Insights

J.S. Held Acquires Shechter & Everett to Expand Forensic Accounting Capabilities for Family Law Disputes in Florida

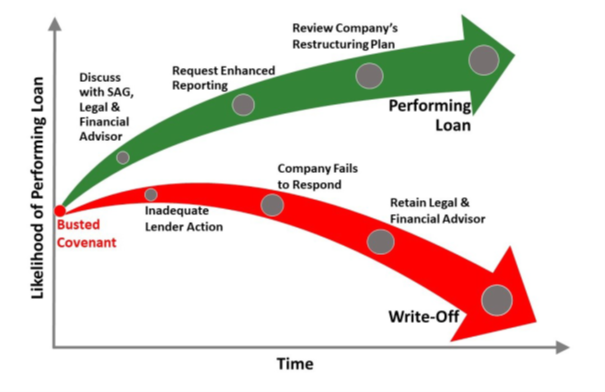

Read MoreHow can you guide a troubled company to maximize its restructuring options for the best outcome? The key is early action and direct communication. Here’s why.

During our decades of experience in the restructuring sphere, far too many clients have hesitated before calling to discuss distressed companies. The companies were beyond resuscitation, resulting in write-offs for the lenders.

Taking action as soon as a borrower’s performance takes a downturn often results in a cascade of positive actions – the lender preserves collateral; management implements reformative actions (or shows that it won’t); and, company advisors are informed, allowing collaborative brainstorming to yield the best outcome. Alternatively, hoping a company’s downward trends will improve without a solid plan in place typically costs lenders time and money in the long run:

Source: Copyright © 2022 Stapleton Group, Inc.

We recommend the following best practices to ride the upward-sloping green curve to performing loans, instead of the death spiral red curve.

Make introductions during the onboarding process before any issues arise.

Not just current financial statements and forecasts!

Insist that the board or management team provide accurate, timely operations reporting that provides leading indicators to performance: rolling 13-week cash forecast updated weekly, purchase orders, employee turnover, significant changes with customers, tax issues, etc.

Go above and beyond the quarterly call to check in.

Be realistic about time spent on troubled borrowers.

Establish protocols to follow when a borrower hiccups.

Proceed deliberately.

We would like to thank our colleague, Mike Bergthold, for his insights and expertise that greatly assisted this research.

Mike Bergthold, is a Senior Managing Director in J.S. Held’s Strategic Advisory practice. He joined J.S. Held’s Strategic Advisory Group in October of 2024 as part of J.S. Held's acquisition of Stapleton Group. Mike is a highly experienced turnaround executive who reduces complex problems into actionable plans to drive immediate and measurable positive results. He leverages over 30 years of experience advising public and private companies on strategy, finance, and accounting to serve as CRO, financial advisor, interim executive, or strategic board member for companies in financial distress or transition.

As an interim CEO, CFO, president, or director of companies in transition, Mike skillfully guides management teams and stakeholders through strategic planning, budgeting and forecasting, complex negotiations, and recapitalizations. Prior to joining Stapleton Group, Mike was a licensed CPA in California and Arizona for 25 years. He also held positions at EY and Andersen and was a senior executive at accounting and IT outsourcing firms.

Mike can be reached at [email protected] or +1 213 404 0113.

This article examines the impact of the Uniform Commercial Real Estate Receivership Act (“UCRERA”) in Arizona and analyzes the important differences between UCRERA and Arizona's pre-UCRERA receivership process, as well as the potential legal issues...

A guide to ensuring the proper transfer of IP assets, including critical steps, key considerations, and working with the right attorney....

How forensic accountants work closely with counsel to understand the legal concepts of matters and, at the same time, delve into the details of corporate records....