Insights

J.S. Held Acquires Shechter & Everett to Expand Forensic Accounting Capabilities for Family Law Disputes in Florida

Read MorePublication Date: May 23, 2024

On 29 May, South Africans go to the ballot box to vote in the country’s most significant election since 1994. Voters will elect members of the national and provincial legislature, with the majority party, or coalition, going on to form a government and install a president. The incumbent African National Congress (ANC), under the leadership of President Cyril Ramaphosa, is likely to lose its parliamentary majority and be forced to enter a coalition to govern. The electorate is increasingly frustrated with poor service delivery, persistent economic challenges, and violent crime.

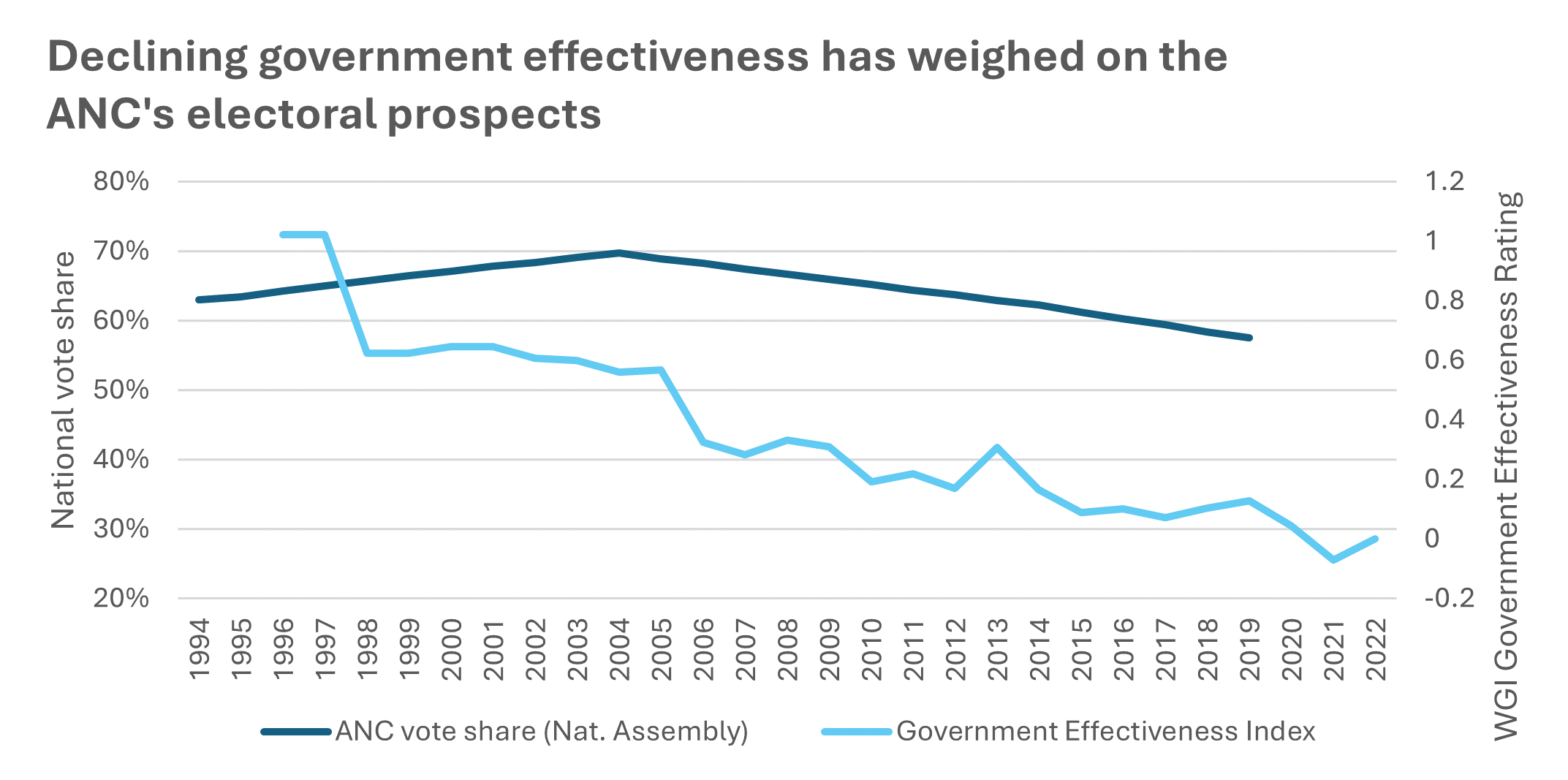

The key concerns for voters heading to the polls are joblessness, service delivery, crime, and immigration. South Africa’s unemployment rate stands at 32%, while the country has one of the highest rates of violent crime in the world. Government effectiveness has steadily declined since 1994, initially based on the democratisation of services after the end of Apartheid, but increasingly as underinvestment and maladministration have weakened institutional capacity. Rolling electricity cuts - known as “loadshedding” - are the stark manifestation of the government’s failure on service delivery.

Source: Independent Electoral Commission of South Africa, World Bank

Against that backdrop, opposition parties have found it easy to adopt absolutist platforms. Several have framed this election as a ‘make or break’ vote for the country’s future. The centre-right Democratic Alliance (DA), the official opposition, has campaigned on South Africa’s “survival” and promises to rescue eroded state institutions. While, in its manifesto, the far-left Economic Freedom Fighters (EFF) declared the need to end an economic and social apartheid which it alleges has continued under 30 years of ANC rule.

There remains huge uncertainty heading to the election, which is just one week away. Key questions include how low ANC’s vote-share will drop, and with whom the ruling party will choose to partner.

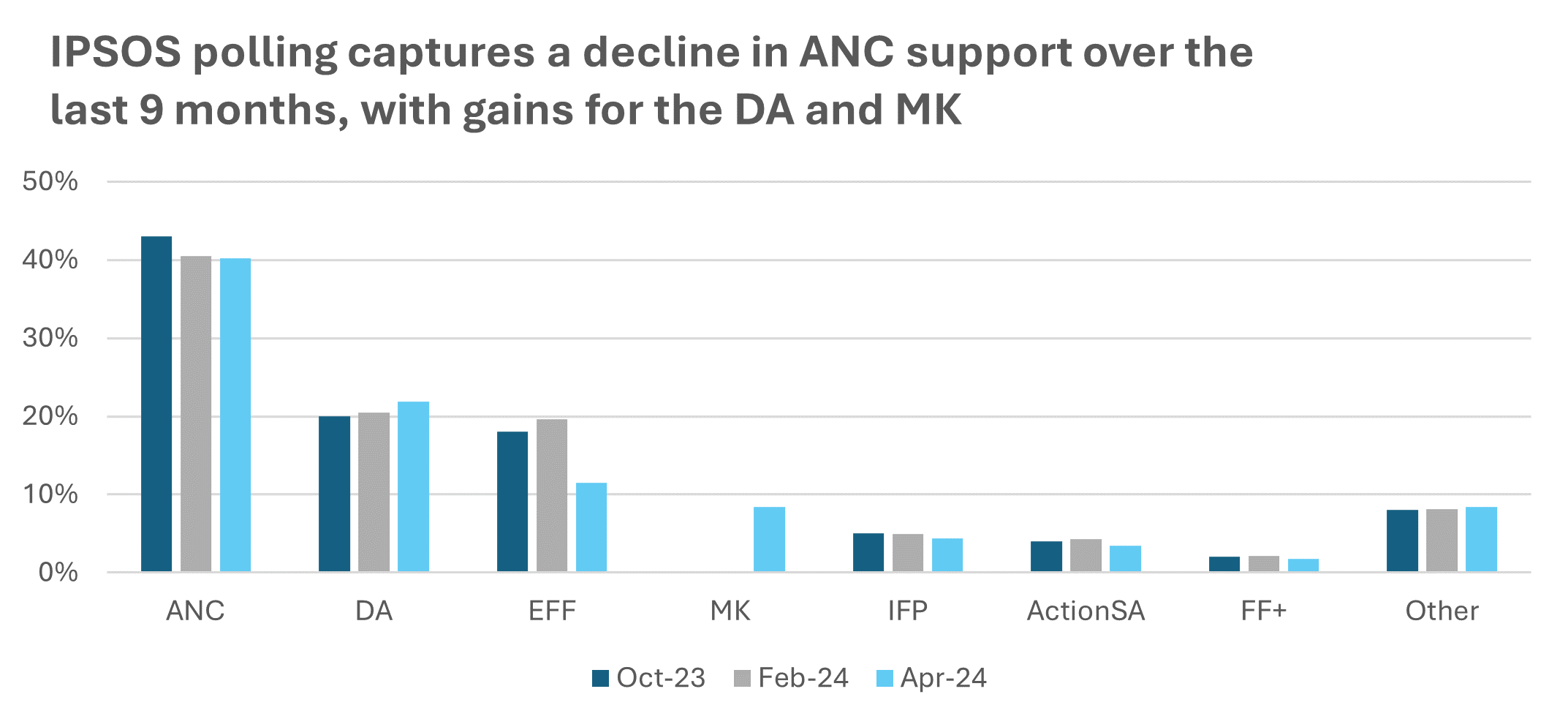

Since the last general election in 2019 all signs point to a weakened ANC emerging from this month’s vote. While disagreeing on the extent of the ANC’s decline, public pollsters are aligned on the negative trajectory of the ruling party’s popularity. Since mid-2022, no major poll has placed support for the ANC at over 50% of the electorate – a threshold below which the ANC must cooperate with the opposition in order to form a government and decide a president. One of the more credible polling agencies, IPSOS, measured the ANC’s support at 40.2% in late April 2024.

Part of the decline stems from ANC’s diminishing popularity in key vote blocs hosting major urban areas beset with service delivery challenges – mostly notably in Gauteng and KwaZulu-Natal provinces. Larger parties such as the DA and EFF are entrenching their footholds in pockets of Gauteng (home to Johannesburg and Pretoria), and smaller offshoots like ActionSA have begun to make a dent. Meanwhile the emergence of uMkhonto we Sizwe (MK), the party led by former president Jacob Zuma, has heightened an already competitive race in KwaZulu-Natal (home to Durban), which looks set to split to the ANC’s detriment. Despite a concerted fight back by the ANC in both Gauteng and KwaZulu-Natal, the party has continued to lose ground.

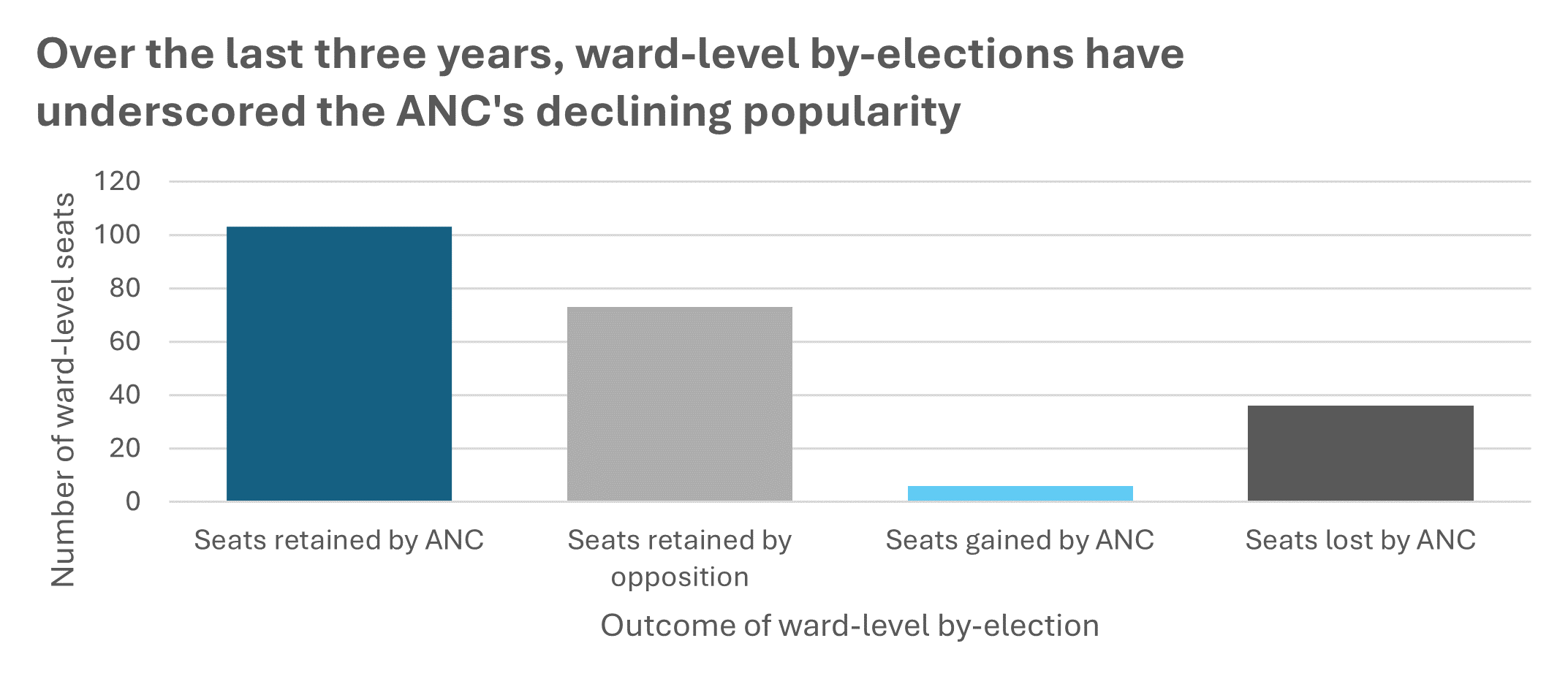

Source: Independent Electoral Commission of South Africa

Institutional biases, underweighting of the rural vote, and overestimations of turnout might undermine the credibility of the polling, but by-election results reveal the same downward trend. Since South Africa’s last municipal election in 2021, the country has held 218 ward-level by-elections. Over that period, the ANC lost 36 seats it had won just three years ago; the party experienced some of its heaviest losses in KwaZulu-Natal and Gauteng despite re-upping its campaigns in the provinces. With most trends moving in the wrong direction for the party, our base case of the ANC falling short of a majority looks increasingly convincing.

Nonetheless, a number of factors suggest that pollsters likely overestimate the extent of the ANC’s decline, with the party unlikely to slip into the low forties some project.

While polls reflect an erosion of support for the ANC, they also capture the uncertainty voters feel about an alternative. The aforementioned IPSOS poll notes that 35% of respondents feel no party represents their views. Within this group, many will opt not to vote owing to disillusion with the options on the table. As in 2019, this would contribute to a lower turnout scenario which polls do not currently capture, and which favours the ANC as the incumbent.

Source: IPSOS

Similarly, because the by-elections bode negatively for the ANC, they also reflect what is arguably its greatest asset: its election machinery. The ruling party is the only one to have contested all 218 by-elections since 2021. With just 11 exceptions, the ANC also ranked within the top three parties in terms of vote share. This underscores the reach of the ANC, which has invested heavily in grassroots structures across the country and can tap rural constituencies far beyond the discontented urban vote. The oppositions’ failure to match this campaign infrastructure continues to hand the ANC supermajorities in predominantly rural provinces where it maintains an edge.

Opposition parties also meanwhile have failed to close ranks and pool campaign resources, vouching instead to participate in a fragmented race. This year 70 political parties and 11 independent candidates will compete for seats in the National Assembly, up from 48 parties in 2019. Members of the Multi-Party Charter – an alliance of 11 political parties including the DA and IFP – have committed to form a government in the event they collectively secure a majority. Until then they are campaigning on distinct policy platforms and often jockeying for the same constituencies. Under South Africa’s proportional representation system, a proliferation of smaller parties serves to undermine their prospects of hitting the threshold for a parliamentary seat. In doing so, it also acts to deprive larger outfits of vote share.

Dynamics within the ANC and around potential coalition negotiations suggest that policy instability will increase following the election, irrespective of how short the party falls of a majority. If the ANC secures 45% or upwards of the vote – as we anticipate – it will be able to cobble together a governing majority with a collection of small parties, or with the help of the IFP. Given their relative size and limited leverage, these parties are unlikely to exert significant influence on government policy and will not occupy key cabinet positions.

Below the 45% mark, the ANC must consider partnering with larger parties such as the EFF or the DA. The EFF promotes an aggressive land redistribution and nationalization program, placing it at odds with most investors. DA policymakers support a weaker central government, less ambitious land redistribution policy, and broad deregulation. Both parties have sufficient weight to enact modest policy adjustments, taking the debate further to the left or the right. But the ANC would most probably seek a coalition agreement which places its rival in a firmly junior position. Indeed, the EFF or DA would need to make material concessions to position themselves as the ANC’s preferred partner, and therefore self-imposing guardrails on their policy influence.

Policy instability is instead most likely to come from within the ANC itself, as it has thus far. On issues of energy in particular, officials openly contradict government policy to serve their own factional interests. Intraparty politicking has led to three ministers having oversight of the energy docket and has motivated the creation of parallel decision-making structures in the presidency. Ramaphosa’s inability to rein in ANC factions underscores his overall weakness in the party, which is only set to worsen as the election promises a negative verdict on his administration. In that context factions will become more assertive, with some already preparing to mount leadership challenges. This will muddy not only the ANC’s position on policy, but potentially also on coalitions as eventual changes in leadership herald possible shifts in preferred partners.

We would like to thank our colleagues Connor Vasey and Anna Westwell for providing insight and expertise that greatly assisted this research.

Anna Westwell is a Senior Associate on J.S. Held's Africa-focused Strategic Advisory team. She predominantly advises clients on Southern and East African political, economic, and regulatory issues. Anna has worked across multiple sectors, including agriculture, FMCG, energy, telecoms, mining, and logistics, to provide support to clients investing, or looking to invest in, African markets. Previously in her career, Anna worked as a researcher at a South African foreign policy think tank. She also conducted social research and assisted with stakeholder engagement and campaigns for several NGOs based across Zimbabwe, South Africa, and the UK.

Anna can be reached at [email protected] or +44 20 8706 1949.

We examine the position that Africa occupies in today’s GSCs and discuss what this means for the continent in the near future and beyond....

J.S. Held experts share their thoughts following trips to Côte d'Ivoire and the Democratic Republic of Congo, and offer advice for investors operating in, or looking at, the two countries....