label, cap, and cork. We may also consider barrel aging supplies, variable labor costs, and any mobile bottling line costs.

Unincurred selling costs depend on the applicable sales channel, and examples include:

Ultimately, our goal is to establish the net loss to the insured based on projected sales price less any costs that the insured did not incur by not producing the wine.

Library Wines

In some cases, the impacted wine is categorized as a library wine. Library wines are bottles/cases of a vintage that are held back by the wineries after the debut, to be released at a later date.

With library wines, there is often limited sales data, and the projected sales price of the wine can be highly subjective. There is also the possibility that older wine may have spoiled, raising issues of obsolescence.

In these instances, we will look at all available sales data and, in some cases, it is appropriate to appoint a wine expert to assist with the valuation.

Mitigation Efforts

In some instances, if the wine is smoke tainted/heat damaged, it may still be sellable, especially if there is only a mild impact on the taste. This wine can be:

Bulk wine is defined as a wine that is shipped in large containers such as tanks (rather than bottles) and then repackaged at its destination.”[13] Buyers of bulk wine typically include other wineries, exporters, or grocery stores with “home brand wines.” In some cases, bulk wine can be used to make food products like wine vinegar.

Unsurprisingly, sales prices for bulk wine are typically significantly lower than DTC or wholesale prices. Furthermore, there is currently a significant oversupply in the bulk wine market, known as the “Great Grape Glut,” with prices at all-time lows. As a result, it can be relatively difficult for wineries to sell smoke tainted wine.

In smoke taint losses, the most common coverage complication we see relates to the location or ”status” of the grapes at the time of loss, primarily whether they were on the vine or picked when the smoke taint occurred.

Policy wording can vary, but disputes often center on whether the wine falls under “crop” or “inventory” coverage. The valuation differs materially between classification of “crop” (lower value) and “inventory’ (higher value).

To assist with coverage determination, we can look at the grape weigh tags to approximate the date the grapes were picked, as the grapes are usually weighed within 24 hours of being picked. The following scenario is an illustration of this:

Prior to 2019, the California wine industry had looked to Lloyd's of London for inventory throughput policies. However, in July 2019 Lloyd's announced that it would no longer be underwriting these policies because of the annual risk to wine production and storage caused by wildfires.[14]

Specifically, Lloyd's said it would no longer insure “wine grapes on the vine, wine in production and the finished product up until a winery releases custody and control.”[14] The decision was a result of a strategic review of unprofitable lines that was conducted by Lloyd's after it suffered $2.6 billion of losses in 2017.

Lloyd’s of London's actions have put pressure on the domestic markets to respond, but according to Elizabeth Bishop of Heffernan Insurance Brokers, “many are saying they cannot offer the coverage until they’ve renewed their reinsurance treaties and renegotiated them so that they can respond to higher values.”[15]

Furthermore, the aggregation of risk in the Napa and Sonoma wine regions means that one wildfire can result in a catastrophic loss event. Specifically, the retail value of wine produced in Napa and Sonoma equates to approximately 50% of the retail value for California while the volume of wine produced accounts for less than 10% of the state’s total.[15]

All these issues have resulted in significant increases in policy rates, particularly for large, high-end wineries with extremely valuable inventory. As a result, wineries have been forced to take on higher deductibles and many will likely consider using dollars they would have spent on insurance policies for fire mitigation tools.[14]

In addition to destroying wine inventory, wildfires can impact wine/grapes through smoke taint, spoilage, or heat damage. We most commonly see claims relating to wine that has been impacted by smoke taint and which cannot be sold through normal sales channels.

We typically take the following key steps to value wine inventory:

If the wine we are valuing is a library wine with limited sales data, it may be necessary to involve a wine expert to assist with the valuation.

A common coverage issue to be aware of relates to the “status” of the grapes at the time of loss and whether they were on the vine when smoke taint occurred or if they had already been picked. This can determine whether they would be categorized as “crop” or “inventory."

Finally, due to the annual devastating wildfires and the aggregation of risk in Napa and Sonoma, Lloyd's of London announced in 2019 that it would no longer be underwriting California wine inventory policies. As such, the wine insurance industry is undergoing substantial change, resulting in significant increases in policy rates and even prompting some wineries to self insure.

We would like to thank Tim Gillihan, CPA, ABV, CFF, Hannah Dingley, ACA, & Trevor Eaton for providing insight and expertise that greatly assisted this research.

Tim Gillihan is a Senior Vice President in J.S. Held’s Economic Damages & Valuations Practice. He brings more than a decade of forensic accounting experience and is primarily engaged as a consultant by attorneys, insurance companies, independent insurance adjusters, and businesses. He specializes in the financial evaluation of damage claims and fraud cases, including first-party property losses, third-party liability cases, commercial litigation damages, partnership disputes, and fidelity matters. A certified public accountant, he has also provided analysis of business valuation, divorce, trust/estate, personal injury, death, and employment discharge cases.

Tim can be reached at [email protected] or +1 510 740 0386.

The purpose of this paper is to discuss some of the major work and financial matters forensic accountants focus on, including fraud investigations and insurance claims, and how they bring unique value to the process....

Hurricane season is always a time of year when many businesses can expect to suffer losses and when catastrophe claims arise as a result, but what happens when losses from seasonal catastrophes are complicated even...