Insights

J.S. Held Acquires Shechter & Everett to Expand Forensic Accounting Capabilities for Family Law Disputes in Florida

Read MoreAfter a significant delay, the Securities and Exchange Commission (SEC) adopted its final rule [1] on Wednesday, March 5, 2024, that requires companies who file registration statements and annual reports to disclose material climate-related risks. [2] The new rules, which become effective 60 days after publication, are phased in for registrants depending on their filing status, with smaller companies having later compliance dates. As has been well reported, Scope 3 emissions, those greenhouse gas emissions calculated based on activities in a corporate value chain, have been removed from the final rule.

SEC Chairman Gary Gensler, in the press release associated with the passage, noted:

These final rules build on past requirements by mandating material climate risk disclosures by public companies and in public offerings. The rules will provide investors with consistent, comparable, and decision-useful information, and issuers with clear reporting requirements. Further, they will provide specificity on what companies must disclose, which will produce more useful information than what investors see today. They will also require that climate risk disclosures be included in a company’s SEC filings, such as annual reports and registration statements rather than on company websites, which will help make them more reliable.

There are two key takeaways from the Chairman’s comments: 1) everyone is now on the same playing field; and 2) the disclosures, because the information will now be consistent, can be used in a meaningful way.

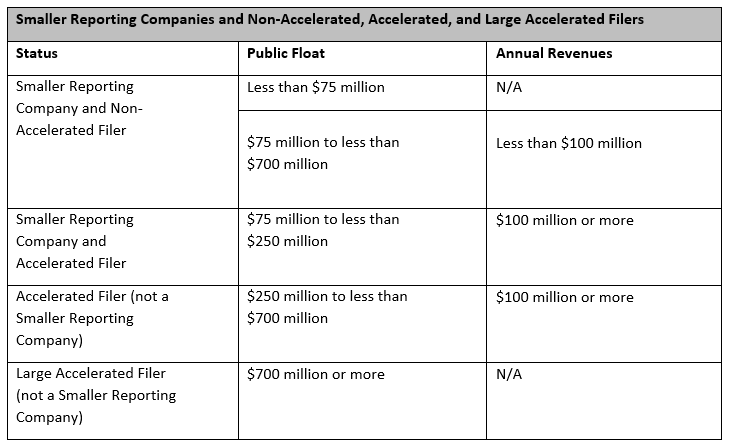

All registrants are required to comply with the rule; this includes large accelerated filers (LAFs), accelerated filers (AFs), non-accelerated filers (NAFs), smaller reporting companies (SRCs), and emerging growth companies (EGCs). The SEC defines the categories of companies under Rule 12b-2 of the Securities and Exchange Act of 1934. While there are several triggers, public float and annual revenue thresholds provide good guidance to make the determination as to what category applies.

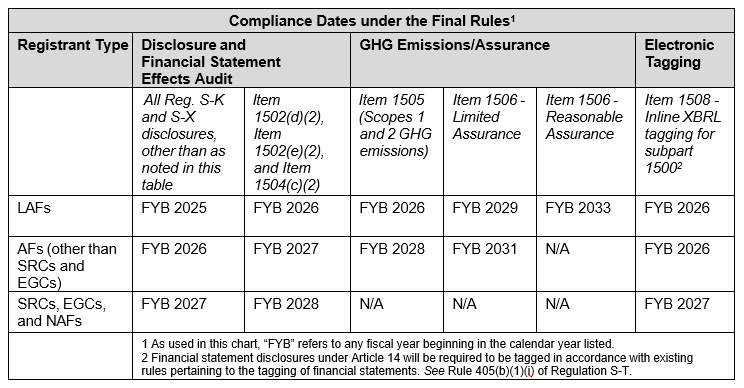

For large accelerated filers, compliance starts in fiscal year 2025, so the time to prepare for and comply with the new rule is short. Scope 1 & 2 emissions reporting is pushed to 2026 at the earliest, and small companies are exempt from that reporting requirement. As indicated in the SEC-provided chart below, compliance dates are staggered between FYB2025 and FYB2033.

Fortunately, the method of disclosure required by the rule is straightforward. The climate-related disclosures are simply additions to existing reporting requirements. The disclosure must appear in registration statements and annual reports and meet the electronic tagging requirements. While the rule allows for the disclosure to be made in “another appropriate section” of the filings, it is likely that climate-related disclosures will constitute their own section in most registrants’ reporting.

What Must Be Disclosed?

Climate-related disclosures must include:

Both sides of the ESG argument appear to be lining up to challenge the SEC’s final rule. [3] As mentioned previously, West Virginia Attorney General Patrick Morrisey has already announced a 10-state challenge. Sierra Club and Earthjustice believe the rules as passed are not sufficient particularly because of the omission of Scope 3 from the reporting requirements. Because ESG has become more and more politicized, litigation will be an ongoing consideration for rulemaking.

Climate-related financial reporting and ESG will become like seatbelts. In the early 1980s Michigan Representative David Hollister proposed a seat belt law. He was threatened with recall by a fellow legislator and called terrible things. [4] At the time, only 14% of Americans used their seatbelt. Following a long push nationally, by 2020, national use of seatbelts has reached more than 90%. [5]

Over time, seatbelt use became ingrained in society. Public companies already have reporting obligations to report material concerns to their investors and the public. The SEC rule now just defines and harmonizes those obligations. That is better for public companies as compliance is easier when there are well-established rules. It is also better for investors and the public as evaluations are easier because the data is uniform. The rule will become like seatbelts, just part of a normal, daily reality.

There seem to be a few unknowns remaining. Legal challenges are front and center to be sure. Existing reporting programs may need revision to comply with the new SEC rule. There are clear overlaps with other regulatory programs, particularly for multinationals, because of existing reporting obligations in, for example, the European Union through its Corporate Sustainability Reporting Directive. Similarly, California’s climate disclosure laws, passed last year, imposed requirements both for public and private companies which reflects that the various programs have slightly different obligations. Ultimately, companies will need guidance from each of the existing requirements to understand how to comply with all the programs with a single reporting effort. That much-needed guidance will need to be developed.

We would like to thank our colleague John Peiserich for providing insight and expertise that greatly assisted this research.

John F. Peiserich is an Executive Vice President and Practice Lead in J.S. Held’s Environmental, Health & Safety practice. With over 30 years of experience, John provides consulting and expert services for heavy industry and law firms throughout the country with a focus on Oil & Gas, Energy, and Public Utilities. He has extensive experience evaluating risk associated with potential and ongoing compliance obligations, developing strategies around those obligations, and working to implement a client-focused compliance strategy. Mr. Peiserich has appointments as an Independent Monitor through EPA’s Suspension and Debarment Program. John routinely supports clients in a forward-facing role for rulemaking and legislative issues involving energy, environmental, Oil & Gas, and related issues.

John can be reached at [email protected] or +1 504 360 8373.

We discuss the requirements outlined in the CSDDD, who would have been affected, why the directive did not pass, and whether this signals a green retreat....

In mid-November 2022, the European Parliament adopted the Corporate Sustainability Reporting Directive (CSRD), a major expansion of the 2014 Non-Financial Reporting Directive (NFRD). The new rules will quadruple the number of companies required to provide...

Boards of Directors are the lynchpin to effective sustainability programs. Effective sustainability programs can only be created and maintained when there is consistent support from the management team. Without an open and apparent management team...